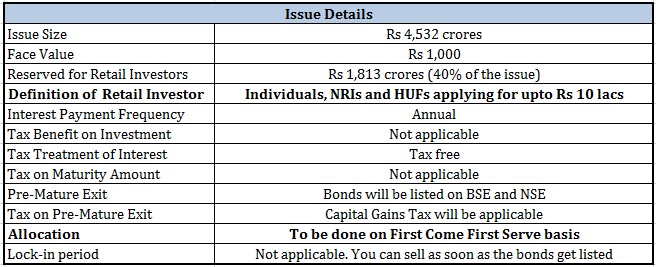

IRFC (Indian Railways Finance Corporation) tax-free bonds issue is out. The issue opens on December 8, 2015 and closes on December 21, 2015. The issue size is Rs 4,532 crores. In this post, I shall discuss the suitability of such tax-free bonds in your portfolio and who should invest in such bonds.

IRFC tax-free bonds issue is not the first tax-free bonds issue this year. NTPC, PFC and REC have already come up with tax-free bonds issue this year. However, IRFC bonds issue is much bigger at 4,532 crores. In fact, it is bigger than all the three issues combined. IRFC’s issue isn’t the last issue either. They are a few more lined up for this fiscal year, most prominent being NHAI (National Higher Authority of India)’s issuance (Rs 24,000 crores).

I have already covered most of the aspects in my earlier posts on tax-free bonds. Hence, in this post, I will mostly focus on the issue details. Rationale shall be same as in earlier posts.

To know more about tax-free bonds in general, especially taxation on sale of such bonds, please go through this post.

IRFC Tax-Free Bond Issue: Salient Features

Bonds will be issued on First Come First Serve (FCFS) basis. The bond will be available in three maturities i.e. Series I (10 years), Series 2 (15 years) and Series 3 (20 years). The issue size of Rs 4,532 crores is for all the series combined.

Interest payment frequency is Annual. Interest earned on these bonds is exempt from tax.

Interest Rate/ Coupon for IRFC Tax-free Bonds

It is easy to see that the investors in the highest tax bracket stand to benefit the most.

Long term Bank fixed deposits are offering 7.25-8.25% p.a. currently. On senior citizen fixed deposits, you can find rates up to 8.75% p.a. currently. Senior Citizens Savings Scheme (SCSS) interest rate as notified by the government for FY2016 is 9.3% p.a. These are pre-tax yields. Investors in the 10% tax bracket won’t really gain much by investing in these bonds.

An additional point to note is that investment in SCSS and 5-year tax saving FDs (not all FDs) comes with tax benefits under Section 80C too. There are no tax benefits on investment in tax-free bonds under IT Section 80C. Even investors falling in the higher tax brackets should consider this aspect, especially if you are not utilizing the complete limit of Rs 1.5 lacs under Section 80C.

For instance, if you invest in a 5-year tax saving FD that offers 8% per annum, the post-yield yield shall be 9.89% (10% tax bracket), 12.08% (20% tax bracket) and 14.68% (30% tax bracket).This is under the assumption you get tax benefit for investment in such FD under Section 80C. Though tax-free bonds and tax-saving FDs are not strictly comparable, I hope you get the idea.

However, investing in tax-free bonds while your 80C limit remains unutilized doesn’t make much sense.

Who qualifies as a Retail Investor?

A retail investor can invest up to a maximum of Rs 10 lacs (face value) in these bonds. If you hold these bonds worth more than face value of Rs 10 lacs (on the record date of payment of interest), you will not be classified as a retail investor and will get a lower coupon (7.07% instead of 7.32% for 10 year maturity).

Thus, you can get higher coupon rate if you hold no more than 1000 of these bonds. Please this is the aggregate number across all the series of this bond. Hence, to be classified as a retail investor, you cannot hold more than 1000 bonds across the three schemes. Your PAN will be used to aggregate your holdings and determine if you are a retail investor.

Can NRIs invest in IRFC tax-free bonds?

Yes, NRIs can invest in these bonds on both repatriation and non-repatriation basis. However, NRIs from US (US persons) cannot invest.

There is no need for NRIs to invest in these bonds. Interest on NRE fixed deposits is tax-free. You can argue that you will be able to lock-in these interest rates for the long term. It is not easy to predict interest rate cycles. Who knows you might get better rates when your NRE FDs mature.

Credit Rating/Credit Quality

CRISIL, ICRA and CARE have given AAA rating to long term borrowing programme of the company, which is the highest rating that can be given to any debt instrument.

The past performance of these credit rating agencies in rating corporate debt does not give me much comfort. However, since the IRFC is promoted by the Government of India, your money should be safe.

Exit before maturity (Liquidity Risk)

The bonds will be listed on Bombay Stock Exchange (BSE) and NSE (National Stock Exchange). However, given the size of the issue and low volumes in bond trading in India, the exit in the secondary market won’t be so easy.

Lower liquidity also leads to higher bid-ask spreads. So, if you are looking to exit in the secondary market, you might have to exit at a price lower than the intrinsic value.

Capital Gains

If you hold the bonds till maturity, there is no question of capital gains.

Bonds prices and interest rates move in opposite directions. When the interest rates go up, bond prices go down. On the other hand, when the interest rates go down, bond prices go up. So, if you expect interest rates to go down in the future, you can invest in these bonds for potential capital gains too.

However, do keep the liquidity risk in mind if you are betting on favourable interest rate movement.

Tax Benefits

Interest on these bonds is tax-free.

No tax benefit on the investment amount under Section 80C.

If you sell the bonds before one year, short term capital gains will be taxed at your marginal income tax rate (as per your income tax slab).

If you sell after one year, long term capital gains will be taxed at a flat 10.3% (including cess). Please note there is no indexation benefit available for listed bonds such as these, which is a negative for tax-free bonds. You can go through this post for comparison of tax treatment of tax-free bonds, debt mutual funds and fixed deposits.

Who should invest in IRFC Tax-Free Bonds?

Investors falling in the higher tax brackets and looking for regular income can look to invest in these tax-free bonds.

Investors in the 10% tax bracket should obviously not invest.

Only those who seek to hold the bonds till maturity should invest. Exit in the secondary market won’t be that easy or at a favourable price. Additionally, capital gains on tax-free bonds are taxed at flat 10%. There is no benefit of indexation. Debt mutual funds offer indexation benefits after 3 years.

For senior citizens or retirees, do explore other options such as SCSS or Senior Citizen Fixed deposits before deciding to invest. Do understand SCSS and 5-year fixed deposits come with 80C benefits while tax-free bonds don’t offer any tax benefits under 80C.

If you are not looking for regular income, don’t invest in these bonds. Firstly, you don’t get the benefit of compounding. Secondly, if you are willing to lock in your money for such long term, equity mutual funds can offer you better tax-adjusted returns. The returns under equity funds are not guaranteed but if you invest with discipline through SIPs, you should get better results.

The issue is on First Come First Serve basis. So, if you plan to apply, do it on the first day itself.