Do you believe in working with an asset allocation approach in your portfolio?

Do you rebalance your portfolio at regular intervals?

Is there a merit in dividing our portfolio in assets with low correlation?

In this post, let us construct a multi-asset portfolio combining domestic equity, international equity, and gold and see if delivers superior performance compared to a Buy-and-hold Nifty 50 portfolio. Superior performance could mean better returns, or lower volatility, or simply better risk-adjusted returns. We compare the performance of this multi-asset portfolio over the last 9 years.

You may argue that international equity is not really a different asset and is still equity. Fair enough but let us play along. I could have added a Fixed income asset (say a liquid fund) and diversify the portfolio even further. However, I have not included a fixed income asset in the portfolio.

Over the past few months, we have tested various investment strategies or ideas and compared the performance against the Buy-and-Hold Nifty 50 portfolio. In some of the previous posts, we have:

- Compared the performance of Nifty Next 50 against Nifty 50 over the last two decades.

- Compared for the performance of Nifty 50 Equal-Weight vs Nifty 50 vs Nifty 50 over the last 20 years.

- Considered the data for the past 20 years to see if the Price-Earnings (PE) multiple tells us anything about the prospective returns. It does or at least has in the past.

- Tested a momentum strategy to shift between Nifty 50 and a liquid fund and compared the performance against a simple 50:50 annual rebalanced portfolio of Nifty index fund and liquid fund.

- Used a Simple Moving Average Based Market Entry and Exit Strategy and compared the performance against Buy-and-Hold Nifty 50 over the last two decades.

- Compared the performance of 2 popular balanced funds against a simple combination of an index fund and a liquid fund.

The Funds and the Asset Allocation

I have used the following three instruments for this analysis.

- Nifty 50 TRI (for domestic equity)

- Motilal Oswal Nasdaq 100 ETF (as proxy for international equity fund)

- Nippon Gold Savings (for gold)

We use the data for the above 3 from April 1, 2011 until July 22, 2020. Before that, there were no passive investment options for the international equity fund.

With respect to asset allocation, we have many options. We can divide the money equally between the 3 funds. Or since you are based in India, you can give a higher allocation to Nifty 50. I would prefer a higher allocation to domestic equity (Nifty 50) because that’s what we compare our portfolio performance against consciously or sub-consciously.

I use the following allocation:

- 50% to Nifty 50 TRI

- 25% to Motilal Nasdaq 100 ETF

- 25% to Nippon Gold Savings Fund

The portfolio is rebalanced annually on April 1.

The Results

Let us begin with point-2-point returns.

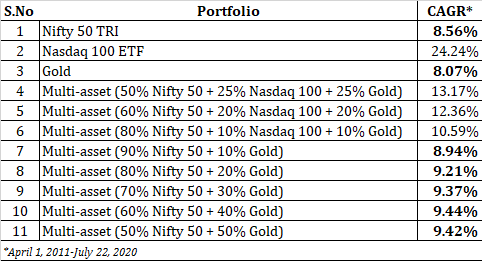

Motilal Nasdaq 100 ETF is outright winner with CAGR of 24.24% p.a. over the 9 odd years. The multi-asset portfolio (mix of Nifty, Nasdaq 100 ETF and Gold Savings Fund) is second with CAGR of 13.17% p.a. Nifty 100 TRI and the Gold Fund return 8.56% p.a. and 8.07% p.a. respectively.

Here is the performance in each calendar year.

While Nifty 50 TRI has given negative returns in 3 calendar years, the multi-asset portfolio has not given negative returns for any calendar year under consideration. This alone is a huge positive. The multi-asset portfolio has beaten the Nifty 50 TRI in 7 out of 10 years.

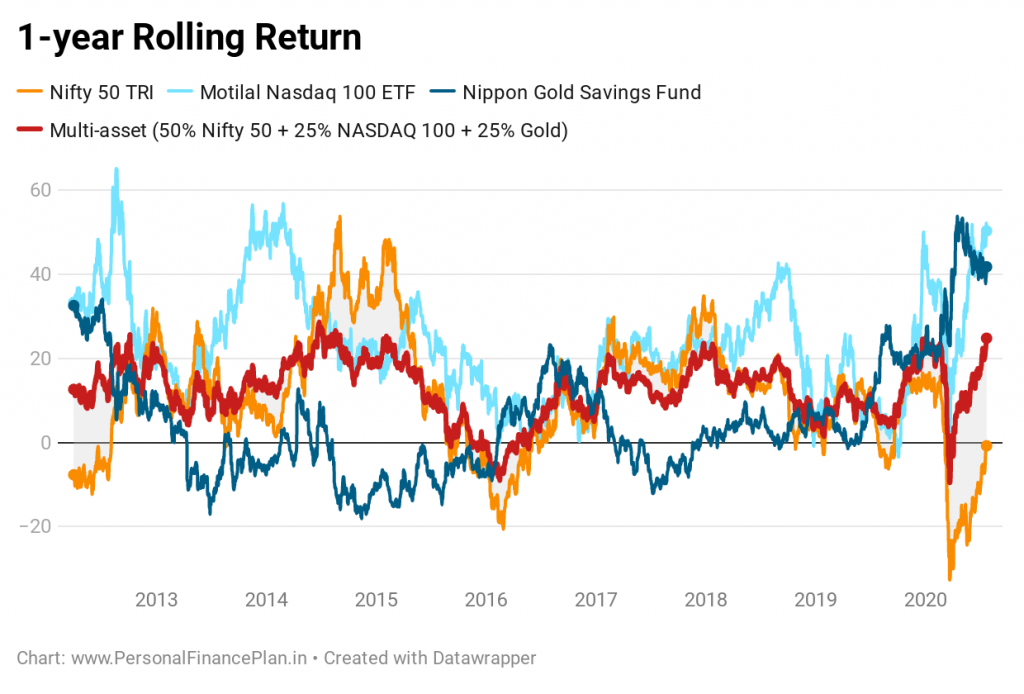

How about rolling returns?

You can see that the performance of the multi-asset portfolio is much more consistent. You would expect that too when you add assets with a low correlation to the portfolio.

Downside protection is a major source of excess returns. Let us see how the multi-asset portfolio has performed in managing drawdowns.

The multi-asset portfolio does very well.

What about the rolling risk?

The multi-asset portfolio has been a super performer in this aspect.

So, the multi-asset portfolio (for the period under consideration) gives much better returns than the Nifty 50 TRI with lower volatility and much lower drawdowns.

What else can you ask for?

The benefits of diversification, asset allocation, and regular portfolio rebalancing in full glory.

The Usual Caveats

- Past performance may not repeat.

- Rebalancing on a regular basis will involve transaction costs and can result in tax liability. I have not accounted for the impact of taxes.

- The tenure is noticeably short, just over 9 years. Not smart to arrive at far-reaching conclusions.

- I am saying all this in hindsight. Nasdaq 100 has been a superb performer over this last decade. Add to this the rupee depreciation from ~40/USD to ~75/USD in this decade. Nasdaq simply shines through. In fact, for the period under discussion, the ETF NAV has gone by over 754%. On the other hand, Reliance Gold Fund NAV and Nifty 50 TRI have gone up by just over 200%. So, exposure to Nasdaq 100 in any portfolio will add value.

- I chose Nasdaq 100 ETF because that was the only option available since March 2011. No other passive fund option before that.

- Motilal Nasdaq 100 ETF is an ETF. I have taken the day-end NAV for this exercise. In real life, you will have to purchase ETF on the stock exchange. Hence, your acquisition price can be quite different from the day-end NAV. In fact, the purchase price can be different from real-time NAV. That’s how ETFs work. Motilal Oswal Nasdaq 100 FoF (that invests in the ETF) was launched only in the year 2018.

- Why Nasdaq 100 fund and not S&P 500 fund? I have no explanation. S&P 500 looks better diversified on paper. Nasdaq 100 consists of primarily tech companies in the US. In 2011, given a choice, I might have picked up an S&P 500 index fund.

- Why not a Global Equity Index Fund? If you are looking for diversification, a global equity index might be a better choice than a US-only index? Again, the lack of options.

- I have used Nippon India Gold Savings Fund. We could have used physical gold. Could have used Sovereign Gold Bonds (SGBs) after 2016. SGBs have an additional advantage of interest income of 2.5% p.a. (or 2.75% p.a. earlier). However, rebalancing portfolios using Sovereign Gold Bonds will be quite difficult.

Eliminating Nasdaq from the choice

We know that the Nasdaq 100 ETF has been a primary driver of returns in the multi-asset portfolio discussed above. What if we had combined just gold and Nifty 50?

Let us discard Nasdaq 100 from the choice of investment options. Let us see how various mixes of Gold Fund and Nifty TRI would have performed.

As you can see, even without Nasdaq 100, gold has added value to the pure equity portfolio. You can see, a mix of an annually rebalanced portfolio of gold and Nifty has given better returns than both 100% gold and 100% Nifty. This means the combination portfolio has given better returns than the two underlying assets it is composed of. I have not checked the volatility of the combination portfolio, but I expect it to lower than a pure equity portfolio.

That’s the power of portfolio rebalancing. Do note rebalancing may not always give higher returns than individual assets but is quite likely to reduce portfolio volatility.

What should you do?

While there is no guarantee that the past will repeat, there is merit in adding different assets to your portfolio. While the percentage allocation to various assets will change depending on your comfort and risk appetite, adding low correlation assets to your portfolio will likely add value over the long term, either in terms of higher returns or lower volatility or both.

I have not added a fixed income (debt) product to this portfolio. Adding fixed income products will make this portfolio even more robust.

What do you think?

12 thoughts on “Adding Gold and International Equity to the Portfolio: Does it enhance Portfolio Performance?”

Dear Deepesh,

Excellent analysis !!

What is the best way to invest in International markets considering diversification, taxation and volatility, (index funds/ETFs/FoF). i’m interested in investing 15-20% in international markets.

Regards,

Thanks Vandan!!!

I prefer India domiciled funds. Therefore, I like FoF, index funds and ETFs domiciled in India better than investing directly in markets abroad (Vested, Stockal, Interactive brokers). Too messy for me. I am sure others can manage.

Now, there is TCS on LRS remittances over Rs 7 lacs in a financial year, making investing abroad directly even more cumbersome.

Between ETFs and FoFs (currently domiciled in India), I prefer FoF because it is easier to buy and sell. Easy to run SIP.

With ETFs in India, there are liquidity issues. There can be a sharp variation between NAV and price. Plus, the equity market that the ETF tracks may be closed when India trades. Then, you have to look at futures market and get a sense of real-time NAV and place your bids accordingly. Not easy.

Hi,

Thanx for the reply.

Can you suggest some good Indian domiciled fund having some (around 10-20%) exposure to diversified international markets like:

1. PPLTE

2. Axis Growth Opportunities Fund

3. Any other good fund

Hi Vandan,

I don’t prefer blend products like PPLTE (unless you want to optimise on taxes).

I prefer pure play funds. There are many funds domiciled in India that invest in markets abroad. you can find this info on ValueResearch.

Pick up any low-cost fund.

Very good analysis, For normal retail investor, Simple Nifty index fund + Liquid fund with AA 50:50 is more than sufficient, If we add International funds, Gold, then rebalancing and paying taxes are cumbersome,

I have gone through your past studies on like to know, how far this simple portfolio (Nifty + Liquid fund) beats or low volatile when compare to your other models.

Second query, if i have list of goals like retirement,Son Education, Daughter education, Marriage , How to manage portfolio, Should we have Unified portfolio for all the goals, or Should i create separate portfolio for each goals. Kindly share post on this topic.

Hi Kalai,

A regular rebalanced portfolio 50:50 of Nifty and a liquid/debt fund is quite formidable.

However, international equity and gold are likely to add value to that portfolio.

Taxes are as big a problem. Gold and international fund get the same treatment as a liquid fund.

I have not tested Nifty+Liquid against all possible portfolios but it has done well mostly. Not easy to beat.

There is no right or wrong approach. Having separate funds or folios for each goal is easier to identify and account mentally. But leads to too many funds or folios. I prefer a unified portfolio but keep checking the growth for various goals.

I work with a set of funds for all the long term goals.

Request you to come up with post how to manage Unified portfolio for all long term goals, It will be very much useful for retail investors.

Do you maintain single AA for all the goals in unified portfolio.

Very informative certainly.

Just a query, what if you value the Nasdaq ETF at constant currency? Logic being to weed out currency risk. Forward looking decisions then would not get weighed by the fact that INR depreciated to 75 from 40.

Thanks!

I get your point. Returns from Nasdaq have been sharply augmented due to rupee depreciation wrt USD. Tech stocks have been a runaway winner in this decade. Hence, we need to take this analysis with a pinch of salt.

It is possible to do these calculations at constant currency too. Will need to enter values for USD/INR rates.

However, that won’t be very practical because you earn in INR and investments must be made in a different currency. Currency conversion has to happen.

Rebalancing will also bring in currency conversion.

Investing in asset priced in different currencies also brings in a level of diversification. So, investing in USD assets reduces currency risk at the portfolio level (although it seems like a big currency risk at the asset level).

“Investing in asset priced in different currencies also brings in a level of diversification.” — Absolutely agreed.

But I get your point overall.

My only point was: If going forward (next 18-20 years) USD/INR doesn’t become 140/150 levels, then investing in NASDAQ or USD assets will not give the same kind of kick to my portfolio as the back test. So I wouldn’t want to take an exposure to unhedged USD assets unless someone advises me on the macro conditions over the next 2 decades. 🙂

By the way, went through quite a lot of your posts. I am impressed and considering reaching out for portfolio advise.

No one knows what will happen over the next two decades. People can make very fancy and cogent forecasts. However, that info is not really actionable.

At the same time, when we invest in let’s say Nasdaq or S&P 500 or a global equity index, we are also taking a call on US equity markets.

Exposure to an economy that is not India.

Hence, investing in global equities is not just a currency play.

Different economy. Different currency. Diversification.

Hedging will be expensive. I would rather leave my position unhedged.

But yes, I get your point. In this decade, both aspects (returns from Nasdaq stocks and the currency movement) were very favourable to Indian investors. This may not repeat.

Thanks. Glad you liked the content.

Hi Deepesh

What is your view on including NIPPON INDIA ETF LONG TERM GILT in this asset allocation model ?