LIC Jeevan Labh (Plan 936) is a limited premium and non-linked participating life insurance plan.

“Limited Premium” implies that the premium payment term is lower than the policy term.

“Non-linked” means LIC Jeevan Labh (Plan no. 936) is not a ULIP. It is a traditional life insurance plan.

“Participating” means you will participate in the profits of the insurer. Your bonus (reversionary or final) will depend on LIC’s performance and therefore can’t be known upfront. Thus, you cannot calculate your returns upfront. You can do that in “Non-participating” plans.

We have seen time and again that traditional life insurance plans are poor products. Such products neither provide you good life cover, nor provide your good returns. And I do not expect this new avatar of LIC Jeevan Labh to be any different.

Let’s find out more about this plan in this post and see if makes sense to invest in such a plan.

Note: I had first written this post about LIC Jeevan Labh (836) in 2016. The LIC withdrew LIC Jeevan Labh 836 in 2020 and launched a new plan LIC Jeevan Labh 936. As I see, there is only a minor difference between the 2 variants. I have updated the post for LIC Jeevan Labh 936.

Buying an insurance product: How to figure out what you are buying?

It is not easy to pen down all the thoughts about a product. Therefore, I have also reviewed the LIC Jeevan Labh (936) in greater detail in this video. Do check out.

LIC Jeevan Labh (Plan 936): Salient Features

- Limited premium payment plan i.e. premium payment term is less than policy term

- Premium Payment Terms of 10/15/16 years for policy terms of 16/21/25 years respectively

- Minimum Entry Age: 8 years

- Maximum Entry Age: 50/54/59 years for policy terms 25/21/16 years respectively

- Minimum Basic Sum Assured: Rs 2 lacs

- Maximum Basic Sum Assured: No upper limit

You can find out more about LIC Jeevan Lab plan on LIC website.

You can see there are only three possible combinations. If you pick up plan with premium payment term of 15 years, you will pay premium for 15 years while you will get life cover for 21 years. You will get the maturity amount at the end of 21 years (if you survive the policy term).

I do not see much difference between LIC Jeevan Labh and LIC New Endowment plan. The only difference I see is that LIC Jeevan Labh is limited premium payment plan. LIC New Endowment plan is a regular premium payment plan.

Difference between LIC Jeevan Labh (836) and LIC Jeevan Labh (936)

There are only a few minor differences.

Changing the Death benefit definition is a major change. For life insurance maturity proceeds to be tax-free, the minimum death benefit must be at least 10 times the annualized premium.

Therefore, there is a possibility that maturity proceeds from LIC Jeevan Labh (936) may not be exempt from tax. However, I tried to calculate premiums for various combinations of age and policy terms for LIC Jeevan Labh (936). The Base Sum Assured was always more than 10 times the annual premium. And since Sum Assured on Death is higher of (Base Sum Assured, 7 times annualized premium), you are safe. The maturity proceeds will be exempt from tax under LIC Jeevan Labh (936) too. Still, do ensure this if you plan to invest in LIC Jeevan Labh (936).

LIC Jeevan Labh (Plan 936): Death Benefit

In the event of demise during the policy term, the nominee gets

Sum Assured on Death + Vested Simple Reversionary Bonus (till date)+ Final Additional Bonus (if any)

Sum Assured on Death = Higher of (Base Sum Assured, 7 times annualized premium)

Simple Reversionary Bonus is announced every year by LIC. It is announced as per thousand of Base Sum Assured. So, if the Sum Assured is Rs 10 lacs and the bonus is announced as Rs 40 per thousand of Sum Assured, your annual bonus is Rs 40,000.

The caveat is that LIC does not credit your bank account with reversionary bonus every year. The bonus merely gets added to maturity amount and is paid at the end of policy term. No compounding benefit. Continuing with the same example, if LIC announces the same bonus for the next 25 years, your policy would accrue 40,000 X 25 = Rs 10 lacs in the next 25 years and this amount is payable to you at the time of maturity (25 years). In the event of demise too, the LIC will pay the accrued bonuses till date. As you can see, no returns on the accrued bonus.

Final Additional Bonus is applicable only in the year of maturity/death. So, it is a roll of dice. It is also expressed as per thousand of Sum Assured.

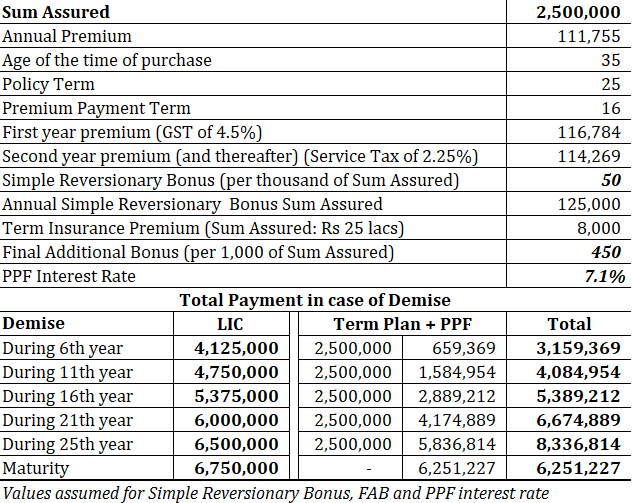

LIC Jeevan Labh (Plan 936): Maturity Benefit Illustration

Maturity Benefit = Base Sum Assured + Vested Simple Reversionary Bonus + Final Additional Bonus (if any)

LIC Jeevan Labh (836) has bonus history for 6 years. LIC Jeevan Labh (936) has bonus history for 2 years.

As you can see, the bonus value can change every year. For the illustration, I will use an optimistic estimate for Simple Reversionary Bonus. Moreover, the bonuses for Plan 836 and Plan 936 are the same. That’s expected.

Bonus increases with policy term. A 16-year policy earns a lower bonus compared to 25 year policy.

Final Additional Bonus, in any case, depends on your luck. I will consider various value of FAB to assess investment performance.

Now, these returns are not special for a long term investment. We considered a 25 year policy term.

At the same time, the returns are tax-free and do not look too bad for a fixed income product. Currently (as on September 8, 2022), PPF offers 7.1% p.a. and it does not offer any insurance. Of course, these returns from LIC Jeevan Labh are not guaranteed and a lot depends on the bonuses that LIC will announce over the policy term. We have already seen that the bonuses can go down (went down from 50 to 47 in 2020 and has stayed there since). I have considered a value of 50 for this analysis. It is possible that these bonuses may reduce further (or increase). Such changes will impact your returns.

Now, consider these returns with the lack of flexibility in LIC Jeevan Labh. You can’t surrender your plan without a heavy penalty. And there are these usual problems with all traditional plans. Therefore, I would advise you to stay away from LIC Jeevan Labh. There is no LABH in LIC Jeevan Labh.

Point to Note: With traditional plans, the returns depend of the entry age. Thus, everything else being the same (Sum Assured, policy term, same year of purchase), a 35-year-old investor would earn better returns from the plan compared to a 45-year-old (at the time of entry). This happens because the premium goes up as the age goes up.

For instance, a 45-year-old would have to pay an annual premium of Rs. 50,937 for the same policy (Rs 10 lacs, Policy term of 25 years). The maturity amount would be the same since bonuses are linked to Sum Assured. Higher premium reduces effective returns. IRR for 45-year-old would be 5.89%, 6.13%, 6,37% and 6.59% for various values of FAB as shown above.

Moreover, the returns will be higher for longer policy terms. You just need to look at the bonuses announced. Lower the policy, lower the bonus. And this applies to both reversionary bonus and the Final Additional bonus.( FAB) Yes, FAB also depends on the policy term. For instance, in FY2021, the FAB announced for 25 year policy was 450 per Rs 1000 Sum Assured. For a 16 year policy, it was Rs 25 per Rs 1000 Sum Assured.

I considered a 16-year policy. 35-year-old. Sum Assured of Rs 10 lacs. Annual premium of Rs 85,181 per annum. Simple Reversionary bonus of 43 for the entire term. FAB of 0. The IRR was 5.78% p.a. For 25-year policy, it was 6.34% p.a. (for FAB of 0).

Could you have done better with Term Plan and PPF?

And I am not even talking about equity mutual funds.

I checked the annual premium rates for 25 lac cover on Policy Bazaar. For 35-year-old and 25 year policy term. The premiums were in the range of 6,000-10,000 per annum. So, instead of putting money in LIC Jeevan Labh, we buy a term life insurance plan and invest the remaining in PPF.

You can see combination of term plan and PPF is right there with LIC Jeevan Labh (expect at maturity). In my earlier analysis, PPF + Term plan was a clear winner. However, PPF rates have come down since then. But I have kept the bonus rates high. Thus, tilting the results in favour of LIC Jeevan Labh.

Had you replaced PPF with equity funds (or a balanced portfolio), you could have ended up with a much higher maturity corpus.

Since LIC Jeevan Labh premium payment term is only 16 years, how do you account for term insurance premium in the years 17 till 25th. I have withdrawn term insurance premium from accumulated PPF corpus. Yes, you can withdraw from PPF after initial maturity of 15 years.

What should you do?

I do not like traditional plans. And I do not deny my opinion is biased.

We saw earlier that LIC Jeevan Labh does not provide good returns for a long term investment, even though returns may not be bad for fixed income product.

Keep your insurance and investment needs separate. It is just so simple. You buy better life coverage. You may need a life cover of Rs. 1 crore. If you try to purchase life cover through a product like LIC Jeevan Labh, you will have to shell out Rs 4-5 lacs per annum. Now, that’s a very high premium. You might settle for a lower life cover (based on your premium payment ability). And this exposes your family to a huge financial risk. On the other hand, a term plan of Rs. 1 crore may cost only 10-15K per annum. With a term plan, you will likely not remain underinsured.

Plus, you get more flexibility with money.

Moreover, you can replicate (and perhaps even outperform) performance of traditional plans using a combination of term life plans and PPF (or mutual funds). There is no LABH in LIC Jeevan Labh. Stay away.

Additional Links

- LIC New Jeevan Anand

- LIC New Money Back Plan-25 years

- LIC Children’s Money Back Plan

- LIC Jeevan Tarun

- LIC New Endowment Plan

Featured Image Credit: Unsplash

The post about LIC Jeevan Labh was first published in September 2016 and has been updated since for LIC Jeevan Labh (936).

91 thoughts on “There is no LABH in LIC Jeevan Labh (Plan 936)”

nice info

but worry is, PPF interest rate will reduce in future.

I don’t know about LIC interest rates..

If PPF rates go down, expect LIC bonuses to go down too.

KINDLY GIVE ME SOLID PROOF ON WHAT BASIS YOU ARE EXPECTING LIC BONUS RATE WILL GET DOWN.

EXPECTATION AND REALITY BOTH ARE DIFFERENT.

BEFORE ANSWER GO THROUGH BONUS RATE FROM 1956 TO TILL NOW.ALSO WHILE COMPARISON OF LIC WITH YOUR MUTUAL FUND TALK ABOUT RISK ADJUSTED RATE OF RETURN FOR MUTUAL FUND.

Where do you think LIC invests?

PPF rate will go down over the long term if the Government bonds yields go down slide the long term.

LIC bonus rate will also get affected. Ofcourse, LIC may be able to manage due to their old holdings at higher rates due to old holdings (at higher interest rates) but won’t be able to hold bonus rates high for too long.

LIC does not pay policyholders from own pocket. It must earn good return to give you okayish returns. Returns with LIC plans have been great in any case.

So, it cannot happen that PPF rates crash while LIC continues to announce decent returns.

Wat is basis for bonus rates? Are you expert enough in Insurance Mr Deepesh before commenting on social platform. LIC has got 60 years history ultimTely contributing to countries development, are you doing same.

I rely on numbers and fair assumptions. I have laid my logic down in the post. You may or may not agree with my assessment. So be it.

If you don’t, you can free to invest in Jeevan Labh.

If you are a LIC agent, request you to ask your clients to read this post once and let them make a choice.

I myself have invested in MF and LIC policy. I feel my money is more secured in LIC than in market risk scheme. Since I have not gained much in hdfc top 200 which was very much hyped during 2009-10 period. I am not LIC Agent but have great respect for my agent for providing all support to me during claim.

Thanks for your inputs. There is no reason why you should not respect your agent.

The problem is with traditional plans. And the issue is not with LIC. Many private insurance companies come with similar plans.

MR DEEPESH UR MISLEADING PUBLIC EVERY COMMON MAN KNOWS ABOUT LIC ITS TRUSTED GVNG MORE RETURNS

I did not say that I don’t trust LIC. Just that returns are bad.

Hi Deepesh-

Very good detailed info with examples, i appreciate the effort you have put in to explain to the common man who has no idea about investment/insurance.

You are welcome, Raghuram!!!

Do share the post with your friends.

Does term insurance provide disability benefit? What about compulsory investment since there is lot of indiscipline in mutual fund Investments.. In ppf we are not committed to the investment amount which is required to achieve long term goal. I seriously belive that we should invest in all baskets.

Dear Rajiv,

Yes, you can purchase disability rider in term plans too. Discipline can be developed.

But no amount of good discipline can convert a poor product into a good one.

Btw, you have SIPs in mutual funds that you can use. You can set debit instructions in your bank account for PPF investment.

So, discipline aspect can be managed.

As far as I know disability benefit is provided on loss of any 2 limbs or more than 50% disability which is provided under Accident Rider n there is no accident rider in Term Insurance plan. Few facts cannot be ignored, It is very important to have good knowledge about market schemes with regular observation, In our daily routine its tough to keep track. One more thing to be noted there are few advisors(MF) in market to cover huge mass of our country since SEBI has demotivated them by cutting Commission rates. For long run mutual funds on paper may seem good but practically difficult to get expected results

Very nice explain rajeev…

Hi Rajiv,

With a term plan, you can purchase both accidental disability and accidental death rider.

I agree with you to an extent. Selecting MFs may not be easy for everyone. However, you do not really require regular observation. Annual review will suffice.

SEBI’s intent is investor friendly. But yes, how it impacts the distribution chain and overall investor participation remains to be seen.

Thanks a Ton, you have opened my Eyes

Thank you Suresh

First understand what is LIC and then it’s plans & there features. Please don’t spread negative words.

Are u still worried about lic bonus rates/returns?

Ex- people bought j akshay in 1994 @14% interest rate. At that time banks were giving 15% so those who invested in j akshay still getting 14% boss…this is the power of LIC that inspite of paying such higher interest rate it is growing day by day, year by year .

Now how come u are negatively marketing such organization.

I can expect that with you as you are so called SEBI registered advisor so u ll be marketing yourself and MF only…

Pls dont misguide people…

Dear Krishna,

I have nothing against LIC. I only have issues with the kind of plans LIC or other private insurance companies come out with.

I compared LIC plan with LIC term plan and PPF.

Where is the mutual fund angle?

Sir you are targeting LIC products only when lics I mean, lics policyholders big contribution For our country’s development.

You are Ignore here pvt insurance company product…

I think you are marketing Mutul fund products here..

Thanks sir

I am a fine person in a fine job, working for a fine institution

And life insurance is the most wonderful thing in the world,

This I believe Life Insurance Corporation of India..

Hi Vinod,

Thanks for your comments.

No, my target is not LIC. My posts are about traditional plans.

Private insurers such as ICICI Prudential and HDFC Life also come out with such plans. Those are also bad.

Yes, Life insurance is quite important. In my opinion, a traditional life insurance plan is not the right mode to purchase it.

In life, peace and ability to sleep well at night is very important.

If your LIC policies let you sleep well and you are ok with low returns, ignore what people like me have to say. Enjoy life.

I used PPF for analysis. Don’t know how equity mutual funds came into picture.

i dont know how you can guige peole to invest in mutual funds which can give you 15% return (if i am not wrong mutualfunds is also like buying stakes of companies) just want to say that if your small companies(in the comparision with LIC) can give 15% return through MF why cant lIC of India give 7 or 7.5%. i know that you”ll not going to digest this. suppose if i am goint to invest for my child’s education i dont think mutual find is good for that.because your investment is not safe there, it can provide you return more then you expeted but you can loose your capital too.

if i am wrong can you tell me the meaning of that last line which comes after all mutual funds add

(all the investments are the subjected to market risk please read all the documents carefully before investing) i am not against mutual funds you can invest in mutual funds also but it is not good to compare these two.(apple and orange, both are good fruit you cant compare these two).

Hi Chetvir,

Thanks for your inputs.

I am not comparing traditional plans with mutual funds. I am merely saying traditional plans are bad investments.

There is risk in even stepping out of our houses. But we do go out. Don’t we?

Similarly, there is risk with investments too. You need to see if you are ok with taking such risk.

If risky investments don’t let you sleep peacefully, don’t invest there. Simple.

I have nothing against LIC either.

Which Traditional good return plan is best for this generation, LIC or private insurance provider?

Any person who thinks of family security after this death and to secure his spouse or kids.

Purchase a term insurance plan from LIC.

Deepesh, I went through your profile & it really surprised me as to how can a educated(financially literate) person give reviews & compare Insurance & Investment.

Both are 2 different things & are incomparable in any regards.

LIC provides Security along with safety which is absent in MFs.SEBI’s very own survey says that very few MF investors remain invested for more than 5 years.

How can a 30 year old achieve his retirement corpus after 30 years if he keeps booking profits & redeeming in crisis,given the liquidity offered.

As it is,literacy rate in India is less.Moreover, financial literacy is hardly accountable.

Double Accident Benefit, Disability benefits,Term Rider,Risk Cover are the various benefits in the insurance plan.

They are the most Disciplined source of savings due to non liquidity offered.

Nevertheless,few degrees doesn’t just help gain financial wisdom. Getting to the grassroot level, interacting with people of all segments would definitely add to ur knowledge

Even I am surprised by his analysis. I hope Deepesh you are not misguiding people by such negative post.

Dear Samson,

You can make personal remarks, if you so wish.

It will not change my opinion or the truth.

Dear Prasad,

Yes, insurance and investment are not comparable. I just want to go a step further and say that it is better not to mix them.

You do not have to compare traditional plans with MF.

If forced saving is your criterion, ULIPs are far better than traditional plans and force people to save.

Have you tried explaining to people that traditional plans provide poor returns? Suggest you try that. You don’t have to assume that people won’t understand. They may as well.

Yes, a few degrees don’t make a person financially savvy. However, selling poor products to people with a bizarre assumption that people can’t understand does not make any one a financial expert either.

Hi Deepesh

I had read somewhere on internet that the maturity amount on jeevan labh is totally tax free. You get whole amount without any deduction is it right?

Tell me then why people always choice LICI policy. It gives 60 year service. If you ask to join some benefit to jeevan labh then what benefits will you join. There are menny expert investment advisor at LICI. And they atfast stady the market then publish the police.

Dear Kuntal,

Thanks for your inputs.

People buy because it is LIC. There is immense trust that people have in LIC. And that’s why they invest.

I have nothing against LIC. LIC is a great instution. I am sure LIC has many brilliant investment minds. Therefore, it is not about questioning their ability. Moreover, LIC has to sell what people want to buy. And people want to purchase traditional plans.

Just that I have strong opinion against traditional plans. And private insurance companies issue such plans too. LIC is not the only insurance company that comes out with traditional plans.

Still confused Should i go for it or not…

Same here

I have written the entire post on “you should not”.

My answer will not change.

I had heard, “A little knowledge is dangerous”. Someone proved it.

Hi Shubhendu,

It is clear you did not like the post.

Nothing wrong in having a difference of opinion.

Could you please point the mistakes in the analysis? Will help other readers too.

Disparaging comments do not help anyone.

Hiii Deepesh sir

I m so confused which plan is best of LIC..

Jeevan labh or jeevan anand…

Plz guide me…

What would u suggest, i should go with LIC jeevan lab or LIC jeevan anand or LIC term policy

Hi Vikas,

I don’t like either.

But if you have to choose one, Jeevan Anand may be a better choice.

Hi Deepesh,

Thank you for reviewing the product. I do not hold any degree in finance and hence wont be able to correct anyone on the basis of the argument. However, I would say your analysis is pretty close to my understanding I am having ever since I started investing 5 years back. I am 28 and having fair amount of my salary diversed into equity trading, SIP, Mutual funds and Term Insurance. Yes, as you said, one should not mix Insurance with returns. If you are solely looking for insurance, nothing is better than term plan. As returns on the investment plans of LICs are nothing special if you look at the market scenario. My father made a mistake of making investment in LIC which I sure would not repeat as gains are not at par with the market. In addition, I do not see or comprehend any extra-ordinary features of the plans offered by LIC. I failed to mentioned I have had a little share invested in PPF which, according to me, is the best one could have instead of sticking with LIC plans. Combination of PPF and Term plans would suffice your basic needs while your equity trading, SIP and Mutual Funds investments would come handy for any exigencies one may face throughout the career. One has to stay invested though for obtaining returns above par the banks or financial institutions offer.

Hiii Deepesh sir

I m so confused which plan is best of LIC..

Jeevan labh or jeevan anand…

Plz guide me…

What would u suggest, i should go with LIC jeevan lab or LIC jeevan anand or LIC term policy…

dear sir,

how to find lic rate of returns. i am very much confused whether to invest in jeevan labh or not.

details policy amt 500000

policy term 25 years

polivy paing term 16 years

premium first year (24887+st)

natural death cover 500000+bonus

accident rist cover 10,00,000+bonus

maturity after 25 years13,50,000

total premium paid 3,90,152

i

Dear Sonali,

If you are talking about returns, consider the maturity value alone.

Hi deepesh,

I have taken LIC Jeevan labh for 25 yr term last week. My moto is to get a good return at maturity. could you please suggest me if there any other better option should i go for.

My age is 30 single and package 6 lpa. haven’t taken any policy before.

waiting for your reply. Thanks.

Hi Jatin,

My article is about why you should avoid LIC Jeevan Labh.

So, not much to add here.

At your age, it will be good to take some equity exposure.

Mf and lic both are different products. But lic also has it’s unique features. It has long term, funds are secured, long term purpose can be solved, lic jeevan labh rate of return is 7.5 for 25 term and around 6.6 for 21yes term, which bank fd also don’t give, Tax benefit also is there tds bhi deduct nahi hota plus the risk cover, jeevan labh is also good for people who can’t pay premium for too long, eg. Retirement. I believe mf are good for good returns and risk. But just like pyramid we should have strong Base. Some investments should give fixed returns like bank fd and lic while some risky for more returns.

Hi Pinky,

Thanks for your inputs.

Hi Deepesh,

Thanks for your efforts. But I don’t understand the terms used here. I am looking to invest in some policy where I will get 35K per month from the age of 58. ie something like a fixed income during my retirement. My current age is 31 yrs old.

I came across Jeevan labh and Jeevan Umang and initially thought, I will pay 15K per month for 16 years. But if I am right then the amount payable per annum after 25 years is not known. Am I right? my agent made a rough calculations where I will be getting 5 lakhs per annum which is taxable.

On the other hand Jeevan Umang is assured but I get what I pay. For example if I pay 15K per month then I will get the same 15K per month. But after 25 years I don’t think it will be enough for me to manage the expenses.

I am quite confused on which one to decide. Could you clarify me please?

You are welcome.

If you have not yet purchased these plans, suggest you do not purchase Jeevan Umang or Jeevan Labh.

Hi Deepesh,

Thanks. Do you mind suggesting any other policy? Even Jeevan Umang is not good?

Thanks

I do not like traditional life insurance plans. Therefore, wouldn’t recommend Jeevan Umang either.

Good article Deepesh.cannot agree more.for all the agents who wrote above ,it is high time you have to change and tell people what is pure insurance and what is profitable investment.Since you people are not doing that ,plz dont try to misguide when somebody is trying to tell the truth.I had personal experience of LIC agent projecting this plans as the best for corpus creation!!.So all know they do lie to sell the products ,same can be the case with other companies also.He was only trying to light up the unknown side of all kichadi products which is neither good for insurance nor for investment…Kudos deepesh..keep up the good work.

Appreciate your inputs, Praseed!!!

Thanks for the support!!!

Do keep coming back for other articles on the blog.

Deepash you don’t like LI products hence you are against. It is not a way to say LI products are bad. Does your MF ensures the return ? whatever we see it is a assumption. NO Assurance. LIC traditional products are capable to assure the return and security. And no company can challenge the base and strength of LICI.

Thanks for your inputs.

We can always agree to disagree.

Btw, I like LIC too. The problem is only with the plans LIC comes out with. Private insurance companies come out with such plans too. Those plans must also be avoided.

I was told my insurance agent I will get 3756600.00 for 21/15 plan with sum assured of 1800000. please confirm this calculation are correct ? How can I trust this numbers ?

Deepesh I agree with you but insurance is not the one to be compared with returns products.

At the same time it is not possible to consistently invest in SIP after few years passed and if death occurs very difficult for the spouse and the kids to continue the same. Very risky at that point of time.

SIP gives great returns i Know but so much risk if died earlier then not possible to continue in that scenario only insurance helps.

Hi Priya,

Yes, mutual funds don’t provide life insurance. And that’s why I never compare MF with any insurance product.

I compare a mix of MF and term plan (or PPF and term plans) with any combo product.

To purchase life insurance, we don’t have to purchase a traditional plan.

One can purchase a term plan. Moreover, even term plans come in a few variants.

There are plans which, in addition to lumpsum payout, also provide income for a few years.

Hi all,

Term plan is best option

EPF/VPF/PPF is good option

Shares is best with high risk option

Mutual fund is medium return with medium risk.

LIC is marginal loss with assured amount.

Invest on land/house is best better good than any other with gaurantee..

“Don’t put your all eggs in one bucket”

@Deepesh, There is nothing wrong of investing in LIC policies. People should invest in SIP’s, LIC Policies and PPF because these will reduce their risk and cover them properly. if you invest in MF’s only and if it gets down there will nothing remains in your hands.

Hi Arjun,

Thanks for your inputs!!!

But Sir for any person who is not earning, Only endowment plan are the options like house wifes. Term assurance is only for the Earner with ITRs, salary slips and everything else to proof their worth. What plan you advise for House wife.

Hi Devesh,

First, you need to see if your wife needs life insurance?

Btw, there are joint term life insurance plans.

https://www.personalfinanceplan.in/all-you-need-to-know-about-joint-life-insurance-policies/

Hi Deepesh,

Thank you so much for your valuable information.

I really appreciate your efforts and your way to explain the difference between traditional endowment plan with e-term insurance and PPF and also we should not mix our investment and insurance schemes

You have got several negative feedback but I think this is the real truth which you tried to show the people but they were not ready to accept

I totally accept your thoughts and support your views on keeping investment and insurance separate.

I have shared this info with my friends and relatives and also explains them to invest in PPF or MFs for their investment purpose and purchase e- term insurance plans for their insurance purpose

This way you can create both your investment and insurance with good maturity amount

Thanks

Thanks Ayush for the kind words.

I don’t mind feedback (whether good or bad). I know some of the adverse feedback seems to have come from vested interests.

Please keep sharing and spreading the knowledge.

Hello Deepash-ji,

Many thanks for writing a wonderful blog to give us valuable information.

This is Vikas Bajaj, an NRI based in Japan.

Being graduated from Tokyo university, I also got in to trap of LIC, when I visited India in Jan 2017.

I have bought two policies and paying an annual premium of approx. 2 lac (approx.1 lac for each policy)

The policies are in force and unfortunately have paid 2 years of premium (approx. 4 lac in total)

The policies are as below;

Start date: Feb 2017 (next premium is to be paid by Feb 2019)

833 Jeevan Lakhhya (SA 20 lac, Term 25 years, premium paying 22 years)

836 Jeevan Anand (SA 20 lac, Term 25 years, premium paying 22 years)

If I surrender the policies now, I won’t get anything back as I have paid only for 2 years. It means I will have to suffer loss of 4 lac.

And if I pay 1 year of premium (approx. 2 lac more), I may have the policies paid up, but I am not sure what shall be the maturity amount as LIC doesn’t give future bonus (mention on the HP) on paid up value/ sum reduced.

Since bonus is not applicable, so total paid up value of the policy shall be 6 lac in total (both policies) and I would get 6 lac after 23 years from today, is this right?

Considering an alternative, if I have fixed deposit of 2 lac in any bank (rather than giving it to LIC), the value after 23 years will be approx. 9.5 lac (having return 7% p.a)

Please advise the following.

1. What shall be the approx. maturity value of the paid up policy?

If maturity value after paid up of policy shall be around 9 lac, I prefer to have the policy paid up after paying 1 year premium.

2. I prefer to have term insurance of SA 1.5 Cr with 40 lac coverage of critical insurance from ICICI Pru. Do you recommend this?

Vikas

vickyapu9@gmail.com

Hi Vikas,

You are welcome.

Though paid-up is an option, I am not a big fan of it.

So, either you surrender or keep making premium payments.

If premium payment is crowding out your other investments or is a big portion of your incremental investments, you must surrender.

Or else, you can continue and consider these plans as part of your debt portfolio.

As for calculations, you will get on maturity: Paid up Sum Assured (~6 lacs)+ bonuses account for the first 3 years. At 40 per 1,000 of Sum Assured, thee should be about 2.4 lacs. So, about 8-9 lacs you can expect at the time of maturity. If you ask me, not worth it. You are likely to lose track.

You can go with any term plan. All are same. ICICI Pru is fine too.

For critical illness, suggest you go through the following post.

https://www.personalfinanceplan.in/critical-illness-insurance-plan-should-you-buy/

First of all, many thanks for your reply & giving me time from your hectic schedule

I need to make correction in one of policy as below

836 Jeevan Anand (SA 20 lac, Term 25 years, premium paying 22 years)

↓

836 Jeevan Labh (SA 20 lac, Term 25 years, premium paying 16 years)

I have used LIC maturity calculater of Jeevan Labh (also confrimed with agent), it says I might get approx 54 lac (SA 20 lac, Bonus 25 lac, FAB 9 lac) at the time of maturity.

According to my calculation, the return shall be approx. 7.5% p.a which is not bad indeed if same amount is paid.

I am not really sure, if Bonus & FAB both are paid.

Lets says, if FAB is not paid, i would get only 45 lac and the rate of reutn shall be 6.5% p.a.

So my question to you is, please confirm if LIC pays bonus & FAB both?

and do you think above calculations are correct?

Hi Vikas,

You are welcome!!!

These policies are called participating policies for a reason.

They participate in profits of the insurance company. Now, the profits can keep fluctuating.

From what I have observed, reversionary bonuses are typically maintained.

FAB can take a big knock in bad times. So luck plays a big role.

As I see, for 16 year premium payment term, the bonus was Rs 43 per Rs 1000 Sum assured. That means 86000 per annum. Assuming this level of bonus is maintained, That is Rs 21.5 lacs of SA over 25 year. Quite far from Rs 25 lacs.

Perhaps, your agent used a bonus of Rs 50, which is not correct in my opinion.

FAB, as mentioned above, depends on your luck.

Many many thanks Deepash -ji

As per your calculation, the return would be approx. 6% p.a.

However, as per LIC official information (below link), the bonus rate for 2016-17 and 20-17-18 is mentioned as RS 50 for policy term 25years.

https://www.licindia.in/Customer-Services/Bonus-Information

Not sure if the same rate can be maintained by LIC over the next 23 years.

Hence the rate (Rs 43) mentioned by you seams good for better calculation.

Currently, I am having an investment in FD, mutual funds, post office scheme etc. and in addition will take cover from term insurance with critical illness cover,

Do u suggest I should opt FD from any good bank instead of paying to LIC?

Btw, no banks offer FD over 10y and rate of interest between 6 to 7% p.a.

Your advise shall be highly appreciated.

You are right, Vikas.

I picked up the wrong number. If the same level of bonus is maintained, your policy will accumulate Rs 25 lacs over 25 years *(assuming the level of bonus is maintained).

At your age, you must look beyond FDs and LIC policies too.

I know term plan beats anything in traditional plans with investment in PPF or FD or MF anything.

How is my idea about taking combination of Termplan with Labh?

Instead of investing in PPF along with term plan i will invest in Labh only so that i get risk coverage from term plan and labh and also 7.35% IRR (for 25/16 table in this).

I’m against all other traditional plans but only in 25/16 the IRR is 7.35% .

What is your opinion on this kind of combination?

Hi John,

I don’t see how Jeevan Labh will get you better returns than PPF.

So, purely from point of view of investments, PPF is a clear winner.

Please note, in case of Jeevan Labh, the returns will also depend on your entry age.

Hello sir,

If I am opting Jeevan labh for a SA of Rs 6,00,000, my premium(with accidental and disability rider) will be Rs 28,297(First year) and Rs 27,687(for the remaining 15 years) and the maturity amount will be Rs 16,20,000 (Rs 7,50,000+Rs 2,70,000).

Now if I consider ppf(8% interest), let’s say I invest that Rs 27,687 annually for 15 years, the amount comes to be Rs 8,11,901. In 16 years, it will be approximately Rs 8,66,028(by unitary method).

Now if I keep that amount in fixed deposit(6.75% interest) for the remaining 9 years, it amounts to Rs 15,81,847.

So, LIC is still yielding me more profit(albeit less liquidity). Where am I going wrong? Also, is taking accidental and disability rider recommended for extra premium of Rs 797 per year?

Kindly give a detailed analysis. Thanks a lot!

the Bonus rates have dropped to 48 per 1000 of SA in current day scenario for Jeevan Labh SA>5L & 25(16) but SRB’s once it is vested it wont change so in your case the 50 will be constant since it has already turned into a vested bonus once after vesting each year so you will be investing 4.43 lacs totally and your maturity will be around 16 lacs tax free.. considering inflation, you still will endup getting a lumpsum sizeable value for this product chosen its IRR will still prove handsome only 7.33%

PPF has limits. Doesn’t it?

what If my investment is much bigger or I already am investing 1.5 lakh/yr in PPF?

Yes, then PPF won’t be enough.

This is nice detailed post Deepesh. Thanks for sharing this. I wanted to check tax implication on the post maturity amount that we receive. A plan that guarantees me 50 L taxfree on maturity at a yield of 7 % after 25 years vs a MF investment that yields me 75L @10-11 % with taxes for the same duration.

Hi Rahul,

You are welcome.

The risk aspect in the two products is quite different. Hence, not really comparable.

Given what you shared. a 10%-11% pre-tax (and taxed at 10%) will be higher than 7% tax-free.

Hi Deepesh,

A small query, is deferred maturity payment allowed in LIC Jeevan Labh.

Hi Gaurav,

Not possible to defer but you can choose to receive maturity or death benefit in installments.

Deepesh,

First of all thanks for the detailed analysis. Is this applicable even for the Jeevan Labh (936) as well? This is because the PPF interest rates are now reduced to ~7% whereas you were calculating it at 8.1.%. Recently some LIC folks have sent me a mail with below information:

“”By investing only 10,000/- per month i.e. 1,20000/- P/A for 16 years, So your total investment towards the policy will be 18,84,075/- whereas at the completion of the term your total returns will be 65,62500/- with complete Tax free under section 80(c) and 10(10d).

You will get a fixed bonus of each 1000 on sum assured, 47/- will be added as a simple bonus and each 1000 on sum assured amount, 450/- will be added as final additional bonus. Where if you convert this bonus into interest: 7.33%-8% this is highest rate of interest at present in India when you compare with Normal fixed deposits, Postal RD, PPF and other guaranteed savings plans.””

Hi,

I need to know about good investment plans then

If someone puts a gun to my head and asks me to buy a LIC product only, then which is that best LIC product(other than term insurance plans), that I should go for ?

With all my biases, I would say Annuity plans (LIC Jeevan Shanti or LIC Jeevan Akshay) if you buy the right variant at the right age.

https://bit.ly/3kF6qHH

Very nice article. You save my money.

now coming to longterm equity or mutual fund investment, of course you will get higher returns if their is no bear market, on top of that who knows what % of tax will govt imposed for capital gains in future. So it look like return will be similar Jeevan Labh (tax free).We don’t what happens to market after 10 years…..even 5 years.sure one who holds their investment will be awarded after bear market, but the problem is tax.(one who is already in 30% current slab).