There is a BIG difference between financial planning for retirement (accumulation phase) and financial planning during retirement (decumulation phase).

Let’s look at what I mean. In this post, I will limit the discussion to investments.

Financial Planning for Retirement (Accumulation Phase)

During this phase, you are trying to accumulating funds for retirement. Quite clearly, this phase is BEFORE retirement.

- You do not withdraw from your portfolio.

- Volatility can be your friend.

- Rupee cost averaging (through SIPs or regular investing) works in your favour, if markets move up over the long term.

- You do not mind lower asset prices (or market corrections) in the interim so long as things get fine by the time you retire.

Financial Planning During Retirement (Decumulation Phase)

During retirement (decumulation phase), you have to rely on your portfolio for your income.

- You have to withdraw from your portfolio to meet your expenses.

- There are no further fresh investments.

- Volatility can be a serious enemy.

- You are subject to Sequence of Returns Risk. We will come to it later.

- Rupee cost averaging can go against you. Again, we will come to it later.

- Sharp market corrections during the early part of your retirement can destroy you financially.

What is Sequence of Returns Risk?

You need to worry not just about long-term average returns.

You need to worry about the sequence of returns too.

Since you are withdrawing from the portfolio at the time market is going down, the portfolio may deplete quite quickly. And this gives rise to another problem.

If your portfolio is depleted beyond repair, there may not be much left when the good sequence of returns comes around.

Reliance on long-term average returns is fine when you are in the accumulation phase. During retirement, do not undermine the importance of sequence of returns.

Illustration

Let’s try to understand with the help of an example.

Let’s assume you have just retired at the age of 60.

- You have planned for another 30 years until the age of 90. Nobody knows how long they are going to live but you can add 10-15 years to the age your grandparents/great grandparents passed away to begin.

- You need Rs 50,000 per month. You will need Rs 6 lacs per annum.

- There is no inflation. 0% inflation. Illogical but please play along.

- You live in tax-free society. There are no taxes.

With these assumptions, you will need Rs. 50,000 X 12 months X 30 years = Rs 1.8 crores to last your retirement. I have assumed 0% return on your portfolio.

Let’s tinker around with the return assumption.

Let’s now assume there is just one asset class, equities, that has given long-term returns of 10% per annum (and will continue to do so). Illogical again. Play along.

You withdraw from your corpus at the start of the year to provide for the rest of the year.

With these assumptions (0% inflation, 10% return and withdrawal at the start of the year), you need Rs 62.2 lacs for your retirement (down from Rs 1.8 crores at 0% return assumption).

Scenario 1 (Constant returns of 10% p.a. every year)

Looks good, doesn’t it? Everything is hunky-dory.

Every year, you earn a return of 10% p.a. Your corpus is over in the 90th year.

Aren’t we ignoring something?

Do you really expect to earn 10% in every year?

In real life, returns are not constant. Even though long-term average may be around 10%, it does not mean you will earn 10% every year.

What if you are unlucky and retire during the bad patch in markets?

You don’t control it, do you?

In the following example, I have chosen returns for a few years so that long-term average return that you earn is 10% p.a. but the initial few years are bad for markets.

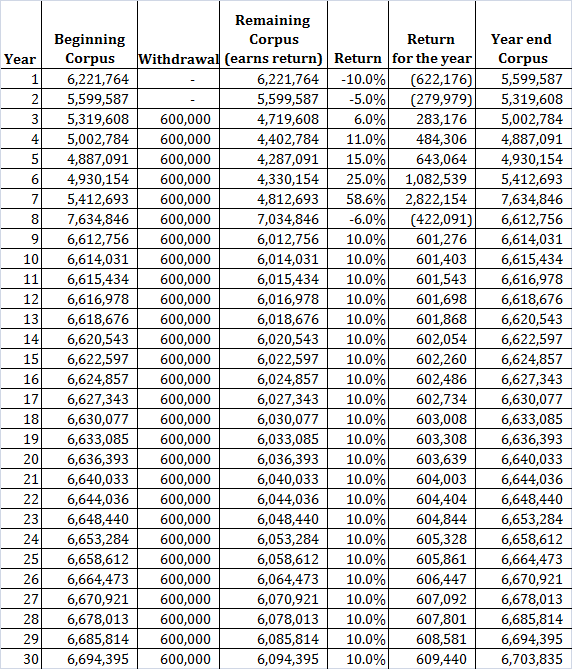

Scenario 2 (Non-constant returns, Long-term average intact)

Your portfolio is depleted in the 18th year. What do you do for the remaining 12 years?

Please understand I have chosen the sequence of returns to demonstrate my point. For another sequence of returns, your portfolio may have lasted for more or fewer number of years. With a favourable sequence of returns, you may even be looking at leaving an estate for your heirs.

For instance, if you swap the returns for 1st and 7th years (-10% and 58%), you will end up with Rs 1.1 crores at the end of 90 years.

What does this tell you?

If you face adverse market conditions in the earlier years, your portfolio may not last the planned term.

Why did this happen?

This happened because you were withdrawing from the corpus at the same time.

Rupee cost averaging works in the reverse direction. You have to REDEEM MORE units at LOWER prices to maintain the level of income. That’s why SWP from equity funds is a bad idea.

Therefore, your losses became permanent.

By the time good sequence of returns came around, the damage had already been done.

For instance, under constant returns scenario, you were to be left with Rs 61.5 lacs at the end of 2 years. In the scenario we considered, you are left with only Rs 42.3 lacs. Over 30% less.

Your withdrawal rate has shot up sharply.

If you compare, in the third year, you are withdrawing ~10% of your portfolio in constant returns scenario while in the second case, you withdraw almost 15% of your portfolio.

Finished.

Do note I considered 0% inflation. With a positive inflation, the situation would have been even worse.

What can you do to guard against Sequence of Returns?

Clearly, you don’t control the sequence of returns. However, here are a few things you can build into your retirement planning.

- Target a much bigger corpus that can withstand sharp losses. While calculating retirement corpus, be conservative about the rate of inflation (higher is better) and return expectation (lower is better).

- Plan for a greater number of years (40 instead of 30).

- Reduce withdrawals for a few years. Quite impractical.

- Work part-time during retirement. If you avoid withdrawals (or reduce withdrawals) from your portfolio even for a few years, it will have a serious impact on the longevity of your portfolio.

For instance, continuing with the same non-constant returns scenario but no withdrawals for the first two years,

Scenario 3 (Non-constant returns, Long-term average intact, No withdrawals for the first two years)

You can see, by not any withdrawals for the first two years, you are left with a nice change of Rs 67 lacs at the end of 30 years. You avoided withdrawing in the bad years. Therefore, your corpus was still around when the good set of returns came.

- You can review your portfolio at regular intervals. If you think you are struggling, it may be time to pick a part-time job to reduce withdrawals from the portfolio. May be easier to go back to work during early part of retirement.

- Use asset allocation techniques to balance between growth (inflation protection) and income portion of your portfolios and reduce volatility at the same time. Very subjective.

- Purchase annuity at the right time to take care of longevity risk.

I have discussed about the sequence of returns risk and how you can reduce such risk in detail in this post.

Would things have been any different if this happened during Accumulation Phase?

If you encountered a bad sequence of returns while saving for retirement, how would you have fared?

Let’s assume you invest Rs 6 lacs on the first day of every year for 30 years.

At constant returns of 10% per annum, you will end up with Rs 10.8 crores.

For non-constant returns as shown earlier, you will end up with Rs 12.47 crores.

Yes, you end up with a larger corpus.

This happened because you earned the higher returns on a much bigger corpus. I have discussed a similar case in another post.

Do note this will not always happen. This is for a specific sequence of returns. The results may reverse for another sequence especially if poor returns come towards the end of the accumulation phase.

Therefore, volatility can be a friend during the accumulation phase (there is no guarantee though). Since you are still contributing, your get greater number of units during the downturn. This rewards you when the markets turn for the good later.

Apart from that, you can make adjustments along the way during accumulation. For instance, you can increase investments if you feel you will struggle to reach the target retirement corpus.

No such luxury during retirement (decumulation phase).

This post was first published on June 17, 2017 and has been updated since.

11 thoughts on “Financial Planning for Retirement vs. Financial Planning after Retirement”

Very well written. The complex problem statement is explained in a very lucid way. Keep up the good work.

This is the problem with the metric of average return or CAGR return. Looking at CAGR makes sense if lump sum (one time investment) is invested over a long time period in which case sequence of returns doesn’t matter. One early bad year compensates another later good year and vice versa in the former case. However when the sum invested ( or withdrawn) over the period increases ( or decreases), the sequence of returns do matter both in accumulation and decumulation phases. It’s not like that sequence of returns do matter most in decumulation phase than in accumulation phase. The catch, I guess, here is the sequences matter (or operate) in reverse directions. In accumulation phase, the bad returns towards the end of the invested horizon impact (less or negative returns on higher corpus at the end) the investor most whereas in decumulation phase the bad returns at the beginning of the corpus withdrawal impact the investor most. Similarly the good returns work in opposite directions (good returns towards the end in accumulation and good returns at the beginning in the decumulation). My take is sequence of return is important in both the cases and catch is during bad phases, invest more (in accumulation) and withdraw less (in decumulation).

Thank you Prabhakar!!!

Completely agree sequence of returns affects both phases.

Bad returns during last few years before retirement can be problematic too.

Just that when you get a bad sequence during accumulation phase, you have a few options.

You can divert more towards savings although this may not be as useful if the hit is just before retirement. Your existing corpus is much bigger.

In some cases, you can even seek work extension or go to part-time job right away.

You can see there is much higher flexibility. You will also be better prepared mentally.

The other very important aspect is that you are still not withdrawing from your corpus before retirement.

Therefore, reverse cost averaging does not wreak havoc on your portfolio.

Once retired, these options may go away.

Suggest you go through the following post.

https://www.personalfinanceplan.in/opinion/four-phases-of-retirement-planning-earn-save-grow-and-preserve/

In my view post retirement one should should invest in debt oriented mutual funds growth option to minimise the volatility associated with equity investments.

Hi Arvind,

Your point has some merit.

If one has lots of money which can take care of inflation for a prolonged period, the person can choose to play safe and invest in low volatility assets.

For others, they need to take some risk and counter inflation and get growth in their portfolio.

AGREE, why to invest in volatile asset after retirement. Accumulation phase is fine.

Thanks Shivaji!!! Some allocation to equity (growth assets) may be needed after retirement too.

Dear Deepesh,

Nicely explained with hypothetical example. Thanks a lot again.

In real life it would be completely different than what would we see in the book. I can understand there are soon or later many people will be touching decumulation phase and you have wrote a nice article to show how sequence of risk.

A constant thought strikes me again and again that – then how can a constant returns instruments say debt schemes with range (8-1o%) can of successful retirement without hurdles ? Considering the inflation rate (6-8%) real return would be in range 2-4 % in addition to the LTCG tax it would further reduce the effective return. If the withdrawal beyond 4 % would also dangerous too.

I heard about various strategy of withdrawal during decumulation phase. like bucket Starkey,dynamic withdrawal strategy, interest withdrawal strategy, capital preservation strategy and many more.

I am confident and appreciate further that you would write in future on those strategies.

Dear Dilip,

I couldn’t agree more with your point.

Settling for very stable (too stable) returns in the form of debt investments for 30-40 years of retirement can be a problem (unless the investor has a lot of money).

You need equity exposure.

However, at the same time, the investor needs to appreciate the risk involved. With debt, it is a constant struggle to beat inflation. With equity, volatility can translate to risk if withdrawal results in permanent losses (I had referred the link to this post in this context).

If the investor is aware of the risk and makes such choices, it is fine.

My concern is investors do not always appreciate the risk involved. Moreover, in good times, the perception of risk goes down (people start to feel the good times will never end and they feel they can’t lose money with equities). That’s the main problem.

Essentially most retirement withdrawal techniques essentially boil down to asset allocation approach. But yes, different techniques can bring out different behavioural responses from the investors. And such behaviour is extremely important.

Sure, I will consider writing on such topics.

First, the corpus need to be more than that is required to meet the monthly expenditure to take care of inflation & voltality or in other words plan monthly expenditure accordingly. Having done that I suggest one spend about 75% of his annual earning fron the corpus and invest 25% in equity or balance funds, We need to remember that even expenditure may not be stable due to family needs in addition to need arising out of inflation. This would also enable us leave some thing for the successor which predominantely arises due to uncertainty of life. The percentage suggested can change depending upon need. It may some time be higher where as other years could be lower.

Dear Sir,

You have not given the example with the reality of life i.e. INFLATION

It will be appreciated if you give example including inflation.Suppose you require 600000 in the first year then average inflation of 7.5 to 10% has to be considered.

Please give example from 60 to 90 with inflation so that you can maintain same level of standard in Old Age.

0% inflation is impossible. Please give with 8%,9% and 10% inflation, which is the reality.