In Budget 2021, the Government had introduced a tax on interest on employee contribution to EPF over Rs 2.5 lacs in a financial year.

The Government rationale was that many HNIs were taking benefit of tax-free interest by contributing heavily to the employee provident fund (EPF) account. Read this Economic Times article for more details. The Government feels it is not right that the HNIs receive the benefit of such tax-free interest.

Back to basics. There are two ways in which you contribute to your EPF account.

- Own contribution (Employee contribution). Qualifies for tax benefit of up to Rs 1.5 lacs under Section 80C of the Income Tax Act. The rule changed introduced in Budget 2021 applies only to own contribution to EPF account.

- Employer contribution (your employer contributes to your EPF account). Also qualifies for tax benefit.

The Central Board of Direct Taxes has recently notified how your EPF contribution over Rs 2.5 lacs in a financial year will be taxed.

How will your EPF contribution above Rs 2.5 lacs be taxed?

Going forward, there will be 2 partitions in your EPF account for own contribution. Employer contribution is separate.

#1 Taxable EPF Contribution Account

Your contribution to your EPF account up to Rs 2.5 lacs per annum goes to this account.

If your employer does not contribute to your EPF account, then this threshold of Rs 2.5 lacs is increased to Rs 5 lacs.

Interest earned in this account is exempt from tax.

#2 Non-Taxable EPF Contribution Account

If your annual contribution to the EPF account exceeds Rs 2.5 lacs (or Rs 5 lacs as the case may be), then the excess portion goes to this account.

Interest earned in this account is taxable. The interest income on this shall be considered “Income from other sources”. TDS is also applicable if such interest income during the year exceeds Rs 5,000.

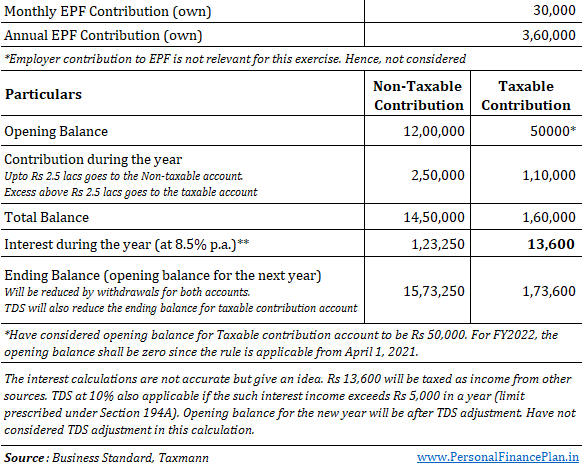

Here is an illustration.

Points to Note

- We can see that “Interest on Interest” is taxed. Earlier, there was confusion about this. Continuing from the illustration, Rs 13,600 was the annual interest in taxable account. Gets added to ending balance or the opening balance for the next year. Thus, any interest on this interest will also be taxed.

- The above calculation is only for your contribution to EPF account. The rule change does not affect how employer contribution is taxed.

- There is TDS if the interest income (on taxable contribution account) exceeds the threshold under Section 194A. If TDS does not cover the entire tax liability, you will have to pay the deficit as advance tax or while filing ITR. TDS will affect compounding slightly.

- The taxable interest will be considered “Income from other sources). Since the EPF investments are not liquid, you will have to pay tax from own pocket.

- If you need to withdraw from EPF, it is better to withdraw from the taxable contribution account.

Does the EPF tax affect EPF as an investment?

EPF has been an excellent long term fixed income product.

Zero risk. High tax-free interest rate.

And it remains that way for most investors. Not many would be affected because of this change in rule.

Rs 2.5 lacs per annum means monthly contribution of Rs 20,833. So, if you are contributing up to Rs 20,833 per month, you are not affected by this change.

Assuming you contribute 12% of your basic salary, your basic salary should be Rs 1.73 lacs per month to breach Rs 20,833 in monthly EPF contribution. Annual basic salary of Rs 20.83 lacs. Not a small amount.

Mathematically, it seems unlikely that a taxpayer in lower than 30% tax bracket will be affected by this rule (unless the investor is contributing heavily by way of VPF).

However, if you are one of the very few who are affected, what should you do?

If EPF pays 8.5% p.a. (assumption), then the post-tax return shall be 5.95% p.a. on the excess amount. In current times of low interest rates, this does not look bad. Other safe fixed income products will find it difficult to provide such returns on a post-tax basis.

At the same time, the bar for the competing fixed deposit products goes down. Earlier, their competition was 8.5% p.a. (assumed). Now, those products have to beat 5.95% p.a. on a post-tax basis. Easier than 8.5% p.a. but still not easy.

However, times can change. It is possible that other investments (say debt funds) may be able to provide higher post-tax returns than taxable EPF in the future. However, at that time, you will not be able to take money out of EPF. Hence, this complicates the decision. And we shouldn’t just compare the products on their return profile but also the risk profile. For instance, most debt funds carry both credit risk and interest rate. Gilt debt funds don’t carry credit risk but carry interest rate risk.

As things stand today, you should continue to contribute towards EPF even if your annual contribution breaches Rs 2.5 lacs. Not that you can do much about it. Restructuring your salary to reduce EPF contribution may not be a good idea. I discuss the reasons later in this post.

By the way, if you do not have a PPF account yet, open one. PPF continues to provide tax-free interest. If you are planning to contribute say 3.5 lacs to your EPF account (including VPF), you can put Rs 2.5 lacs in EPF and Rs 1 lac in PPF. PPF will offer better returns than the taxable portion of EPF.

What about VPF (Voluntary Provident Fund)?

The rule change certainly brings down the attractiveness of VPF. Therefore, if your regular contribution is already breaching Rs. 2.5 lacs per annum, you may want to reassess your position about VPF.

I am not saying you should not invest in VPF but the attractiveness has certainly come down if you breach the Rs 2.5 lacs annual limit.

Should you restructure your salary?

There is an option to restructure your salary, reduce your basic and thus bring down contribution to EPF account. For most employees, this is not a good idea because there are a few benefits that are linked to your basic salary. Such benefits will also go down.

For instance, employer contribution to EPF account will also go down. EPF employer remains exempt until Rs 7.5 lacs. Let’s say employer was contributing Rs 4 lacs to your account. You restructure salary so that the employer contribution comes down to Rs. 2.5 lacs. The excess (Rs 4 lacs – Rs 2.5 lacs = Rs 1.5 lacs) will be paid as salary and will be taxed. Earlier, this 1.5 lacs would have gone to your EPF account and earn tax-free income. Now, you will pay tax of 45K (30% tax bracket) and get only Rs 1.05 lacs in your bank account. Unnecessary hit.

Reducing your basic salary can also impact other tax benefits such as HRA (House rent allowance).

Additional Links

How to calculate taxable of interest on PF contribution? (TaxMann)

Your EPF account will now show taxable and non-taxable balance (Business Standard)

If you want to know what happens to your EPF account if you don’t contribute to it, read this excellent post from Sreekanth.

Addendum

I had written this post in February 2021. Have modified the post (in September 2021) after clarification from CBDT. Still retaining below what I wrote in February 2021. Has many interesting points.

What has not changed?

#1 Your contribution to EPF (above Rs 1.5 lacs) comes from post-tax income (It always did!)

Any investment (your contribution) into EPF above Rs 1.5 lacs goes from your post-tax income. The tax benefit under Section 80C is capped at Rs. 1.5 lacs. Thus, any Section 80C investment/expense more than Rs 1.5 lacs comes from your post-tax income. Or to put it in a different way, the excess investment above Rs 1.5 lacs does not help you save tax.

Two points

- EPF is not the only Section 80C investment. There are other competing products too such as PPF, ELSS, insurance etc. The cap of Rs 1.5 lacs per financial year is for all such investments/expenses combined. So, if you put Rs 60,000 in ELSS every year, then only Rs 90K of your EPF contribution saves you tax. Or if you are investing Rs 2 lacs in EPF, then 50K of EPF and 60K of ELSS is not helping you save any tax.

- That investment above Rs 1.5 lacs comes from post-tax income does not make EPF a bad investment. Why? Firstly, because any other investment that you make will come from your post-tax income. Secondly, EPF gives you tax-free interest income and tax-free maturity proceeds and remains an excellent fixed income investment for retirement.

#2 Nothing changes for your contribution until March 31, 2021

The change in tax rule shall apply only from April 1, 2021.

Your contribution until March 31, 2021 (irrespective of the amount) shall continue to earn tax-free interest even after March 31, 2021 (until maturity).

#3 Employer contribution more than Rs 7.5 lacs comes from post-tax income. Interest on such excess portion taxable too.

This rule was changed last year (Budget 2020).

Earlier, the employer contribution to your EPF account came from pre-tax income i.e., you got tax-benefit if your employer contributed to your EPF account. And the interest income on such portion was also exempt from tax.

In Budget 2020, the Government capped this tax benefit.

If the employer contribution (cumulative) to your EPF, NPS or superannuation account exceeded Rs 7.5 lacs in a financial year, the excess portion will be added to your income and taxed at your slab rate.

In addition, the interest that you earn on such excess amount is taxable too.

Now to what has changed.

What has changed?

#4 The interest on your contribution above Rs 2.5 lacs shall be taxable.

If you contribute more than Rs 2.5 lacs per financial year, then the interest earned on this excess amount will be taxable.

Let us say you contribute Rs 35,000 per month to EPF account in FY2022. That makes it Rs 4.2 lacs in a financial year.

That is Rs 1.7 lacs extra.

The difference comes in how the interest is taxed.

- Earlier, the interest income on the entire Rs 4.2 lacs would have been exempt from tax if you continued to work.

- Now, the interest only on the first Rs 2.5 lacs will be exempt from tax. The interest on the excess Rs 1.7 lacs will be added to your income and taxed at the slab rate.

- Note that the interest won’t be taxed in just the first year. The interest on such excess will be taxed every year. Thus, the interest earned on this Rs 1.7 lacs will be taxed every year.

Point to Note

- This new rule applies only to your contribution (employee contribution).

- Includes both mandatory and voluntary (VPF) contribution.

- This new rule does not apply to employer contribution. Rules pertaining to employer contribution were changed last year (Budget 2020). Referred in Point #3.

- Note that your contribution above Rs 1.5 lacs (Refer to #1) always came from post-tax income. Hence, no change in this regard too.

- This rules only changes how the interest income on your EPF contribution exceeding Rs 2.5 lacs will be taxed.

- EPF and PPF are different products. Nothing changes about PPF taxation.

Will the interest on interest on the excess amount also be taxed?

Continuing with the above example, Rs 1.7 lacs was the excess amount of own contribution.

Assuming EPF fetches 8%, Rs 1.7 lacs * 8 % = Rs 13,400

Now, will the interest on this Rs 13,400 be taxed in the coming years?

While we should wait for clarity in this matter from the Income Tax Department, in my opinion, such interest on interest will also be taxed. Otherwise, the purpose behind the change will be defeated.

I copy commentary from the Finance Bill, 2021 about the proposal and proposed change in the Income Tax Act. Section 10 of the Income Tax Act contain clauses to exempt income from EPF.

Commentary

Clause (11) of the said section provides for exemption with respect to any payment from a provident fund to which the Provident Funds Act, 1925 applies or from any other provident fund set up by the Central Government and notified by it in this behalf in the Official Gazette.

Clause (12) of the said section provides for exemption with respect to the accumulated balance due and becoming payable to an employee participating in a recognised provident fund, to the extent provided in rule 8 of Part A of the Fourth Schedule.

It is proposed to insert a proviso to such of the aforesaid clauses so as to provide that the provisions of these clauses shall not apply to the income by way of interest accrued during the previous year in the account of a person to the extent it relates to the amount or the aggregate of amounts of contribution made by that person exceeding two lakh and fifty thousand rupees in any previous year in that fund, on or after the 1st day of April, 2021 and computed in such manner as may be provided by rules.

Proviso to be added after Clause 11 and 12 of Section 10

“Provided that the provisions of this clause shall not apply to the income by way of interest accrued during the previous year in the account of a person to the extent it relates to the amount or the aggregate of amounts of contribution made by that person exceeding two lakh and fifty thousand rupees in any previous year in that fund, on or after the 1st day of April 2021 and computed in such manner as may be prescribed;”;

Since Rs 13,400 is related to the excess over Rs 2.5 lacs, the interest on Rs 13,400 shall be taxable too in the future.

Hence, you can think of your EPF balance being divided into 3 parts.

- Exempt employee contribution

- Taxable employee contribution (excess over Rs 2.5 lacs per year after April 1, 2021 to be kept in this account). Interest on such excess shall also be added back to this account.

- Employer contribution (guess this can be divided into two parts too. One for less than 7.5 lacs and one for the excess).

7 thoughts on “EPF Tax: How will your EPF contribution above Rs 2.5 lacs be taxed?”

Excellent Deepesh,very clearly explained as always..

Anyway no guarantee that govt will leave that option also in future about PPF..

If NPS is there ,then is it better to invest the extra amount here (if contributed via VPF)?

Thanks Sreenivas!

NPS and EPF are very different products.

Hence, do not have a black and white answer.

NPS has its own host of issues.

Well explained.

This happen when we attempt to take advantage of the scheme. Although I am unable to understand how few could contribute VPF in crores as any investment in PF is supposed to be part of salary earned and VPF is also accepted basis declaration of the employee as percentage of salary earned.It

Thanks Rakesh.

Higher salary, Higher basic. Then, through VPF, you can contribute up to 100% of your basic in EPF.

Hi Deepesh,

They are using all sorts of avenues to tax salaried employees while not doing anything to catch the real tax evaders who are among the businessmen and professionals.

In this case they should have allowed a voluntary limit on PF contributions to 2.5 Lacs rather than the mandatory 12% contributions on basic salary.

Why would one mandatorily want to contribute more than 2.5 Lacs knowing that the interest above that will be taxed?

Hi Pradeep,

I understand. Investing a lot of money into EPF won’t be as advantageous as it used to be.

Sir

I need your clarification and suggestions on below. I’m briefing my case as under

I have opted VRS on 31.01.2020 and upto 31.01.20 I was an employee of the company… Since our PF is in company officers Trust, we have been informed that we can keep the corps (pf contribution + intrest) as on 31.01.20 with the trust till 63 years of my age.. and this will earn intrest as declared by the Government time to time. Hence I have not opted to withdraw during my VRS. Also we were told that after 31.01.20, the total corps will be treated as FD. .

For the FY 20-21, govt has declared 8.5 percentage intrest and the corps as on 31.03.20 will be treated as principle.

My worry is since the corps is treated as FD the intrest earned is liable for tax and needs to be paid during this assessment year and otherwise I have to pay intrest on due tax till it is paid like past instances..

I request your views on this and adviceon tax liabilities as well to prevent paying intrest on tax..

Thanks n regards muthuswamy

Show quoted text