LIC has launched a new immediate annuity plan LIC Jeevan Akshay VII (Plan 857).

Moreover, the immediate annuity variants of LIC Jeevan Shanti (Plan 850) have been withdrawn. Thus, LIC Jeevan Shanti becomes a pure deferred annuity product.

In this post, let us find out about LIC Jeevan Akshay VII in detail.

While I have covered the basics of an annuity plan in another post, I will touch upon these aspects briefly in this post.

What is an Annuity plan?

Along with bank fixed deposits, an annuity plan must be one of the simplest financial products.

You give a lumpsum amount to the insurance company. And the insurance guarantees you an income stream for life.

That’s it.

Let’s say you buy an annuity plan for Rs 10 lacs and the prevailing annuity rate is 6% p.a.

In such a case, the insurance company will pay you Rs 60,000 per annum (or Rs 5,000 per month) for life. It does not matter what happens to the interest rates subsequently. You have locked in the rate of 6% for life.

The insurance company pays you Rs 60,000 per annum as long as you are alive.

The payment stops when the investor dies.

Depending upon the variant chosen, the insurer may give back the purchase amount to the family on investor demise.

Now, we have this penchant for complicating things. And investors have different needs too. Hence, annuity plans come in multiple variants. If you must buy an annuity plan, you must navigate through all the options and choose the right one for you. Usually, the simplest option is the best.

Note that the annuity rate (or the interest rate) depends on the investor age and annuity variant chosen.

You can expect Annuity rates to increase with investor age at the time of entry.

Many investors buy annuity products to ensure an income stream during retirement. Or an income stream to replace salary that stops during retirement.

Immediate Annuity and Deferred Annuity Plan

I use pension payment, annuity payments, or payments interchangeably in this section.

With an immediate annuity product, the annuity payment starts immediately i.e. from the next month or the next year.

With a deferred annuity product, you defer the annuity payments for a few years and the payments start at the end of the deferment period.

For instance, you are 50 years old. You buy an immediate annuity plan. The annuity payment will start from the next month or the next year (depending on the frequency option chosen).

In case of a deferred annuity product, you can defer the payments for say 10 years (to coincide with retirement). Hence, the payments will start only after 10 years.

By the way, in both cases, you lock-in the annuity rate at the time of purchase.

LIC Jeevan Shanti had both immediate annuity and deferred annuity variants. The immediate annuity variants have now been withdrawn (effective August 25, 2020). LIC Jeevan Shanti now becomes a deferred annuity product.

LIC Jeevan Akshay VII is an immediate annuity product. It has no deferred annuity variant.

Hence, if you are planning an annuity plan from LIC

Immediate Annuity: Buy LIC Jeevan Akshay VII

Deferred Annuity: Buy LIC Jeevan Shanti

LIC Jeevan Akshay (Plan 857): Salient Features

- Immediate Annuity product

- Minimum Investment: Rs 1 lac

- Maximum Investment: No limit

- Minimum Entry Age: 30 years

- Maximum Entry Age: 85 years (100 years for Variant F)

- Premium Payment Frequency: Single Premium Payment (pay the premium just once)

- Annuity payment frequency option: Monthly, Quarterly, Half-yearly, Annual

- Tax Benefit on Investment: Up to Rs. 1.5 lacs under Section 80CCC (within the overall limit of Section 80C)

- Annuity Payments taxable at your marginal income tax rate

- Loan Facility: Available with only Return of Purchase price variants (Variants F and J)

- Surrender: Option to surrender available only under variant F and J

- NPS subscribers exiting NPS can purchase LIC Jeevan Akshay VII.

- Rebate for online purchase i.e. for the same purchase amount, you will get a higher pension if you purchase online (compared to offline purchase)

- Higher pension for higher purchase amount too.

- GST at 1.8% is applicable on the purchase price. Hence, if the purchase price is Rs 10 lacs (annuity calculated based on purchase price), you will have to pay Rs 10.18 lacs.

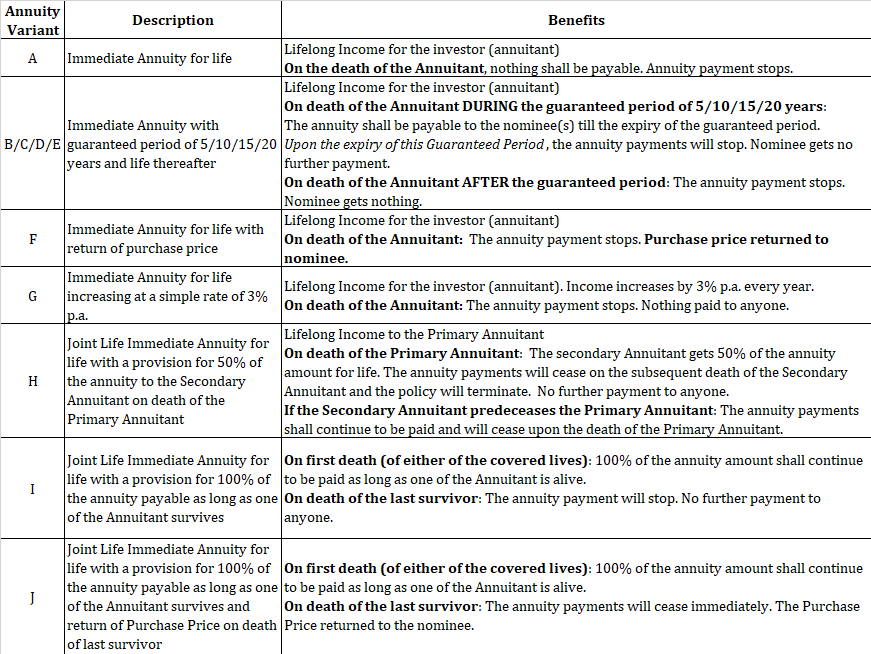

LIC Jeevan Akshay (Plan 857): Variants

LIC Jeevan Akshay comes in 10 variants.

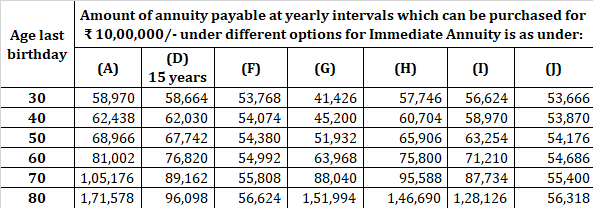

LIC Jeevan Akshay VII: Annuity Rates

I reproduce the sample rates from LIC website.

LIC Jeevan Akshay VII: How to Buy?

You can buy through your agent or you can buy online from the LIC website. As mentioned earlier, you get rebate for purchasing the policy online.

Let us say your annuity payment is Rs 6,000 per month for offline purchase. If the rebate is 2%, you will get Rs 6,120 per month for online purchase.

You can go to LIC website, locate “Buy Policy Online” and follow steps.

Before you buy LIC Jeevan Akshay VII (or any other annuity plan)

An annuity plan is perhaps the only investment product that I like from insurance companies. Yes, there are merits and demerits of every product. However, there can be a gap (or risk) in your financial planning that only an annuity plan can fill.

At the same time, not everybody must purchase an annuity plan. Product suitability is important.

You must purchase the RIGHT variant at the RIGHT age.

You can also use annuity strategies to increase income and reduce risk.

Suggest you go through the following two posts.

Retirement Planning: When to Buy an Annuity Plan?

Retirement Planning: How Staggering Annuity Purchases can help increase income and reduce risk?

I trust your judgement.

31 thoughts on “LIC Jeevan Akshay VII (857): Review: New Immediate Plan from LIC”

Brilliant content; keep posting.

Good analysis.

Thanks

10 lacs deposit on LIC Jeevan Akshay VII how much pension came on monthly

Depends on your age. You can check the rates on LIC website.

Love your website. Thank you for doing such a good job

Very good and clear content. Thanks a lot. Keep posting.

Thanks!

I did not understand what is Variant F? (Maximum entry age 100 years)

Kindly explain

Under variant F, the investor gets an annuity for life.

After the investor’s demise, the purchase price (investment amount) is returned to the nominee.

I wish to add: In a deferred income plan, with a one time purchase, the purchase corpus is enhanced by accumulation of a tax-free compound interest till the payout commences. This shelters you in the interim period from levy of tax at a high rate if you are a salaried employee in the maximum tax range. When your annuity starts you will have retired and you may fall in the lower tax bracket. Thus you can derive the benefit of tax planning through such a plan.

That’s a valid point. Thanks for sharing.

a candidate age 43 years and deposit 1,00,000 then 60 years age how amount collect per month ??

It is an immediate annuity plan. The pension will start right away.

Kudos Deepesh, your post are insightful.

My query is related to option H and option I.

When we say joint life, should it be compulsorily spouse or it can be any close relative.

Pls clarify.

Thanks Ilango!

The Joint life annuity plan can be taken between two lineal ascendants/descendants of a family (Grandparent, parent, children, grandchildren) or spouse or siblings.

Thankyou Deepesh for your quick clarification.

Does this mean , if a 80 year old grandfather takes the policy by investing 10 lacs with his loving grand daughter as joint annuitant ,who is 30 years old.

As per option I, the grand daughter will receive Rs.128,126/ year as annuity for next 40 years as joint annuitant ( Female life expectancy statistically 70 years) , which is like 12.7% assured for next 40 years.

Excuse me if my doubt is dumb and I have erred some where in the understanding of the basics.

Thats a good question. Deepesh Ji plz answer.

If its correct, then many young people will use this trick.

They can take option “I” with aged grandparent as joint annuitant, and take advantage of the high interest rate of their high age. Once the grandparent ceases, the grand son/daughter will continue getting the high interest rate based on the given condition.

Or the grand daughter will get interest based on his/her own age ? Will be interesting to know.

Hi Mrinmoy,

The annuity income will depend on the age of the second member too.

Sir can s policy holder terminate new Jeevan Akshay policy in free look period even the LIC deposit the annuity in policy holders a count without sending the policy bond to study and desire the terms and conditions plz let me know sir

Hi Ilango,

The illustration is confusing (you can also call it misleading). My bad. I should have clarified.

The annuity income will depend on the age of the second member too.

The sample rates ( on LIC website) do not specify what they have considered for the age of the second member.

They would have considered the age of the second member to be high too.

Thankyou Deepesh for the clarification.

I will get in touch with a LIC agent and try to get additional info based on actual age of annuitants.

Superb Post

Thanks Mrinmoy!

CAN U PLEASE SEND CIRCULAR OF LIC IN WHICH OPTION J IS REMOVED IN JEEVEN AKSHYA VII ?

Dear Mr. Tripathi,

Not sure I got your query right.

LIC Jeevan Akshay VII has option J.

You can get more info about the product on LIC website (https://licindia.in/Products/Pension-Plans)

My age is now 63 and my wife is 56. I will invest 2 lakhs. Would you please help what will be annuity corpus under Option I and Option J.

Sir, there a option to top up the premium amount or should we buy a second policy. Ex: 1 opt for Option F & buy the policy for 3 lakhs & after couple of months can I add another 7 lakhs to the same policy?

Hi Manjunath,

You will have to buy a new policy.

How do i get refund of GST on policy bought?

Sir,

I am 69. I want to invest Rs. 10,00,000/- in LIC Policy No.857. I prefer option F. How much amount shall I receive monthly as pension ? Kindly enlighten me in this regard.

Thank you.

Amar Nath Dutta

In option D will the annuitant get the annuity income even after the gauranteed period of 15 years . If yes then how much