Healthcare costs are rising fast and a health insurance plan can secure your family’s finances against medical emergencies or prolonged hospitalization. Not just that, a health insurance plan also ensures that you can provide quality healthcare for your family.

Most informed people have either purchased health insurance already or are planning to add one to their insurance portfolio. Even those who are covered under their employer’s group health insurance plans are now exploring personal health insurance plans. The common refrain (and rightly so) is that employer group health insurance plans do not offer adequate coverage for the entire family or have too many sub-limits. They are quite right. A cover of 4 lacs for a family of 6 (Self, spouse, 2 kids and parents) is simply not going to be enough. With such cover, be prepared to shell out heavily from your pocket in case of prolonged hospitalization.

Please read this post to find out more about parameters you must consider while purchasing health insurance. To know more about how to start researching health insurance plans, please read this post.

Individual Health Insurance Plan or a Family Floater Plan

You have decided to purchase a personal cover.

Now, there is another question to answer.

Whether they should go for individual health insurance plans for each of the family members or go for a single family floater plan for the entire family.

Under a family floater plan, the entire family shares a common pool. A family floater plan provides cover to the entire family to the extent of the Sum Insured.

Sum Insured is the maximum payout that the insurance company would make in a policy year.

The total claim amount that shall be reimbursed by the company for the treatment of all the family members shall be limited to Sum Insured.

If you have bought a family floater plan of Rs 10 lacs for a family of four, the insurance company will reimburse hospitalization expenses up to Rs 10 lacs per policy year. These Rs 10 lacs can be used by a single person or all the family members combined.

Let’s consider an example. For a family of four (self, spouse and 2 kids), you can purchase individual health insurance plans with a Sum Insured of Rs 5 lacs each. Alternatively, you can purchase a family floater plan with Sum Insured of Rs 20 lacs (or Rs 10 lacs as the case may be).

Under the separate individual plans, hospitalization expense of each of the members will be reimbursed up to a maximum of Rs 5 lacs. For instance, if you get hospitalized and the treatment bill runs up to Rs 7 lacs, the health insurance plan will only pay up to Rs 5 lacs. You will have to pay Rs 2 lacs from your pocket. On the other hand, if you had gone for a family floater plan, the entire Rs 7 lacs would have been reimbursed by the company.

Additionally, if you get hospitalized again during the same policy year, there will no further payout from the individual plan as you have used the entire limit. Had you purchased a family floater plan, there would still be Rs 13 lacs of cover left. The remaining cover can be used by you or any of your family members during the policy year.

Premium Comparison: Individual Health Insurance Vs. Family Floater

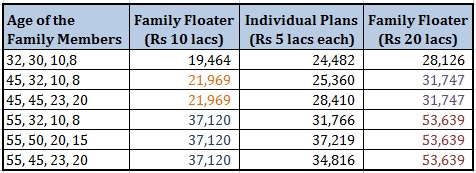

I compared the premium amount for the four individual policies with the premium for the family floater policy for Apollo Munich Optima Restore Plan. Individual policies will cost a total of Rs 24,482 (Ages 32, 30, 10, 8). On the other hand, the family floater plan (of Rs 20 lacs) would have cost Rs 28,126. Since it is not very likely that the entire family would be hospitalized in the same year (apart from accidental cases), you could have gone for a lower cover under the family floater insurance plan. You will have to pay Rs 23,330 for a floater cover of Rs 15 lacs and Rs 19,464 for a cover of Rs 10 lacs.

Looking at the premium, you would be compelled to think that you should purchase family floater plans only. They provide greater coverage (as a single person can use the entire amount) and are not very expensive either.

Well, things are never so simple. Let’s consider a few aspects.

The premium for the Family Floater Plan depends on the age of the eldest member

A chain is only as strong as its weakest link. And an insurance company will price the company based on the weakest link. Therefore, the premium of a family floater will depend on the age of the eldest member and the health of the weakest member.

The Premium of the family floater, typically, depends on the age of the eldest member of the family. Let’s look at the premium amount for Apollo Munich Optima Restore Plan for a family.

You can see that the premium depends on the age of the eldest member of the family. So, essentially, it is a function of the age of the eldest member and the number of members in the family. The choice between the two plans depends on the family structure and the age of the eldest family member. Old age of any of the members, in an otherwise young family, will shoot up the premium of the family floater plan.

Please note any premium amount is for healthy citizens. If you (or any member in the family) have an illness that increases hospitalization chances, the insurance company may load (increase) the premium amount. Additionally, I have made the inference based on premium amounts for Apollo Munich Optima Restore Plan. Other insurance companies may follow different underwriting process and may offer entirely different results.

In case of pre-existing illness, loading will apply on premium for the entire family

At the time of purchase of the policy, if a person has an illness that increases the likelihood of getting hospitalized, insurance company loads (increases) the health insurance premium for such a person. It makes sense too. Because of that illness, the risk of the insurance company has increased. They are more likely to make a claim under the policy.

Hence, if you are purchasing a family floater plan and any member has such illness, the insurance company will load the premium for the entire family (entire Sum Insured). The reason is simple. Under the family floater, a single person can utilize the entire cover. To the insurance company, it does not really matter if one member utilizes the entire cover or 4 members utilize it. They have to make the same payment. So, even if a single member has a specific illness, they load up the premium for the entire family.

If you had you gone for a separate individual health insurance plan for each member, the premium for only that specific individual member would have been loaded (increased). No such increase in premium would happen for the remaining members.

Hence in such cases, it may be a better idea to purchase separate plans for each member of the family. Alternatively, you can purchase an individual plan for the specific individual while the rest of the members can be part of the family floater plan.

Even at the time of enhancement of Sum Insured, loading will apply

Please understand Claims based loading is not permitted by IRDA, the insurance regulator. This means a health insurance company cannot increase your premium at the time of renewal just because you made a claim in the previous policy year. The insurance company can increase it because of your age or due to their overall claim experience (and not your individual policy claim experience).

However, if you choose to enhance the cover at the time of renewal, the premium for the enhanced Sum Insured will be loaded if any member has any illness (that increases the likelihood of getting hospitalized) or has contracted such illness since the inception of the policy.

For instance, you purchased a family floater of Rs 5 lacs 2 years ago. At the time, you had no such illness. However, in the last two years, you developed a major kidney problem and had to be hospitalized. As per IRDA guidelines, the insurance company won’t be able to increase your premium just because you made a claim.

However, if you plan to increase the coverage from Rs 5 lacs to Rs 7.5 lacs, this extra cover of Rs 2.5 lacs will be subject to fresh underwriting and the premium for this extra amount can be loaded.

As mentioned before, if you have a family floater, the premium for the entire family will be loaded.

Family Floater Plans suit young families more

- For a young family, the chance of two or more members falling ill (and getting hospitalized) in the same policy year is relatively low. Hence, in a way, each member can enjoy much higher coverage than they would have if you had purchased an individual plan for each of them. For instance, you can either purchase an individual plan of Rs 2.5 lacs for each member in a family of four. Or you can purchase a family floater of Rs 10 lacs (or even less) for the entire family. If there is just one hospitalization in a year, you get coverage up to Rs 10 lacs for that hospitalization. For young families, the premium for family floater plans can be comparable or even cheaper than multiple individual plans.

- As the family ages, the probability of getting hospitalized increases. The chances of two or more members falling ill in the same policy year also increase. At that time, it may make sense to shift to individual plans or opt for a higher floater cover.

- For instance, for a younger couple, rather than purchasing 2 individual polices policies of Rs 5 lacs each, you could have done with a family floater plan of Rs 5 lacs or Rs 7.5 lacs (instead of Rs 10 lacs). The rationale is that the chance of both getting hospitalized in the same policy year is low. However, as the couple grows older (age of 50 or more), this probability increases. Hence, it makes sense to opt for a larger family floater cover (5+5=10 lacs).

- Typically, your children will be covered under your family floater plan only till such time they turn 25. After that, they will have to purchase (move to) fresh individual plans. Continuity benefits (for the waiting period for pre-existing illness) shall apply.

Should I purchase individual policies or a family floater policy for my parents?

A few policies allow you to add parents to your family floater plans. Do not include your parents in family floater plans. As pointed out, the premium for the family floater depends on the age of the eldest member. The premium for the family will shoot up unduly.

Purchase separate individual health plans for each of them. Or purchase a family floater plan that covers both of them.

If any of them has an illness that increases chances of hospitalization, it makes even greater sense to go for individual policies. The reason is if you purchase a family floater, the premium for both the members (entire Sum Insured) will be loaded.

If none of your parents has any serious illness, you can purchase a family floater plan for them too. Just make sure that the Sum Insured is adequate for both and does not require revision anytime soon. There is a drawback with this approach. If you choose to enhance the premium after sometime (and one of them has contracted a major illness since the inception of the plan), the premium for both of them will be loaded.

Therefore, for people above 45 or 50, I recommend individual health insurance plans than family floater plans. In a family floater plan, the bad health of one member can increase the premium for all the members (entire floater Sum Insured). Please note this shall happen only at the time of purchase of health cover or enhancement of cover at the time of renewal.

Do note this choice of the age of 45 or 50 is a bit subjective. You can check for your family and the policy chosen.

Read: Use this Smart Health Insurance Strategy to reduce Premium

Read: Health Insurance Strategy for your parents

What should you do?

Family floater plans are better suited for young families, where the chances of hospitalization are relatively low. For people above 45 or 50, it is better to purchase individual plans rather than family floater plans. At least the older members can be part of individual plans while the other members can be part of a family floater plan. I have discussed this aspect in great detail in this post.

You can begin with a family floater plan as you start your family and move to individual plans as you (and the family) grow older and your premium affordability increases.

I have seen a few people using a mix of individual and family floater plan to complete their health insurance portfolio. There are top-up and super top-up health insurance top-up plans available too. So, you can structure your health insurance portfolio in many different ways to suit your specific needs.

And yes, irrespective of whether you choose separate individual plans or a single family floater plan, the health insurance cover should be adequate.

Which one do you prefer? Individual Health Insurance or Family Floater Plan?

The post was first published in October 2015.

Image Credit: Pictures of Money, 2014. The original image and information about usage rights can be downloaded from Flickr.