In a rising interest rate scenario, liquid funds and money markets are good choices for debt mutual fund investments. If you are willing to hold until maturity and are comfortable with interim volatility, you can also consider target maturity ETFs and index funds.

The Reserve Bank has increased the rates by 90 bps since the beginning of May 2022. And going by their commentary, more Repo rate hikes are in the offing. If you have invested in debt funds, your fund NAV might have fallen. And the possibility of further rate hikes must concern you.

Which are the best debt mutual funds in a rising interest rate scenario?

When interest rates rise, the bond prices fall. This is established but by how much?

Duration is a measure of interest rate sensitivity. Higher the modified duration, greater the sensitivity to interest rate movements.

Higher Modified duration —> Higher interest rate risk

Short term bonds (or debt mutual funds) have low modified duration. Thus, if the interest rates were to rise, such bonds and debt mutual funds will fall less.

Long term bonds (or debt mutual funds) have higher duration. Will take a bigger hit if the interest rates rise.

So, the simplest suggestion is to invest in low duration funds but there is nuance to this.

Yield rise or fall won’t be the same across all maturities

When RBI hikes rates, not all bonds take the same hit.

Yes, there is difference in duration across bonds and debt mutual funds. And that explains the difference in price movement in various funds when interest rates change.

However, the rise (or fall) in the interest rate is also not the same across all maturities. So, if the RBI increases the rates by 50 bps, it does not mean that the 10-year Government Bond yield will also go up by 50 bps.

In fact, when the RBI increased Repo rate by 50 bps on June 8, 2022, the 10-year government bond yield actually fell from 7.52% to 7.43% and then inched back up slightly. Long duration bond fund showed positive returns for the day. Surprising, isn’t it?

But that’s the way capital markets are. The markets work on expectations. We have seen this all too often in equity markets. The company reports bad earnings but the stock rises since the earnings were better than expected. Or the company reports good earnings but the stock falls since the earnings were worse than expected. And the debt markets are not too different. Game of expectations.

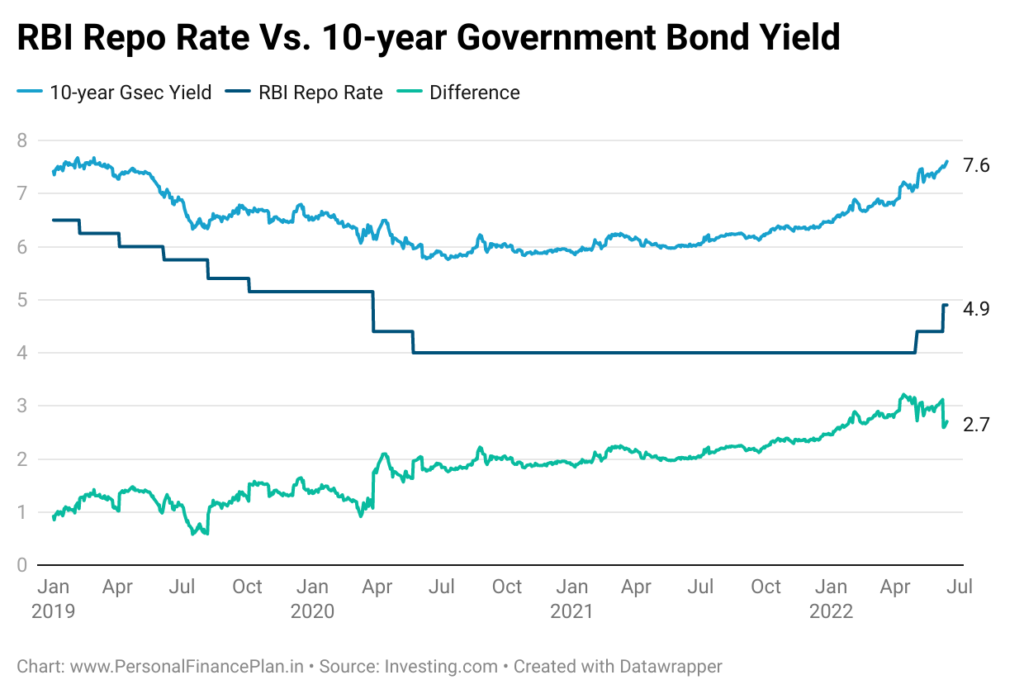

In the chart below, I plot how RBI repo rate and 10-year Government Bond yield have changed since 2019.

Since May 3, the repo rate has gone up by 90 bps. On the other hand, 10-year Gsec yield has gone up by only 48 bps.

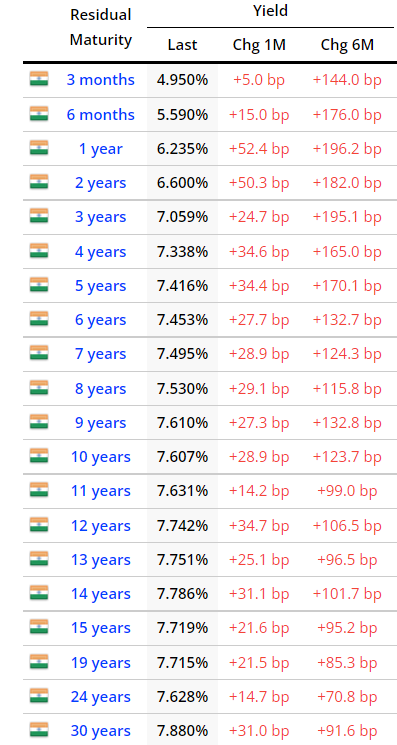

Further, I reproduce the yields for various Government Bonds (as on June 13, 2022). The table also shows the change in yields for various maturities over the past 1 month and 6 months.

Source: WorldGovernmentBonds.com (India, June 13, 2022)

Focus on the change in yields over the past 6 months. You can see that the yields have gone up sharply over the shorter end of the yield curve (short term bonds).

The yield curve was much steeper six months ago. Also evident from the chart below.

Source: WorldGovernmentBonds.com (India, June 13, 2022)

The fall in price of bonds (debt fund NAV) will be a function of 2 things.

- Change in yield for that maturity (for now, let’s ignore the expansion or compression in credit spreads)

- Duration of bond/debt mutual fund

Fund A (short duration): Modified duration: 0.5, Change in yield: 1%. Change in NAV = 0.5 X 1% = 0.5%

Fund B (long duration): Modified duration: 6 , Change in yield: 0.25%. Change in NAV = 6 X 0.25% = 1.5%

While you are likely to see more damage in longer maturity debt funds simply because of high duration, do keep the above dynamic in mind.

When the yields rise, bond prices fall but the prospective returns improve

When the interest rates or yields rise, the bond price or debt fund NAV falls but the YTM (Yield to maturity) goes up.

Reproducing definition of YTM from Investopedia.

Yield to maturity (YTM) is the total return anticipated on a bond if the bond is held until it matures. Yield to maturity is considered a long-term bond yield but is expressed as an annual rate. In other words, it is the internal rate of return (IRR) of an investment in a bond if the investor holds the bond until maturity, with all payments made as scheduled and reinvested at the same rate.

YTM for a bond or a debt fund is the best indicator of prospective returns from a bond/debt mutual funds.

Let’s consider an example. You buy a fresh 10-year bond that pays a coupon (interest) of 6% per annum. The face value is Rs 100. A coupon of Rs 6 every year. Price of the bond is Rs 100.

Suddenly, the yield goes up to 7%. The price of the bond will fall to Rs 92.97.

If the yield goes up to 8%, the price will fall to 86.6.

If the interest rate/yield goes up further, the price will fall more. But it will pay the same coupon of 6% every year.

If you were to purchase the bond at the price of Rs 86.6 and hold the bond until maturity, you will earn 8% p.a. Yes, there is risk that the interest rate will rise more, and the bond price will fall further.

However, if you are content with 8% p.a. and can ignore volatility, you can lock-in the yield of 8% p.a.

You must see if this is good enough for you.

But there is a problem. This approach is fine with bonds that have finite lives.

Most debt mutual funds have infinite lives and thus you can’t lock in a yield. The exceptions are target maturity ETFs/index funds FoF as we will discuss in the next section.

Which debt funds to invest in a rising interest rate scenario?

In a rising interest rate scenario, long duration bonds or debt funds will likely be hit more.

#1 Pick funds with lower modified duration

Your choices are overnight funds, liquid funds, ultra-short duration funds, low duration fund or money market funds.

In the overnight funds, the returns are usually too low for my comfort. So, I will rule these out.

As per SEBI Classification of debt mutual fund schemes, in ultra-short and low duration funds, there are restrictions on interest rate risk but not credit risk. I am not comfortable taking a lot of credit risk in my debt investments. We all saw what happened with Franklin debt mutual funds.

Hence, if you must invest in these two categories, you must check the credit quality of the portfolio before investing. Or

Invest in liquid funds or money market funds.

With liquid and money market schemes, you control both interest rate and credit risk to some extent. Select a debt mutual fund scheme from an established fund house, large AUM, and a low expense ratio.

Over the past couple of years, the yields in liquid funds and money market funds were quite low. 3-3.5% for liquid funds. 3.5%-4.5% for money market funds. With the RBI increasing rates, the Yield to maturity (YTM) of the funds have also inched up. Liquid fund YTMs are over 4.5% p.a. Money market YTMs are ~5.5% p.a. And this is before the most recent RBI repo rate hike on June 8, 2022.

#2 Consider Target Maturity ETFs/index funds/Fund of funds

With Target maturity products (TMF), the life of the fund is finite. For instance, Bharat Bond 2030 ETF/FoF will mature in April 2030. The AMC will return your money on the day of maturity.

By investing in such products, you can lock-in your returns (YTM on the date of investment) to an extent. For instance, the YTM of Bharat Bond 2030 ETF is 7.72% (as on June 13, 2022). If you invest today and hold until maturity, you will earn a return, which is closer to 7.72% (before adjusting for expenses and tracking error). Besides, the interest rate sensitivity goes down as the time goes by since you move closer to fund maturity.

Contrast this with most debt mutual funds that have infinite lives. The modified duration (or the interest rate risk) never goes down. For instance, a constant maturity gilt fund will always have average maturity of ~10 years. Hence, the interest rate risk never goes down.

For more on merits and risks in Target maturity funds, refer to this post on Bharat Bonds.

A note of caution: Even fixed maturity plans (FMPs) can be called target maturity products. But those are active funds and can be misused by AMCs to dump poor quality bonds from other schemes.

When I refer to TMFs, I refer to debt ETF/FoFs that replicate the performance of a debt index. For instance, Bharat Bond 2030 ETF tries to replicate the portfolio and performance of Nifty Bharat Bond Index -April 2030. You have a better idea of the kind of securities the fund will own.

Additionally, target maturity funds can be volatile in the interim since many of these are medium to long duration. If the interest rates rise further, the fund NAV will fall. However, if you hold until maturity, you will earn the fund YTM (yield to maturity) as on the date of investment. Allow provision for fund expenses and tracking error.

Therefore, invest in TMFs only if you are comfortable with interim volatility and plan to hold for the long term, preferably until maturity.

Which Target maturity fund to pick?

If you look at the yield curve earlier in the post, 4-5 year maturity is the sweet spot. Also, look at the maturity dates and the YTMs. Good if you can match maturity date with a cashflow requirement. Higher YTM is better but the longer maturity TMFs will be more volatile. Pick accordingly.

Compare the alternatives

The Government bonds are offering 7.5% p.a. (as you can see in the above table). And these are the safest bonds out there.

You can simply buy treasury bills/government bonds through your broker (non-competitive bidding) or through RBI Retail Direct facility.

You can also look at RBI Floating rate bonds. Floating rate bonds. NSC interest rate + 0.35%. Currently, these bonds offer 7.15% p.a. (NSC interest rate of 6.8% + 0.35%).

Or if you are a senior citizen, you can consider Senior Citizen Savings Scheme (SCSS) or Pradhan Mantri Vaya Vandana Yojana (PMVVY). Both these schemes offer 7.4% p.a. (June 2022).

For borrowers, the home loan interest rates have gone up sharply (or will go up in the next few months when their loan interest rates get reset). The home loan are floating rate loans. Now, the home loans have been linked to external benchmarks (RBI Repo rate, Treasury bill yields). Hence, the increase in loan rates will be quite swift.

On the other hand, the bank FD rates have not gone up after the Repo rate hikes. ICICI Bank currently offers 5.1% p.a. on 1-year Fixed deposit. The Government is paying more for 1-year borrowing.

Here are the results of treasury bill auction done by the Reserve Bank on June 8, 2022.

So, the Government is borrowing for 1 year at 6.12% p.a. and the biggest banks offer about 5% p.a. for 1-year fixed deposit. Clearly, the banks are not as safe as the Government.

Then, how could that be? By the way, this has been the case for many months now (since mid-2020).

Well, the banks have different drivers than just the RBI repo rate. Competition, demand for credit, liquidity in the system. If the credit growth is slow or if there is excess liquidity in the system, there is no need for the banks to pay more on fixed deposits. I believe the bank FD interest rates will go up but only after a lag.

Additional Links

Image Credit: Geralt, Pixabay

4 thoughts on “Which are the Best Debt Mutual Funds when Interest Rates are rising?”

Thank you very much Deepak for a beautiful article on ‘PRACTICAL Bond Investing’ where you taught me like my college IIM Professor who taught me so well back in 1994. As you know, I am fond of GOVT BONDS as the CREDIT RISK is close to ZERO and my favourite is ‘3-Year RBI BONDS’ which yields 7.059% as per your post. In the above 3-Year Bond, I hope the DURATION of the Bond will be averaging around 2.8 years which means our INTEREST RATE RISK completely disappears after 2.8 years with an Yield of 7.059% and we are going to get the FACE VALUE of the BOND if we HOLD till the Life of the Bond of 3 years. Can you please tell me how much is the COUPON Interest paid yearly for the above bond and the CURRENT PRICE of the BOND as I am bit confused with my calculation? Since the CREDIT RISK is ZERO, I personally feel it’s the best choice currently available compared to TARGET MATURITY BONDS such as “AXIS AAA Bond plus SDL ETF 2026 maturity fund of fund’ where the Bond still invests in 22% Corporate Debts which may be subjected to CREDIT RISK with a good WEIGHTED Coupon of 7.35%. I am ready to forego a 1% YIELD with Targeted Maturity FoF compared to GOVT 3-YEAR BOND where I will get back my piece of mind with prompt Coupon and Face value payments. Please correct if I am wrong in any of the above wordings. Thanks

Thanks Saravana.

For any bond, the duration risk (interest rate risk) goes down with time as you move closer to maturity.

So, if you buy a bond today YTM of 7% and hold until maturity, you will earn 7% from that bond. Pre-tax ofcourse.

Yield will change every day. Hence, can’t pinpoint.

In case of Target maturity funds, the benefits are that you control interest rate risk to an extent. The risk goes down with time. Most are passive funds. You get indexation benefit. Can lock in yield (to an extent). But there were will tracking error and expenses.

The Govt. bonds are safer but you will have to pay tax on interest income.

Thanks Deepesh for your fast response and appreciate for your clarification. Yes, the Coupons in Govt Bonds are received on a yearly basis and is subjected to Tax whereas in Target Mutual Debt Funds, the Interest is re-invested and so we have an advantage of ‘Indexation Benefits’ that saves TAX. I hope you will write a separate article on “ZERO-COUPON GOVT BONDS” where we can take the advantage of ‘Indexation Benefits’ similar to Target Mutual Funds which will be a better option post-tax returns with ZERO Credit Risk. Kind Regards – Bavan

As always a great article to know about mutual fund investing…. I have query wrt a particular mutual fund though this article is in general to all…

I have a daughter whos is 2 year old and want to start investing in mutual fund and one of my friend suggested to go for UTI CCF mutual fund and choose scholarship option in which I will get tax benefit on maturity. I searched a lot but hardly found any article related to this MF. Can you suggest is this a good option? Should I invest in it only for tax saving or this MF is good in terms of returns also?

Thanks