Franklin Templeton AMC dropped a bomb yesterday. In a communication dated April 23, 2020, it notified that it is winding up 6 debt mutual fund schemes.

- Franklin Low Duration Fund

- Franklin Dynamic Accrual Fund

- Franklin Credit Risk Fund

- Franklin Short Term Income

- Franklin Ultra Short Bond

- Franklin Income Opportunities Fund

These are very popular schemes. The combined assets under these schemes are ~ 28,000 crores.

I copy an excerpt from Franklin Communication.

What does this mean?

- You can’t make any further purchases in the mentioned schemes.

- You can’t redeem your investments from the mentioned schemes. Your money is stuck.

It is like the entire portfolio of these schemes has been side-pocketed.

The realized value from the sale of underlying assets (or receipt from any interest/ principal from the bonds) will be distributed to the unit holders on proportionate basis.

Do note the NAV of these schemes will still be published on a daily basis.

Additionally, there are other mutual funds (both equity and debt) from Franklin that are open for business as usual. The issue is limited to only 6 debt mutual fund schemes.

Is my money lost?

No, your money is not lost (even though you may get back less).

It is just stuck. You have lost the flexibility of taking it out whenever you want.

As and when the fund realizes any money from these investments, it will be transferred to your bank account.

What must have forced Franklin AMC’s hand?

To meet redemptions, they must sell bonds. And the bond markets are not very liquid, especially for the not-so-good-credit-quality bonds.

You do not get good deals (and sometimes no deal at all) when you try to sell in illiquid markets. We witnessed how NAV of most debt mutual fund schemes (even liquid funds) fell during the month of March. This was because they faced sharp redemption pressures.

Franklin schemes have been witnessing sharp outflows too. For instance, Franklin Ultra Short used to be a ~ Rs 20,000 crore scheme just about a few months back. The scheme’s size as on April 23, 2020 is just Rs 9,728 crores. As I discussed in one of my earlier posts, a sharp drop in the size of the mutual fund scheme is a red flag.

Here is how the asset under management have fallen for Franklin UST Bond Fund.

Franklin knows the best about the quality of the portfolio of these schemes. Perhaps, Franklin figured out that it won’t be able to meet redemptions if outflows continued at this scale. That the credit quality of its portfolio was not particularly good didn’t help.

The lockdown and its repercussions will test viability of many weaker companies. Hence, it is difficult to find buyers for bonds from such weak companies.

In a way, it is also a prudent move. If the redemptions continued, Franklin would have continued to sell better quality bonds from its portfolios. Therefore, the investors who stayed back would be left with even lower quality portfolios.

When will I get my money back?

You will get your money back as and when the AMC realizes any income (interest payment or principal repayment) and sells these bonds. Sale of bonds is difficult during present times.

If you are an investor, look at the underlying portfolio to see when various exposures are maturing.

Franklin Ultra Short Bond fund is an ultra-short bond fund. For an ultra-short bond fund, the average maturity of the portfolio can be upto 6 months as per SEBI guidelines.

Franklin Low Duration Fund is a low duration fund. For a low duration fund, the average maturity (Macaulay duration) of the portfolio can be up to 1 year.

Therefore, you can expect an Ultra-short bond fund portfolio to mature faster. Hence, you are likely to get your money back sooner in case of an ultra-short bond fund (provided there are no defaults).

At the same time, average maturity of 6 months does not mean that all the underlying bonds will mature within 6 months. Remember, the cap is on Average maturity(Macaulay Duration of the portfolio, and not on the maturity of each bond).

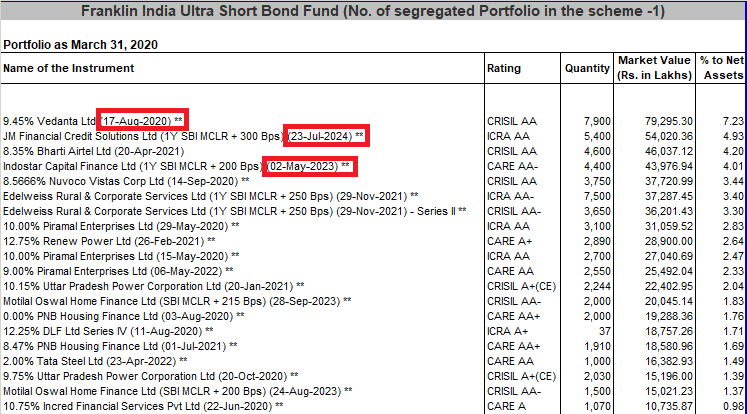

I copy a snapshot of some the portfolio holdings of Franklin Ultra Short Bond Fund as on March 31, 2020. You can see some of the bonds whose maturity extends to even 2024.

Do note this data is on March 31, 2020. On March 31, the size of Franklin Ultra Short Bond Fund was Rs 10,964 crores (On April 22, it is Rs 9,738 crores). So, it has lost Rs 1,200 crores over the last 3 weeks. The AMC would have sold investments to meet redemptions. Hence, the current portfolio may be very different from the one copied above.

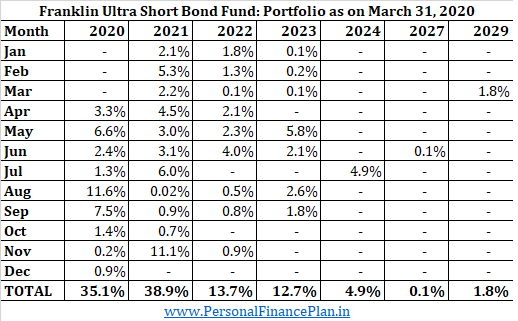

As for the portfolio as on March 31, 2020, here is how the maturity profile of the Franklin Ultra Short Bond Fund looks like.

The sum of all the percentages is more than 100%. This is because the scheme had borrowings as on March 31, 2020.

As mentioned earlier, the portfolio may have changed since March 31, 2020. You can see only 74% of the portfolio is maturing in the next two years. This is quite bizarre for an ultra short duration fund. Do note that this data is only about bond maturity (principal repayment). All the bonds will continue to pay interest too as per the schedule. Hence, you will more than what you see in the table (unless there are defaults).

How good is the portfolio?

While credit ratings are not really reliable, it still gives us an idea of the quality of the overall portfolio. In this case, this might indicate how much money you will get back.

I have put the portfolio in the descending order of credit quality. The only exception is A1 and A1+, which should be right up at the top (but I have put them lower). You can check the credit scale of various rating agencies here: CRISIL, ICRA CARE

Over 80% of the portfolio is AA- and above. So, I think you should get a fair amount back.

You can check the portfolio of other Franklin funds here (Select Monthly Portfolio Disclosure) and do similar analysis.

More worried about the “Beyond First order” effects

What we discussed above is how this Franklin move affects investors. However, I feel the repercussions of this move will be far-reaching.

What will be impact on other debt MF schemes from Franklin?

What about the confidence in other credit risk funds? Will this category survive?

The Credit Risk Mutual funds are a source of funding to many weaker companies. If their debt is having so many problems, what about their equity?

What about the confidence in debt mutual funds in general?

I don’t know the answer. Time will tell.

Choose your investments wisely

Disclosure: I do not have exposure in any of these schemes. However, as discussed in my earlier post on Franklin exposure to Vodafone-Idea bonds, I did recommend a few clients to take some exposure in Franklin Ultra Short Bond Fund as a credit risk fund. In hindsight, it looks like a bad decision. After Vodafone-Idea issue and especially after the recent lockdown, I had started asking investors to exit this fund. However, I could not communicate this to all and some of them will be stuck with small exposures. There are certain legacy portfolios (clients purchased before they started working with me) that still have significant exposure to Franklin Ultra Short Bond Fund. That is painful. Could have done better.