Want to construct your portfolio completely with index funds? Or want to construct the “Best portfolio” using index funds or ETFs?

How would you do that?

Good that there are many options available in the passive investing space. There are cap-based indices (Nifty 50, Nifty Next 50, Nifty Midcap 150 etc) and there are factor indices (Momentum, Low Volatility, Quality, Value etc).

Having such options is fine but how would you construct a portfolio with such indices?

How much weightage would you give to each of these factors in your portfolio? Which are the best factor index funds or ETFs?

In this post, let’s find objective answers to the above question, albeit with many caveats. In other words, we will find, based on past data, the “Best portfolios” based on your requirements.

Which index funds or ETFs to consider?

We consider the following (price return) indices.

- Nifty 50 index

- Nifty Next 50 index

- Nifty Midcap 150 index

- Nifty 100 Low Volatility 30 index

- Nifty 200 Momentum 30 index

- Nifty 200 Quality 30 index

- Nifty 50 Value 20 index (NV20)

- Nifty Alpha Low Volatility 30 index

- Nifty Midcap Quality 50 index

I have written about all these indices in my earlier posts and discussed about their methodologies. Have also compared the performance of these factor indices However, I have been mostly concerned about the performance of indices in isolation. I have not focussed on the interplay or the correlation between the indices. Or if combining 2 or 3 strategies would yield better results. And this is a problem because you wouldn’t best all your money on just a single strategy.

Why?

Because we know that, when it comes to investing, nothing works all the time. Thus, no strategy, no matter how good, will outperform all the time. In fact, there will be times when it will struggle badly. And it is difficult to stick with an underperforming strategy for a long time if you have bet all your money there. You might bail out at just about the worst time.

Now, if we construct the portfolio using two or more of these indices (strategies), it is possible when one strategy struggles, the remaining ones are doing well. This can result in a smooth performance overall and help maintain discipline.

In this post, let’s figure out how to construct a portfolio using a combination of these indices.

Or in other words, what combination of these indices will result in the “Best” portfolio?

I have picked popular cap-based indices single factor indices (Nifty 50, Nifty Next 50, Nifty Midcap 150), single factor indices (Quality, momentum, low volatility, value) and even a multi-factor index (Alpha Low Volatility 30) index. I have tried to pick indices for which we already have index funds or ETFs. The only exception in Nifty Midcap Quality 50 index.

A note about Nifty 50 Value 20 index (NV 20): I didn’t pick a pure value index (Nifty 500 Value 50 index) because its long-term performance has been pathetic. Have chosen Nifty 50 Value 20 even though it is not a pure value index. NV 20 has very high weightage to ROCE (return on capital employed), a metric you would usually associate with a quality stock. So, it is more of a Quality + Value index.

What is the Best Portfolio?

There can’t be one objective definition of the “Best portfolio”. Because all of us have different expectations from our portfolios. While some of us shoot for the highest returns, the others are content with moderate but stable returns.

Some of the desirable features of any portfolio could be:

- High returns (CAGR/IRR)

- Low volatility (Low standard deviation)

- High Sharpe ratio (Sharpe ratio is a measure of risk-adjusted returns. Higher the better)

- Low maximum drawdowns

- High average rolling returns

I have presented a small list above. There may be many other metrics that you would want your portfolio to rank well on. For instance, you may just be concerned about downside deviation.

Additionally, a portfolio may not rank well on all the metrics. For instance, a portfolio/fund may offer the best CAGR but may be the most volatile or may have the deepest drawdowns.

Thus, you first need to decide what you want from your portfolio and can try to optimize the portfolio for that metric accordingly. For instance, the highest CAGR portfolio may be different from the lowest drawdown portfolio.

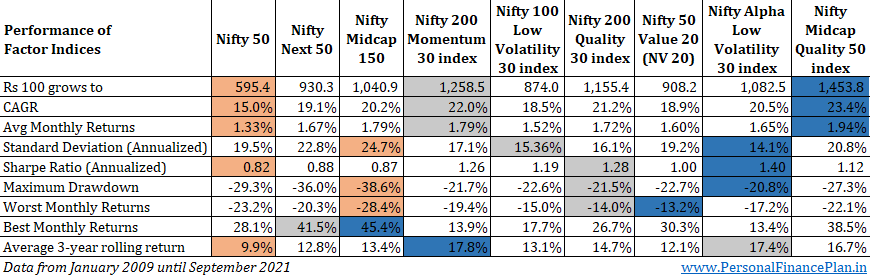

How have the Factor Indices performed?

I compared the performance from January 2009 until September 2021.

Reason: The data for Nifty 50 Value 20 index is available only from January 1, 2009.

I have highlighted the portions as follows:

- Best Performer on a metric: Blue

- 2nd Best Performer on a metric: Grey

- Worst performer on a metric: Pink

You can see, no index has rank 1 or 2 on all the metrics. And this brings us to an important point. Can we improve the performance on various metrics by mixing these indices?

Let’s find out. The first thing to check here is the correlation between the various indices. Correlation is a measure of how various indices move together. A correlation of 1 means that both the variables move together in the same direction. A correlation of -1 means that when one variable goes up, the other goes down and vice-versa.

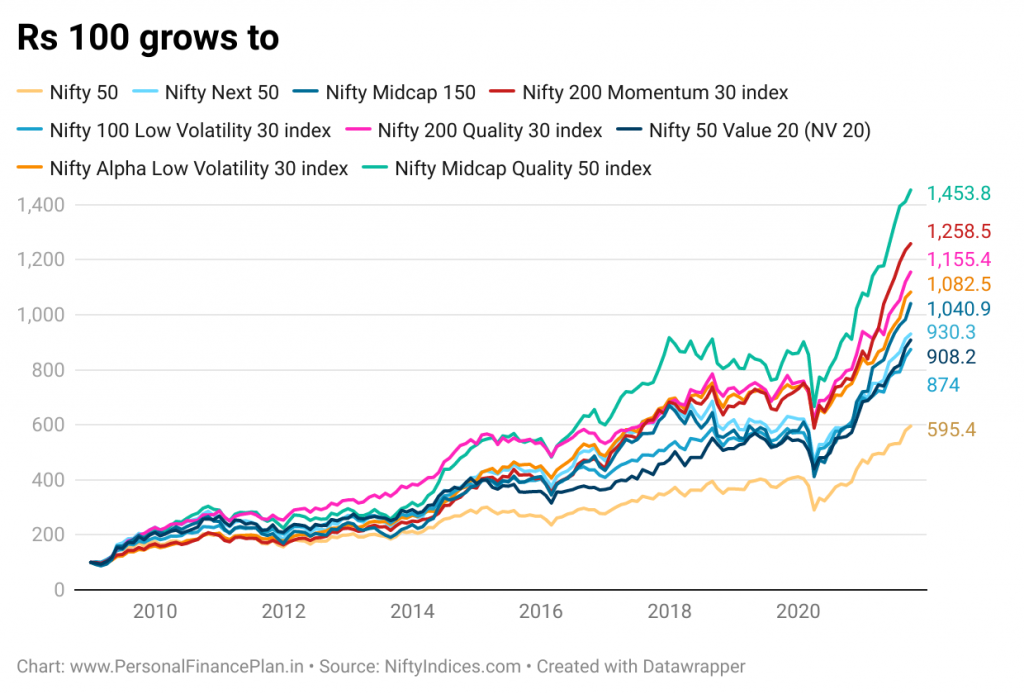

For the sake of completion, I present the “Rs 100 grows to” and rolling returns charts below.

Correlation between the Factor Indices

Note that all these indices comprise of Indian stocks. Hence, would have very high correlation with each other. And you can see this in the table above. Most of the numbers are above 0.8. I have highlighted those below 0.85. Thus, you must appreciate the limitation of a portfolio mix of the above indices. What we test in the remainder of the post is about optimising your domestic equity portfolio.

You can’t rely on a portfolio with a mix of these indices for diversification. For diversification, we need much lower correlation coefficients (than the numbers we see in the above table). And that happens when you mix completely different assets in a portfolio.

For comparison, I present the correlation of monthly returns between Nifty, Gold, Nasdaq 100 index and a debt fund since March 2011. Have used Nippon Gold BeES as proxy for gold. Motilal Oswal Nasdaq 100 ETF for Nasdaq 100 and HDFC Liquid fund for debt fund.

The number are either negative or low positive. And that’s how you diversify a portfolio and reduce portfolio losses. By bringing together assets with negative or low correlation. Now, let’s go back to the main topic.

What do we optimize for?

Your best portfolio combination will depend on the metric you want to portfolio to optimize for. I don’t which is your preferred metric. Hence, we will find optimized portfolios for all the metrics discussed above.

Firstly, we will see the results for each metric for uncapped weights. You can even go 100% to a single index. Negative weights (or shorting) is not allowed.

Then, we take a more practical approach. To avoid going too heavy with a particular strategy, we will cap the maximum weight at 25% and 40%. Or we will find the “Best portfolios” using 2 maximum weight caps.

I have used Excel Solver function to identify the best portfolios for each metric, subject to the weight caps.

I have highlighted the metric being optimized in Blue.

Highest CAGR

The highest CAGR portfolio is heavy on Nifty Midcap 150 Quality 50 index, Nifty Momentum index and Nifty 200 Quality 30 index.

Highest Sharpe Ratio

Heavy on Nifty Alpha Low Vol 30, Quality 30 and Nifty Momentum index.

Lowest Standard Deviation

Heavy on Nifty Alpha Low Vol 30, Nifty Low Volatility 30 index and Nifty Quality 30 index. Nifty Momentum Index also comes in a capped portfolio.

Lowest Maximum Drawdown

This is interesting. Nifty Midcap 150 index had the deepest drawdowns. Still, it commands a good weight in lowest drawdown portfolios. Nifty Quality index and NV20 index are the other prominent players in such a portfolio.

Best 3-year Rolling Returns

Nifty Momentum index is the biggest weight here. In constrained portfolios, Alpha Low Vol 30, Nifty Quality and Midcap Quality index come in.

How do we use the above information?

One surprising finding is that you don’t find any weightage to Nifty 50 in any of the optimized portfolios. Nothing.

Does that make Nifty 50 a bad choice?

No. Nifty 50 is not a bad choice. And I have listed down some of the reasons in the “Caveats” section below.

In a post on How to build a long term portfolio, I mentioned that the core equity portfolio should be built around market-cap based indices. And I stick with that.

Depending on your preference, you can use the “Best portfolios” for the satellite portion of your equity portfolio.

The Caveats (and there are so many of them)

- This is based on past data. There is no guarantee that the past will repeat.

- I have used data for about last 13 years. The results can change if you change the time period. For instance, if we are optimizing on Sharpe ratio, the best combination can change if we use the last 5-year or last 10-year data.

- There is a start point and end point bias. We have used Jan 2009-Sep 2021. The best combinations for any metric will be different for say, Jan 2009-Sep 2020. Or for Jan 2011- Jan 2021.

- Even for 13-year data, the results we have seen for 2009-2021will be different for returns from 2023-2035.

- The calculations I have done assumes monthly rebalancing to target allocation. Quite impractical. Unlikely you would do that. Firstly, it is a lot of work for investors like you and me. Secondly, there will be tax implications. Annual rebalancing is just fine.

- The factor indices have been launched recently. Do not have sufficiently long track record. The good results that we see in the factor indices could be a result of back-fitting. The performance of live indices could be very different. Moreover, the alpha can shrink when serious money chases the indices (or a similar strategy). Cap-based indices such as Nifty 50 and Nifty Next 50 have a long track record.

Therefore, take these findings with a pinch of salt. At the same time, the past data is not completely useless either. Relying on past data is better than crystal-gazing.

How would you use this information?

Which metric do you want to optimize your portfolio for? And which factor indices will you use for your portfolio?

Let me know in the comments section.

Additional Links/Source/Credit

- A tweet from Kora Reddy (@paststat) got me thinking in this direction. I also attended his workshop on building such optimized portfolios, where he patiently explained how to build such models. If you are interested in this topic, suggest you attend the workshop the next time it is organized.

- Which is the Best Nifty Factor Index? By Anoop VijayKumar from CapitalMind

- NiftyIndices