I do not like traditional life insurance plans and always advise readers to stay away from such plans. Traditional life insurance plans provide low life coverage and poor returns.

But what about those who have already purchased such a plan? Should such policyholders surrender the plan? Well, not always.

If you have already purchased the plan, surrender of the policy may not always be a prudent choice. The reasons include front loaded commissions and heavy surrender penalty.

If you work out the numbers, it may actually make a lot of sense to let the plan run its full course if you have paid premium for a few years. The outcome will depend on the plan features, surrender value, number of years of premium paid and the policy term. So, do not jump to any conclusion. Do some maths and make a decision subsequently.

The rationale is that the surrender value and the future premiums should yield much better results than the expected maturity value of the insurance plan. For instance, if you need to earn 14% return on surrender value and future premiums just to match expected maturity value of the insurance plan, it may actually make sense to continue. If the required return is only 6%, it is better to surrender the plan. Go through the following post for more on this.

Must read: Surrender, continue or paid up: What should you do?

If you have decided to continue the plan, you will do well to be aware of a fringe benefit that traditional insurance plans can provide.

Are you aware that you can take loan against your LIC policy?

In this post, I will discuss loans against LIC policies, eligibility, repayment structure or whether it makes sense to opt for such loans.

I pick up LIC New Jeevan Anand, a very popular participating non-linked endowment plan from LIC. The term and conditions will be similar for other plans too. The analysis in this post will be based on LIC New Jeevan Anand.

Must Read: Stay away from LIC New Jeevan Anand

How much can I borrow against my LIC plan?

You can borrow up to 90% of the Surrender Value of the plan (85% in case of paid up policies) as on date of application.

You can make an application for loan only once you have paid premium for three years.

It goes without saying that you can take a loan only once your policy acquires surrender value. Typically, LIC plans acquire surrender value only after 3 years.

You have to assign the policy to LIC as security.

How is the loan repaid? What is the loan tenure?

You get a lot of flexibility.

You have to pay interest every six months.

About the principal, you can repay the loan till maturity of the policy.

You just need to keep making the interest payments on time and you won’t hear from LIC about principal repayment.

Alternatively, if you wish, you can also repay principal along with interest.

In fact, if you do not repay principal even till maturity/death, LIC will automatically square off the outstanding loan amount against maturity/death benefit and pay the balance to you/ your nominee.

You borrow for a minimum of six months (minimum tenor). Even if you want to foreclose the loan before six months, you will have to pay interest for at least six months.

Book Suggestion: How to Retire Rich: Invest Rs 40 a day? (P V Subramanyam)

What is the applicable interest rate?

The interest rate is declared by LIC and may vary according to the insurance plan. You can enquire about the prevailing interest rate from the LIC.

As I understand, the prevailing rate of interest is 10.5% per annum.

Book Suggestion:How to Retire Rich: Invest Rs 40 a day? (P V Subramanyam). Hindi version is available too.

What If I default on my interest payment?

If you do not pay interest amount within 30 days from the due date, LIC reserves the right to foreclose the policy and settle the loan amount against the proceeds.

Illustration

If you are planning to borrow against your LIC policy, you need to find the current Surrender Value of the plan. Surrender value will determine your loan eligibility.

How to find the Surrender Value?

Well, you can simply call your agent or walk in to the nearest LIC branch to find out the Surrender Value. You do not have to go through the following exercise.

In this post, I will try to assess the Surrender Value for the particular scenario for LIC New Jeevan Anand. I do not guarantee that the value is accurate. But it will give an idea about how loan eligibility is calculated.

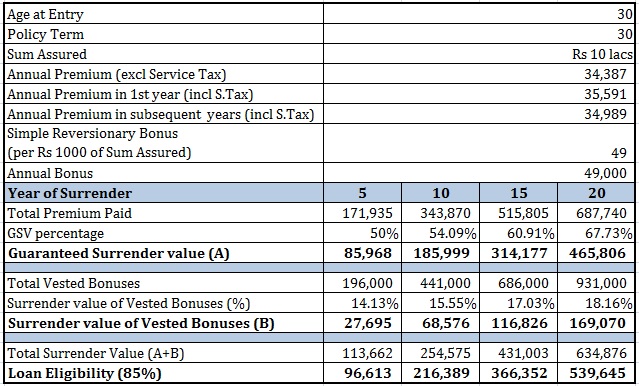

Let’s say you purchased LIC New Jeevan Anand 15 years back (by the way, the plan didn’t exist at the time) when you were 30. The Sum Assured is Rs 10 lacs and the policy term is 30 years. You have paid premium for 15 years.

The annual premium is Rs 34,387 (before Service Tax). For the first year, the premium will be Rs 35,590 (including service tax of 3.5%). For the subsequent years, the annual premium will be Rs. 34,988 (including service tax of 1.75%).

For LIC New Jeevan Anand, Surrender Value is the sum of

Guaranteed Surrender Value of Premiums paid (GSV)

And

Surrender Value of Vested Reversionary Bonuses (SVV)

There is also provision for the payment of Special Surrender Value, if it is more beneficial to the policy holder. However, I will ignore special surrender value for the purpose of this exercise. In any case, you don’t have to calculate this value on your own since it is readily available with your agent or at the nearest LIC branch.

Guaranteed Surrender Value is the percentage of total premiums paid till date excluding any tax or rider premiums. The percentage is a function of policy term and number of years of premium paid. The tabulation is provided in the policy document.

For instance, if you surrender the policy after 15 years, the applicable percentage is 70% for a policy term of 20 years and 60.91% for policy term of 30 years.

Guaranteed Surrender Value

= No. of years of premium paid * Annual Premium before Service tax * GSV percentage

=15 * 34,387 * 60.91% = Rs 3.14 lacs

Surrender value of vested reversionary bonuses is calculated in the same manner. You have a separate tabulation for applicable percentage in the policy document.

Let’s assume LIC announced Simple Reversionary bonus of Rs 49 per thousand of Sum Assured for each of those 15 years. Your annual bonus will be Rs 49,000.

You will have received 14 annual bonuses. Total Simple Reversionary bonus = Rs 49,000 * 14 = Rs 6.86 lacs.

Surrender percentage after paying 15 premiums in 30 year policy is 17.03%.

Surrender value of vested bonuses = 17.03% * 6.86 lacs = Rs 1.17 lacs

Surrender value of the policy = Rs 3.14 lacs + 1.17 lacs = Rs 4.31 lacs

Loan Eligibility = 85% * Rs 4.31 lacs = Rs 3.66 lacs

I have calculated the loan eligibility for the same plan in different years.

You can see loan eligibility grows as your policy grows older.

What are the benefits of loans against LIC policies?

- Quick disbursal. It is your money. You can expect the loan disbursement to be swift.

- Not much documentation required. Only the policy to be assigned to LIC. No additional security.

- At interest rate of 10.5% per annum, it is much cheaper than personal loans.

- You get a lot of flexibility. There is no EMI like repayment schedule. You can repay the principal and when you want. Can be very useful when you are facing cash flow pressure.

What are the drawbacks?

Since loan amount is linked to surrender value, you cannot expect to take a high value loan against the policy. You can see even after paying premium for 20 years, the loan eligibility is only 5.39 lacs (in the example discussed above).

There is no tax benefit for repayment of loan against LIC policy.

Points to Note

- Loans are offered against traditional life insurance plans only.

- Financial institutions other than LIC also offer loans against LIC policies. However, the rate of interest is typically higher than the rate charged by LIC. Can’t see why anyone would do that when LIC offers at a lower rate.

- Even though I have calculated surrender value many times in this post, you do NOT have to surrender the plan to take the loan. You merely need to find the surrender value. If you surrender the plan, you won’t get any loan.

- You can also request a second loan against the same policy while first loan has not been repaid. The cap of 90% of Surrender value shall apply to the combined amount.

How to apply for loan against LIC policy?

You need to submit Form 5196 to your agent or the nearest LIC branch to take out a fresh loan. For a follow-up loan (second loan), you need to submit Form 5205.

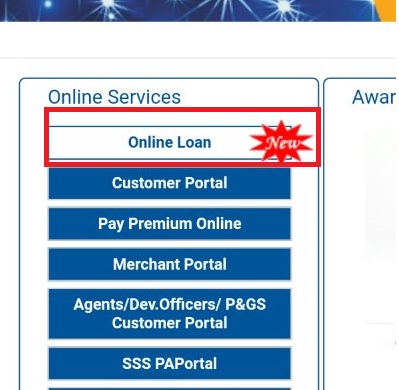

Now, you can apply for Loan from LIC and even make loan payments online

Do note that the loan application can only be initiated online. It cannot be completed online. There is an offline step involved.

You need to do is to register on LIC website. To register, you will need a few pieces of information such as your LIC Policy Number and a few personal details. You can go to the following link (https://licindia.in/Home-(1)/LICOnlineServicePortal) and click on “New User”.

Once you have registered, you need to login by clicking on “Registered User”.

However, your job is not yet done. Once you log in, you need to subscribe for “LIC Premier Services”. You can apply for a loan against your LIC policy only once you are a Registered LIC Premier Services User.

To register as Premier User, you need to download an auto-generated form, take a print-out, sign the form and upload on the LIC site.

Hopefully, within a few days or weeks, your request for Premier Services Registration will be approved. Subsequently, you can apply for a loan online through the LIC portal.

Do note the link to Apply for loan online is available on the home page too. (https://www.licindia.in/). You can click on that link too. However, you will still need to log in (after registering) into LIC portal and be a “Registered Premier Services User” before you apply for the loan.

A few screenshots of how to apply for Loan against LIC policy online

Link on the loan Page on LIC Home page or directly click on the following link (https://www.licindia.in/home/policyloanoptions)

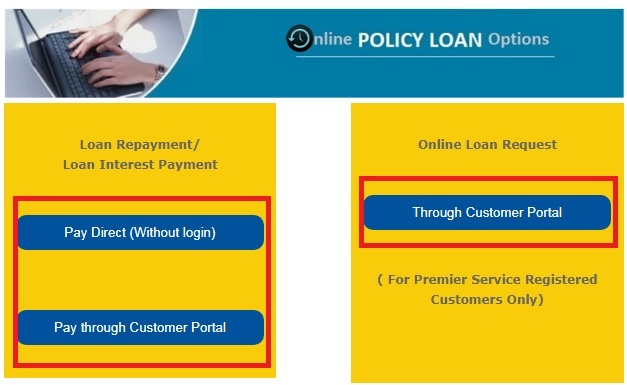

You can apply for the loan online. You can make loan repayment or interest payment online too.

Once you have logged in, you need to register for LIC Premier Services. Alternatively, you can click on Service Registration–>Service Request–>Premier Services Registration to complete the process.

To register for premier services, you need to follow a 3-step process. You need to download an auto-generated form, print, sign, scan and upload on the portal.

Once your registration for LIC Premier Services is accepted, you can apply for loan online by clicking Service Registration–>Service Request–>Online Loan Request.

Once you have completed this step, you need to submit the following documents at the nearest branch (and not your base branch).

- Printed and signed Loan application form

- Policy Document

- NEFT Mandate form (for loan disbursal)

You need to submit these documents within 4 days of making the online application. If you fail to do so, your application will be automatically rejected and you will have to apply again.

You can track the status of your loan application or your application for Premier Services Registration under Registration–>Service Request–>Request Status.

PersonalFinancePlan Take

Traditional life insurance plans are poor products. However, if you are trapped in one, loan against the policy is one feature you can explore if you are looking for low cost debt.

Loan against LIC policy can be a cheaper alternative to personal loans.

Do note interest rate is important. 10.5% may be okay. However, if you get a loan at 13-14%, it may be prudent to actually surrender the plan and use the proceeds for your requirement rather than taking out a loan against the same LIC policy.