In October 2017, SEBI announced multiple mutual fund categories and announced that each fund house could have just one fund in each category of fund scheme.

An important announcement: www.PersonalFinancePlan.in has been chosen as one of the Top 25 blogs for mutual fund blogs by FeedSpot, a RSS reader. Though such rankings shall always be taken with a pinch of salt, it is always good to see your effort getting recognized. Thank you for the support.

Keep sharing and spreading the word about the blog.

Now, back to the main topic.

What changes has SEBI brought? How do these classifications affect you? Let’s find out the answers in this post.

What does the SEBI circular say?

As per the SEBI circular, there are five broad groups.

- Equity Schemes

- Debt Schemes

- Hybrid Schemes

- Solution Oriented Schemes

- Other schemes (for index funds, ETFs and Fund-of-Funds)

Within each group, there are multiple categories.

For instance, equity has 10 categories (multi-cap, large cap, Large and mid cap, mid cap, Small Cap, ELSS etc). Debt has 16 categories, Hybrid has 6 while solution oriented and others have 2 categories.

And each fund house can have just one scheme in each category. There will be exceptions in case of.

- Index Funds/ ETFs replicating/ tracking different indices; (i.e. you can have multiple index funds, one tracking say Nifty 50, the other tracking Nifty Next 50 etc)

- Fund of Funds having different underlying schemes; and

- Sectoral/ thematic funds investing in different sectors/themes (a fund house can have banking fund, a pharma fund, an IT fund etc)

You can go through the circular here.

Definition of Large Cap, Mid Cap and Small Cap Company

Earlier, SEBI had not defined what constituted a large cap, mid cap or a small cap company. Therefore, it was not uncommon to see a large cap equity mutual fund to take a significant exposure or a mid cap fund taking a good exposure to large cap companies.

Additionally, there was no classification what was a large cap, mid cap or a small cap company.

Now, SEBI has given the definition for various types of companies.

Large Cap Company: 1st-100th company in terms of full market capitalization

Mid Cap Company: 101st-250th company in terms of full market capitalization

Small Cap Company: 251st company onwards in terms of full market capitalization

Well Defined Categories

SEBI has defined various categories under the 5 aforesaid groups.

For instance, an equity scheme can belong one of the 10 categories defined by SEBI.

SEBI has also defined asset allocation (scheme characteristics) for different kinds of schemes.

I copy an excerpt from SEBI circular (for 5 out of 10 categories under equity) for your perusal.

As you can see, a large cap fund needs to hold at least 80% of its asset in stocks of large cap companies.

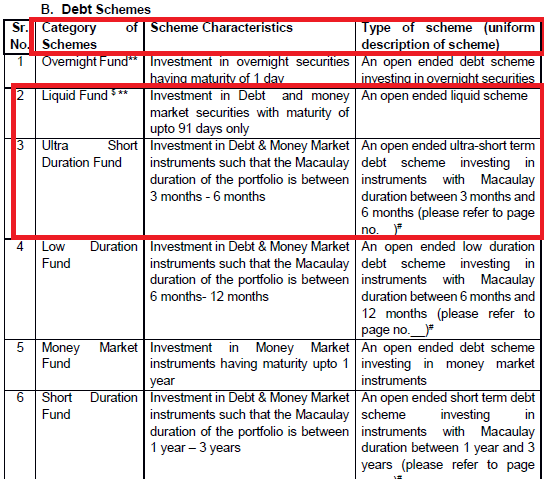

What about Debt Funds?

In my opinion, retail investors are more likely to commit a mistake in picking up a debt fund as compared to an equity fund. There are many risks involved in investing in debt funds that many investors just ignore.

In this light, these regulations can add some value (not much but still reduces confusion). In fact, the circular puts restrictions on where the fund house can invest under various categories.

For instance, in a liquid fund (a category under debt funds), the fund manager can invest only in securities that are maturing in up to 91 days.

In an ultra short duration fund, Macaulay duration of the portfolio has to be between 3 months and 6 months. Duration is a measure of interest rate sensitivity of a debt portfolio. Higher the duration, greater the interest rate risk. I have discussed this aspect in this post. For more on Macaulay duration, go through this article on Investopedia.

A credit risk fund will invest atleast 65% of the assets in securities that are rated less than AAA (highest rating). By the way, fund houses used to call such funds credit opportunities fund (Notice the focus on reward and not risk. No such category now).

I copy an excerpt from SEBI Circular.

Frankly, there was no such term as an ultra short duration fund before. We used to have Ultra Short Term debt funds (btw, this was not a definition by SEBI). However, the fund manager used to have good leeway in deciding where to invest. It is good that there are clear restrictions.

What about Balanced Funds?

SEBI has clearly defined asset allocation for hybrid funds. Existing balanced funds will qualify as Hybrid funds.

As with equity and debt funds, there are multiple categories under the group of Hybrid funds.

An excerpt from SEBI circular.

There is no such category as Monthly Income Plan (MIP). This nomenclature was deliberately misleading. So, this is a relief. Now such funds will have to be categorized as Conservative Hybrid Funds.

There is Balanced Hybrid Fund category with up to 60% asset allocation. Remember this will not qualify your investment for equity taxation (minimum 65% equity exposure is required for tax-free gains after 1 year). No arbitrage is allowed in such schemes (in my opinion, that rules out any possibility of equity taxation).

Then, there is Aggressive Hybrid Fund category where equity allocation can be between 65% and 80%. This will qualify for equity tax treatment.

A fund house can have either a Balanced Hybrid Fund or Aggressive Hybrid Fund category.

I believe fund houses will opt for Aggressive Hybrid Fund Category i.e. classify their existing balanced schemes as aggressive hybrid fund category to maintain equity taxation.

What will happen to your scheme?

One of the following may happen:

- Your fund may continue as it is (or some other scheme gets merged with your fund scheme).

- Your fund may be wound up. (Quite unlikely. More likely to be merged with another scheme).

- Your fund scheme may get merged with another scheme in the same category. For instance, your large cap fund may be merged with another large cap fund from the fund house.

- The investment objective of your fund may change. A fund house can do this to avoid the scheme getting merged with another scheme, especially if both the schemes are quite big and successful.

Even though it is pointless to break your head till such time you know the status of your scheme, I will be vary of Option no. 4.

What are the implications for you?

In my opinion, it is a good move for the investors. Fund houses used to have multiple schemes under the same category and made it really confusing for the investors. It is not uncommon to see multiple large cap, multi-cap or midcap funds from the same fund house.

Many investors use platforms such as MorningStar, ValueResearch for their fund research. However, with everything so subjective, it was always difficult to compare. Benchmarks had almost become meaningless. For instance, it is not right to compare a purely large cap fund that sticks to say Nifty stocks to another large cap fund that is investing heavily in midcaps.

Different portals may classify a scheme differently. Scheme A may be a large cap fund according to one portal while another platform may define it as a multi-cap fund.

Now, with crisp classification (category) in place, at least such confusion won’t be there. It should get easier for investors to compare funds.

Moreover, it always helps to know where your fund is going to invest. In some way, it should help you select the right funds for you.

At the same time, 36 categories (in total) is still quite a few. 16 categories in debt funds is likely to confuse investors a bit. I do not also agree with description of some categories. The SEBI order applies only to Open Ended Funds. As I understand, AMCs can continue to launch close ended funds with impunity. Fair bit of mis-selling happens with close-ended funds.

A very good start nonetheless.

Will there be any tax liability?

It is possible that your scheme (say Scheme A) may get merged with another scheme (say Scheme B). In that case, you will be given an option to shift to Scheme B. If you take this option, there will not be any tax liability in your hands. Moreover, subsequently, when you decide to exit Scheme B, the date and cost of investment in Scheme A will be considered for tax liability.

In case you do not want to shift to Scheme B, you can exit that investment. However, in that case, you will face exit load and capital gains tax implications.

How long will this take?

SEBI has given fund houses 2 months to review their schemes and submit proposals for merger,closure, fundamental attribute change etc. to SEBI. Once SEBI issues observations, AMCs will get 3 months to carry out the changes. So, expect this exercise to stretch over 6-12 months.

Additional Read

SEBI Circular on Categorization and Rationalization of Mutual Fund Schemes

LiveMint: Regulation 3.0: Indian Mutual Funds

LiveMint: Five Takeaways from SEBI’s order on Mutual Fund Schemes

9 thoughts on “Categorization of Mutual Fund Schemes by SEBI”

Thanks Deepesh , I was waiting for this writeup for some time.

Congratulations on Personal Finance being selected as Top 25 Mutual Fund Blog , This is well deserved recognition for your hard work.

On SEBI Cicular this is a good move by SEBI has now we have clear demarcation on the duration for Debt Fund now specially the upper limit. of duration.

A query I had here will Short Term GILT and Long/Medium Tem GILT Term will survive in Debt Category , considering short duration fund now has a term limit of 3 years and that is the last category of Debt Fund mentioned in SEBI Circular . What about those 10 years GSEC ?

Thanks Austin!!!

In my opinion, the last word is yet to be written in this saga.

Frankly, am as clueless as you are.

There are only two categories of gilt funds. One that allows across maturity and one that has 10 year duration (don’ know how they will keep it constant at 10). No place for short term gilt funds.

Suggest we wait and see this pans out.

Thanks Deepesh

Hi Deepesh,

Can you suggest ICICI Balanced advantage fund-direct will be under which category?

Hi Shiv,

It is a dynamic asset allocation fund. So, should fall in dynamic asset allocation or balanced advantage fund.

it cannot be equity savings fund? and what is the difference in balanced advantage and equity savings, i feel both are same?

equity savings keeps lower net equity exposure. Ensures equity taxation through use of derivatives.

Dynamic asset allocation funds change exposure depending upon market conditions (or their perception of market conditions). Equity exposure can range from 0% to 100% depending upon fund mandate.

I have invested some amount in ELSS which completed lock in period. Can i switch market value amount of invested in same ELSS fund? Is it consider as 80 C tax saving instrument?

How do you switch into the same fund?

If you meant selling units and reinvesting those, you can do that.