You recently sold a house for hefty profit of Rs 80 lacs. You had bought the property ten years back for Rs 20 lacs and sold it for Rs 1 crore. Even after adjusting for indexation and other transaction costs, the long term capital gains comes out to Rs 50 lacs. To find out the method for calculation of long term capital gains, read this post here.

Long term capital gains on a residential property are taxed at 20% after adjusting the cost of acquisition for indexation. 20% of Rs 50 lacs is Rs 10 lacs. You feel like the Government is robbing you. It is not letting you reap the full rewards of perhaps the wisest investment decision you made in your life. Well, that’s the way it is. The Government keeps a pie of what you earn (salary). Similarly, it keeps a share of your gains.

However, the Government does give an option to avoid paying tax on these long term capital gains (LTCG) arising out of sale of this house.

You can seek relief in two ways. Under Section 54 and Section 54EC. Under Section 54, you need to re-invest in residential property within the specified time limit. Under Section 54EC, you need to invest in select bonds for three years. We will discuss both options in detail.

How to save tax on gains from sale of house under Section 54?

There is some relief available to you under Section 54 of the Income Tax Act.

You can avoid paying income tax on long term capital gains tax on sale of a residential house if

- You purchase a residential house within a period of 1 year before or 2 years after the sale of such house; or

- You construct a residential house within a period of three years from the date of sale of such house

Please note the relief under Section 54 is available for only long term capital gains. There is no such relief under Section 54 for short term capital gains. So, if you sold your property within 3 years from the date of purchase at a gain, be prepared to pay short term gains tax.

NRIs (non-resident Indians) can also avail this benefit under Section 54.

Why does the Government offer this benefit?

Well, there may be many reasons for selling an old house and buying/constructing a new house. You may want to shift to bigger (or smaller) house. Or you may be shifting cities and may have to sell the old house to purchase a house in the new city. In such cases, your intent may not be to earn income by way of sale of old house but to acquire a new house.

The Government does not want to penalize you in such cases. Hence, it offers conditional relief under Section 54 in such cases where you use the gains from sale of old house to purchase/construct another house.

Are there any conditions to be met?

Yes, there are a few additional conditions to meet.

- Long Term Capital Gain on only sale of residential property is covered under Section 54. You cannot seek relief for LTCG on sale of gold or debt mutual funds or even commercial real estate under Section 54.

- You can use the capital gains to purchase (or construct) just one residential property. you cannot utilize the LTCG to purchase/construct two different houses. In the aforementioned example where you had LTCG of Rs 50 lacs, you must invest Rs 50 lacs in a single house worth Rs 50 lacs or more to get the maximum benefit. If you purchase two properties worth Rs 40 lacs each, you can get the relief for only up to Rs 40 lacs. In such a case, you have to pay LTCG tax on the remaining Rs 10 lacs. On the other hand, you can use LTCG from sale of more than one residential property to purchase/construct a house and avail benefits under Section 54.

- There is no exemption if you purchase/construct the house outside India.

- If you cannot purchase/construct a new house by the due date of filing return for the financial year in which you sold the house, you must deposit the unutilized capital gains in an account opened under Capital Gains Deposit Account Scheme. Withdrawals from the account can be made for purchase/construction of a house. This is discussed later in the post.

Quantum of Relief under Section 54

If all the conditions mentioned above are met, you shall get tax relief up to:

- If the cost of the new house is greater than the long term capital gains, the entire long term capital gains shall become tax exempt.

- If the cost of the new house is less than the long term capital gains, the relief shall be to the extent of the cost of the house. You will have to pay tax on the remaining amount.

For instance, you had LTCG of Rs 50 lacs on sale of a residential property. If you purchase/construct a property for Rs 60 lacs, the tax relief shall be Rs 50 lacs (LTCG).

On the other hand, if you purchase/construct a new residential property for Rs 40 lacs, the tax relief shall be limited to Rs 40 lacs (cost of new house).

What if I am able to utilize only a part of LTCG in purchasing/constructing a new house?

In such a case, you get the benefit under Section 54 only to the extent LTCG is utilized to purchase/construct a new house within the specified time limits.

For example, if you had LTCG of Rs 50 lacs and you purchase a house for Rs 30 lacs, then you will get relief on Rs 30 lacs. For the remaining Rs 20 lacs, you will have to pay long term capital gains tax at 20%.

Can I use LTCG on sale of a residential property to purchase a commercial property?

Of course, you can but you won’t be entitled to benefits under Section 54 if you use LTCG to purchase a commercial property, say a shop.

The long term capital gains have to be used to purchase/construct a residential property.

Can be benefit availed be reversed?

Yes, the benefits can be reversed. This can happen if you sell the new residential property within 3 years from the date of purchase/completion of construction of the new house.

In such a case, for the purpose of calculation of long term capital gains on the sale of new property, the benefit availed under Section 54 shall be deducted from the cost of acquisition of the property.

Let’s try to understand with the help of an illustration:

Illustration 1

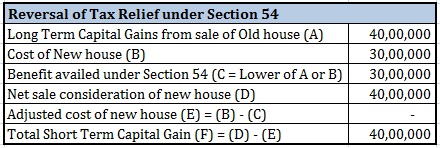

You sold a residential property in the June 2012. You had purchased this house in the July 2005. The sale transaction resulted in long term capital gains of Rs 40 lacs. To avail tax relief under Section 54 of the Income Tax Act, you purchased a new residential house in July 2013 for Rs 60 lacs. You sold this new residential property in January 2015 for Rs 80 lacs.

Since you sold the residential property within 3 years from the date of purchase, the benefit of Rs 40 lacs availed under Section 54 shall be deducted from cost of new property.

You can see total short term capital gain is Rs 60 lacs in FY2016. You will have to STCG tax as per your income tax slab. Since the new house has been sold before completion of 36 months, the house is a short term capital asset. There shall be no benefit of indexation either as this benefit is available to only long term capital assets.

If you fall in the highest tax bracket, you will have to pay tax of Rs 18 lacs in FY2016. Surcharge and cess shall be extra.

Illustration 2

You sold a residential property in the June 2012. You had purchased this house in the July 2005. The sale transaction resulted in long term capital gains of Rs 40 lacs. To avail tax relief under Section 54 of the Income Tax Act, you purchased a new residential house in July 2013 for Rs 30 lacs. You sold this new residential property in January 2015 for Rs 40 lacs.

In this case, the cost of new house is less than the LTCG of Rs 40 lacs. You would pay tax of Rs 2 lacs (20% of Rs 10 lacs) in FY 2013. Surcharge and cess shall be extra.

For FY2016, your STCG will stand at Rs 40 lacs. If you fall in the highest tax bracket, your STCG liability comes to Rs 13.3 lacs in FY2016. So, you end up paying total tax of Rs 15.3 lacs (Rs 2 lacs in FY2013). This does not include surcharge and cess.

Capital Gain Account Scheme

Though you have time of 2 years for purchasing a new house or 3 years for constructing a new house, the Income Tax Department cannot be sure of your intentions. Hence, you have to purchase/construct the new house before filing income tax return for the financial year in which you sold the house.

However, if you sold the house in January 2015, it may not be possible to purchase or construct a new house by July 31, 2015 (due date of filing income tax return for FY2015). In such cases, you can deposit long term capital gains (whole or part) in Capital Gains Account Scheme, 1988 before the due date of filing returns (or your actual date of filing return, whichever is earlier). The funds in the Capital Gains Account can only be utilized to purchase/construct a house.

Hence, the unutilized capital gains amount can be put in Capital Gains Account before filing income tax return for the financial year in which the sale was made. And the return needs to be filed on or before the due date of filing returns.

With this, the Income Tax Department can be sure of your intentions and give you relief under Section 54.

Where can I open Capital Gains Account?

Capital Gains Account can be opened with 28 Public Sector Banks. You can open both savings (Type A) and term deposits (Type B) accounts. The funds from the account can only be utilized towards purchase or construction of house.

You will have to submit proof of deposit in such account while filing your returns to claim tax exemption on long term capital gains under Section 54.

Interest earned on the account is taxable. You can get more details about the account from the nearest bank branch. For the list of features for Capital Gains Account offered by Punjab National Bank, you can visit this page.

Can the benefit be revoked?

Yes, if the amount deposited in the Capital Gains Account cannot be utilized (wholly or partially) for purchase or construction of house within the specified period (2 or 3 years as the case may be), the unutilized amount shall be taxed as long term gains when the specified period ends.

For instance, if you sold a residential property on January 15, 2012 for a long term gain of Rs 40 lacs, you must either purchase a new house by January 14, 2014 or construct a new house by January 14, 2015 to avail benefits under Section 54.

However, you need time to finalise the purchase deal or construct a new house and cannot do the same before July 31, 2013 (or the due date specified by IT department). To avail benefit under Section 54, you must deposit Rs 40 lacs in a Capital Gains Deposit Scheme Account by July 31, 2013 (or the specified due date of filing return).

If you don’t deposit the unutilized capital gains amount in Capital Gains Account by July 31, there shall be no relief for the unutilized Capital Gains under Section 54.

You can make withdrawals from the said account to purchase a house (till January 14, 2014) and construct a house (till January 14, 2015). For any unutilized amount in the account beyond the specified period, you will have to pay LTCG tax.

Let’s consider various scenarios:

- You purchased or constructed the house within specified time: You get the complete benefits under Section 54 i.e. the tax benefits are not revoked.

- You did not utilize the amount within the specified time: The specified time of 3 years (for constructing the house) gets over on January 14, 2015. The benefit availed under Section 54 shall be revoked and you will to pay long term capital gains tax on Rs 40 lacs while filing returns for FY2015.

- You utilized the amount only partially: You used Rs 30 lacs to purchase a new house on December 12, 2013. For the remaining unutilized amount (Rs 10 lacs), you will have to pay LTCG tax while filing return for FY2015. For purchase of a house, the deadline was January 14, 2014. Since Section 54 allows exemption for purchase/construction of only one house, funds had to be utilized by January 13, 2014 (since you had used the funds for purchase of house). You will have to pay long term capital gains tax on Rs 10 lacs in FY2015.

I do not want to invest in another residential property. What do I do?

If you do not want to invest long term capital gains from sale of your house into another residential property, you cannot claim any tax relief under Section 54.

However, you can claim tax relief under Section 54EC. Under Section 54EC, you can get tax relief by investing in capital gains bonds of NHAI (National Highway Authority of India) and REC (Rural Electrification Corporation) within six months from the date of sale of capital asset. Maturity of these bonds is 3 years. Interest rate, currently on offer is 6% per annum. You can find more information about these bonds of websites of NHAI and REC. You can find more information about capital gains bonds offered by NHAI for FY2015-2016 here.

Non-resident Indians (NRIs) can also avail benefit under Section 54EC.

- You can avail relief under Section 54EC for all long term capital assets (and not just residential house). So, you can avail for gains on commercial property, debt, gold etc.

- Only long term capital gains are eligible for tax relief under Section 54 EC.

- You cannot invest more than Rs 50 lacs in these bonds in a single financial year. Thus, benefit under the scheme is limited to Rs 50 lacs per financial year.

- In any financial year, tax relief under Section 54EC shall be limited to the amount of investment in the specified bonds or Rs 50 lacs, whichever is lower.

- Cumulative investment in specified NHAI and REC bonds in the year of sale of asset and the subsequent year shall not exceed Rs 50 lacs. This is to ensure that the assessee does not split the long term capital gains in two financial years. For instance, in absence of this clause, on LTCG of Rs 1 crore in December, you could have invested Rs 50 lacs each in March and April of next calendar year and got relief for entire Rs 1 crore under Section 54EC.

- The LTCG must be invested in these capital gains bonds within six months of the sale of long term capital asset. Practically, you will have to do it before filing returns for the financial year in which the asset was sold.

- If at any time within 3 years from the date of purchase of these bonds, you sell or take loan against these bonds (or monetise these bonds in any way), tax benefits under Section 54 EC will be revoked.

- Additional point to note is that total relief under Section 54EC is also limited by the amount of bonds NHAI and REC choose to issue. However, at current rate of 6%, this is likely to be the cheapest cost of finance for these entities.

PersonalFinancePlan Take

You can save tax on Long Term Capital Gains on sale of residential property by using capital gains to invest in a new residential property. Do remember there are time timelines to adhere to for purchase/construction of new house.

Be sure of what you want to do with the long term gains. If you want to purchase/construct a new residential house, seek relief under Section 54.

If you do not want to purchase a new property, use the tax benefit under Section 54EC (rather than availing benefit under Section 54). This way, your tax benefits won’t be revoked at the end of 3 years.

As I understand, you cannot claim relief under both Section 54 and Section 54EC for long term capital gains on the same property i.e. For LTCG of Rs 40 lacs on sale of residential property, you cannot use Rs 30 lacs to purchase a new property(Section 54) and invest remaining Rs 10 lacs under NHAI/REC bonds (54EC). You can take relief under one section for sale of one property, not both.

List of sections under which tax relief for long term capital gains can be sought is provided below. I have not discussed Section 54F in this post because the benefit under this Section is only for long term capital assets other than residential houses. However, I have included it in the table for the sake of completion.

Image Credit: The original image and information about usage rights can be downloaded from Pixabay.

Disclaimer: I am not a tax expert. This is a simplistic description of income tax laws. The exact rules may have multiple sub-conditions. It is not possible to include all sub-conditions in this short post. You are advised to consult a tax consultant to understand your tax liability better.

Deepesh is a SEBI registered Investment Adviser and Founder, PersonalFinancePlan.in