Quality healthcare is getting expensive with each passing day. And it is important to buy adequate health coverage to have some cushion against the rising health care costs.

However, buying health insurance is not easy.

Why? Because the insured event is not very objective.

Contrast this with life insurance. There is just one insured event. The demise of the policyholder. And it is an objective one too. If the policyholder has passed away, the insurance company must pay. There is no confusion about whether the policyholder is dead or alive. And all the plans cover the same insured event. You can just go with the cheapest life insurance plan (do look at the claim settlements too).

In health insurance, there are tons of insured events. There is always an element of subjectivity involved. You can’t be sure whether a particular treatment is covered unless you check with the insurer.

There are multiple variants. Individual, family floater, top-up and Super top-up plans. Moreover, different policies offer different coverage. For instance, Policy 1 covers procedure X and not Y. Policy 2 covers procedure Y and not X. There are waiting periods, sub-limits, co-payment clauses, disease-wise capping, no-claim bonus, restore benefits and many more. And plans will vary on these parameters too. Not just that, each company has 5 different plans. Different coverage and premiums.

This makes choosing a health insurance plan difficult. You can’t just go by the lowest premium. You must understand the coverage and features of the plan to understand whether this is right fit for you.

In this post, we look at a critical parameter that you must consider before buying a health insurance plan. Room-rent sublimit. If you get this wrong, your insurer will not reimburse/cover the full cost of treatment even if the treatment is covered under the plan.

What are Sub-limits?

As the name suggests, within the overall Sum Insured, the insurance company covers a particular expense only up to a certain limit. For instance, even though the Sum Insured is Rs 5 lacs, the policy may cover treatment for a certain illness only to the extent of Rs 50,000. If you incur Rs 65,000 on hospitalization for such illness or procedure, you will have to pay Rs 15,000 from your own pocket.

Sub-limits can be structured in any way. There is no specific IRDA guideline on the matter. You must read the terms and conditions of the health cover plan to understand if there are any sub-limits in the plan. With these sub-limits, the insurer can limit its liability to a certain extent.

Therefore, health insurance plans with sub-limits are likely to be cheaper than those without any sub-limits.

One of the most important sub-limits in a health insurance plan is the cap on room rent. With this cap, the insurance company caps its liability on room rent per day.

Peculiar nature of hospital charges

Hospital charges are linked to the type of room you have taken. Doctor’s visit to a shared room will cost you Rs 1,000. However, if you have taken a private room, visit by the same doctor will be charged at say Rs 2,000 per visit. It makes no sense but that’s the way it is.

A simple X-ray that costs Rs 500 for a shared room may cost Rs 1,000 if you have taken private room. You have to go to the same X-ray room and stand before the same machine but the charges are different.

In other words, the hospitals charge you on the basis of your ability to pay.

And what better indicator of your payment ability than the room you have chosen to stay in!

From your perspective, your coverage will deplete fast if you are staying in an expensive room. And you can’t ignore that if your treatment is prolonged.

How does this affect your insurance claim?

Since the charges are linked to the type of room or the room rent, your medical bill for the same treatment goes higher if you choose better accommodation.

If your health coverage is without sub-limits, there is not much insurer can do. It will have to pay for all the covered expenses.

However, if your insurance plan has sub-limits, be prepared for a surprise. In this case, if the room rent per day exceeds the prescribed sub-limits (cap), the insurance will pay charges only in the proportion of rent sub-limit to actual rent.

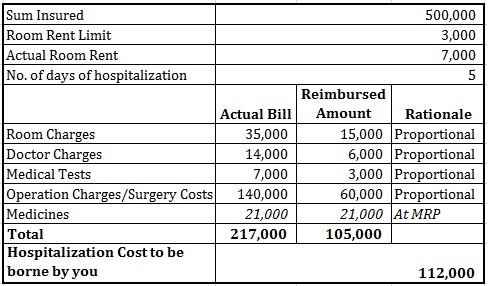

Suppose room rent cap (or sub-limit) in your health plan is Rs 3,000 per day and the actual room rent is Rs 7,000. You get hospitalized for 4 days and run up a bill of Rs 1 lac. You might feel that insurance company will pay everything apart from excess room rent i.e. Rs 1 lacs – 4, 000 * 4 days = Rs 84,000. Well, that’s not the case.

The reimbursed amount will only be Rs 1 lacs * 3000/7000 = Rs 42,857. Even though you had total cover of Rs 5 lacs, it does not matter since the reimbursed amount will be in proportion of sub-limit and actual room rent. This will certainly come as a shock to someone who is not aware.

Typically, this is done for hospital services. Medicines are reimbursed at MRP irrespective of the room rent.

Illustration

Please note that the cost for medicines to be reimbursed is same as the actual cost. You have to pay Rs 1.12 lacs from your own pocket.

Please note that the cost for medicines to be reimbursed is the same as the actual cost. You have to pay Rs 1.12 lacs from your own pocket.

What should you do?

Avoid purchasing health insurance plans with room-rent sublimit, especially if you are living in bigger cities.

Health insurance plans from public insurers (National, Oriental, United) tend to have room-rent sublimit. Usually daily room rent is capped at 1% of the Sum Insured. For ICU, it is 2% of the Sum Assured.

If you already have a plan with room rent sub-limit, you can port to a new plan without sub-limits while retaining continuity benefits (waiting period).

However, not everyone can afford a health insurance plan without sub-limits. In that case, you can purchase a plan with sub-limits. Before finalizing the plan, try to get an idea of room rents in the hospitals in the vicinity or those hospitals where you would like to get treated. Subsequently, pick up a plan where room rent cap is enough for taking a room of choice at those hospitals.

Sometimes, your hand may even be forced. Even though you want to go for a shared or a cheaper room, it may not be available. In that case, you will have to pick a private room or take treatment in another hospital. In case of emergency, that is not an option. You take whatever is available.

So, if you can afford, pick up a plan without sub-limits. If you can’t, be aware and be prepared.

Other posts on Health Insurance Plans

Tax Benefits for Purchasing a Health Insurance Plan

Use this smart Health Insurance Strategy to get higher cover at a lower premium

How claim is settled if you have two Health Insurance Policies?

Individual Health Insurance Plan Vs. Family Floater

What are Top-up and Super Top-up Health Insurance Plans?

How Health Insurance Companies can easily trick customers?

Health insurance plans you must avoid

Top 10 Exclusions under your Health Insurance Plans

Should you purchase Critical Illness Plans?

Should you purchase a Health Insurance Plan with Maternity Benefits?

Should you purchase a Health Insurance Plan with Restore/Refill Benefit?

What is a Hospital Cash Insurance Plan?

Featured Image Credit: Unsplash

The post was first published in November 2015 and has been updated since.

23 thoughts on “How Room Rent Sub-limit can affect your Health Insurance claim?”

Once again very good information – and unbiased.

Can you please share how the following situation plays out? Maybe even write a post if you think it makes sense.

What would be the situation if I have 2 policies – both with room rent limit and I want to claim in scenario as described below:

Policy1: insurance amount Rs 5 lac, room rent limit 5000, Company A

Policy2: insurance amount rs 4 lac, room rent limit 4000, Company A

If hospitalisation needs to be done where room rent is rs 10,000 per day and total cost is Rs 2 lacs (say 5 days hopitilization). Both policies are from same insurance company. Assume any amount for medicines, etc.

This may not be as uncommon scenario as some might think, as health insurance purchase by older people and paid premium over decades may lead to such scenarios since portability was not in place / not known.

thanks in advance,

Thanks Toohey!!!

As mentioned in the post, prices of services in hospitals are linked to room rent (or type of room). Assuming Rs 2 lacs is the bill for such services, you should be reimbursed Rs 1.8 lacs (Rs 1 lac under policy A and Rs 80K under Policy B). There will be some difference for sure. But the amount to be reimbursed should be in that range. I am further assuming there are no other sub-limits apart from cap on room rent. Exact amount will depend on individual policy coverage.

Please note items sold on MRP such as medicines are reimbursed (room rent limit won’t impact claim reimbursement on this part of the bill).

I agree such scenarios should not be uncommon since portability norms came into existence only a few years back.

Sir, would it make any difference if the both policies of 4lac and 5 lac be from different insurers?

Prabhanshu,

Didn’t get your question. Difference to what?

What are the portability options? Do we get the benefit of waiting period already spent with the existing insurer? Are there clear rules about this?

Yes you do. There is another post on my website on health insurance portability.

Do go through the post.

http://www.personalfinanceplan.in/insurance/health-insurance-portability-migrating-to-a-new-health-plan/

Sir

You have provided very good information.But problem with policy without sub limit is that there will always a possibility of misuse.There will be a possibility of jacking up of Premium by the company for the extravagance of few customers.I have personally observed that in last two years in Optima Restore of Apollo, premium has been increased to the order of 50%. In my opinion, a policy which offers a single private room accommodation is reasonable in the long run, even if with some inconvenience.

with regards,

Satheesh Rao

Dear Satheesh,

I agree with your points. Plans without sub-limits will be more expensive with sub-limits.

Quite possible the insurance company may have revised its premium based on claim experience.

But atleast the customer won’t be in for any surprises at the time of claim.

It is your choice. The idea is that the customers should be aware of what they are getting into.

If you are aware, you can even use a plan with rent sub-limit smartly and reduce your hospital bill liability.

Hi Deepesh,

Yes I do understand that If person is going for higher category room, Insurance company will deduct proportional amount from other charges like doctor fees, lab charges etc….

BUT, is this same deduction rules will be applicable for PRE Hospitalization doctor and lab charges if claimed with main hospitalization file? Doctor visits and Lab charges occurred during pre hospitalization.

Hi Prashant,

Nice observation. I have not come across raising such issue. Therefore, will rely on my judgement.

From what I have seen, policy documents do not put any restrictions on such charges (like they do in case of room rent charges).

Therefore, that should not be a problem. Moreover, differential charges come into picture only when you are admitted in the hospital.

As I understand, actual room rent should not affect pre-hospitalization charges.

Hi Deepesh .. MF Direct Plans vs MF plans through distributors … which one is better

Not the right post for this comment.

Direct plan of a MF scheme will give better returns than regular plan of the same scheme.

Hi Deepesh,

Post on site are very informative. Great job.

Me and my wife both are covered under insurance policy based on medical reimbursement process (not on cashless facility) from my employer worth up to Rs 1.5 lakh. Now i am planning for one medical insurance plan from star health worth Rs 5 lakhs (Total cashless). I want to ask that if in future my total medical expense exceeds Rs 7 lakhs for one particular disease then how much amount will be recover from both the policies. Like as per figures, will it be possible to recover Rs 6.5 lakhs ? I mean can i recover the remaining amount from second insurer?

* Employer Insurance – Medical reimbursement

* Star Health Insurance – Cashless Facility

Please suggest

Thanks

Hi Sushant,

You are welcome. Please share the post with your friends.

I have a few posts on my website on claims from multiple policies.

https://www.personalfinanceplan.in/insurance/how-claim-is-settled-in-case-of-multiple-health-insurance-plans/

Technically yes. You can claim up to Rs 6.5 lacs.

Claim from the second policy will not be cashless.

Hi deepesh

Really a worth…post you had ….sir please go on my confusion…I am going for single private room… With no limts…what does it mean…is it mean we have to take single common AC room or we can opt for deluxe category room or higher room in this private single room category….please explore…also I am going to port my star health policy for my family to Cigna TT …is it worth..

What would be the claim ratio for the Cigna TT..and what services they provide to their customers…please comment

Hi Gaurav,

Thanks. Do share the post with your friends too.

Yes, single AC room should do. Please note every hospital will have different room categories.

You have to go with the cheapest single private room that has AC.

Luxury or premium rooms won’t be covered. Always better to check with the insurance company before a planned hospitalization.

If your policy is old and you have not faced any issues, it is better to continue with the existing plan.

SASI SANKAR SAYS

OCTOBER 6TH 2017

HI DEEPESH

There are limits for pre and post hospitalisation expenses. Also there are limits to the claims of senior citizens.

please reply

Dear Sir,

Not sure if I got your question right.Could you be a bit more specific?

Till date, I have not seen sub-limits depending on age. There may be co-payments but no sublimits.

Hi Deepesh,

I have some urgent queries related to this topic. Can you please drop me sms/watsapp from your number, so that I can call and clear my doubts. Thanks in Advance.

Hi Madhav,

Please leave your query as a comment. I will respond at the earliest.

Alternatively, you can write to support[at]personalfinanceplan.in.

Dear Deepesh, I want a clarification in New India Assurance’s policy wording for No Proportionate Deduction and no one seems to be knowing what does it actually mean. It will be great if you can help me with it.

3.2 PROPORTIONATE DEDUCTION CLAUSE:-

Reimbursement/payment of Room Rent, boarding and nursing expenses incurred at the Hospital shall not exceed 1% of the Sum Insured per day. In case of admission to Intensive Care Unit or Intensive Cardiac Care Unit, reimbursement or payment of such expenses shall not exceed 2% of the Sum Insured per day. In case of admission to a room/ICU/ICCU at rates exceeding the aforesaid limits, the reimbursement/payment of all other expenses incurred at the Hospital, with the exception of cost of medicines, shall be effected in the same proportion as the admissible rate per day bears to the actual rate per day of Room Rent/ICU/ICCU charges.

OPTIONAL COVER I: NO PROPORTIONATE DEDUCTION

On payment of additional Premium as mentioned in Schedule, it is hereby agreed and declared that Clause 3.2 stands deleted for the members covered in the Policy as stated in the Schedule.

You shall continue to bear the differential between actual and eligible Room Rent. – What does this mean ?

Despite opting for No Proportionate by paying extra premium i am not really convinced of this line above. Please help me decipher it. Many Thanks. R

Dear Madhur,

I will put down my understanding.

If you do not opt for this feature:

1. You pay the difference between room rents.

2. Additionally, the insurers merely foots the proportionate charges for other expenses. For instance, the limit us Rs 3k per day. You got admitted in an Rs 7K per day room. The surgery costs Rs 70K. The insurer bears Rs 30K. You pay the remaining.

If you opt for this feature by paying an additional premium:

1. You still pay the difference between room rents.

2. For the example given above, the insurer foots the entire 70K.

I would like to know if top up plan will come into picture if sub limit of particular disease is exhausted.

For example, My insurance coverage is 500000 and have a top up plan of 500000.

Insurance specifies cataract limit is 25000 and the cost I incurred is 50000. Can I use top up plan to claim remaining 25000?