Long-Term Capital Gains on sale on equity mutual funds and listed shares was proposed in Budget 2018. I have discussed the proposal in an earlier post.

In this post, let’s look at the actual impact (in numbers) because of the introduction of tax on long-term capital gains.

LTCG on sale of equity shares/equity mutual funds

From FY2019, the long-term capital gains (holding period > 1 year) on the sale of listed shares and equity mutual fund units will be taxed at 10%.

Initial Rs 1 lac of LTCG shall be exempt from tax.

You can read more about the tax proposal in this post.

How will tax on LTCG on the sale of equity shares/equity mutual funds affect your returns?

This is best understood with the help of an example.

Let’s assume you invest Rs 1 lac today.

I don’t know how much return you will earn over the next 5, 10 or 20 years.

Therefore, I will assume varying levels of returns and consider multiple investment horizons.

Since there is a tax exemption on LTCG (on sale of equity) of Rs 1 lac per financial year, I have reduced the LTCG in the year of sale by Rs 1 lac to calculate tax liability.

I have calculated the returns for different levels of return and different investment horizon. Of course, you don’t know the return will earn when you invest. However, you should still be able to assess the impact of taxation on your net returns.

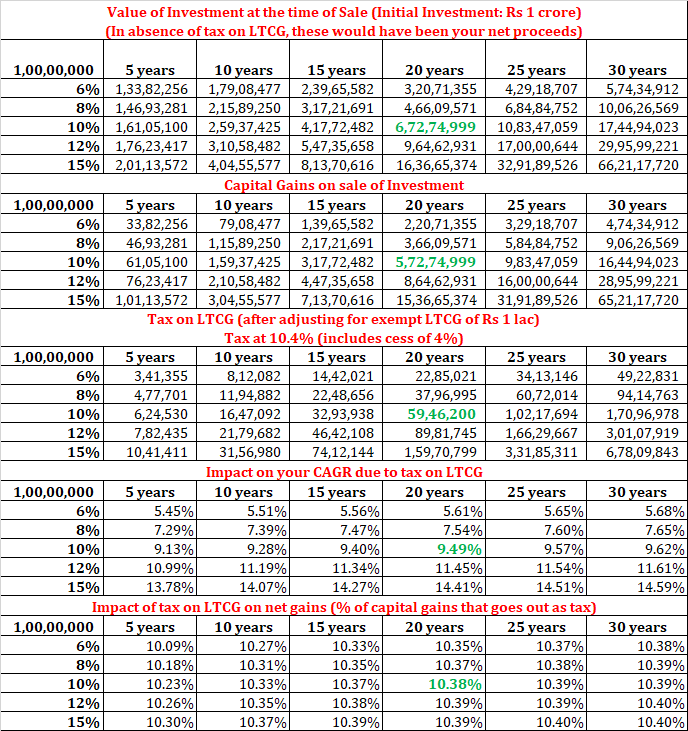

If you invest Rs 1 lacs and redeem the investment after 20 years and happen to earn a pre-tax return of 10% p.a., your sale proceeds will be equal to Rs 6.72 lacs.

Your total capital gain is Rs 5.72 lacs. Out of this, Rs 1 lac is exempt. Therefore, you have to pay LTCG tax of 10.4% (including cess) on the taxable gain of Rs 4.72 lacs.

Your LTCG tax liability will be Rs 49,166.

After accounting for tax, your net proceeds is Rs 6.23 lacs.

In 20 years, your money has grown from Rs 1 lacs to Rs 6.23 lacs.

That is post-tax return of 9.58% p.a.

Due to LTCG tax, your pre-tax return of 10% p.a. has gone down to 9.58% p.a.

Moreover, you can see in the above table that the impact in terms of the difference between pre-tax and post-tax return depends on the investment horizon and the rate of return.

Additionally, the impact of LTCG exemption of Rs 1 lac will go down as the investment amount gets bigger.

Let’s do the same calculation with an initial investment of Rs 1 crore.

As you can see, the post-tax return in the same example (20 years, 10% p.a.) goes down to 9.49% p.a. (post-tax return for an initial investment of Rs 1 lac was 9.58% p.a.).

This demonstrates that the net impact of LTCG exemption of Rs 1 lac per financial year goes down as your portfolio gets bigger.

In terms of absolute amount, the tax hit is Rs 59.46 lacs (on the total capital gain before taxes on Rs 6.72 crores). Clearly, not a small amount.

Fall from 10% p.a. to 9.49% p.a. may not look like much. However, when we talk about many years of compounding, the impact is going to be sizeable.

I have read accounts where many experts have mentioned that the impact is going to be minimal. That’s clearly not the case. Most of us shifted from regular to direct to save this extra 0.5-1% p.a. of the expense ratio. Didn’t we?

Therefore, let’s not fool ourselves. There is going to be an impact of LTCG taxation. Let’s accept it and pay the taxes happily.

I always believed that equity investors were getting extremely preferential tax treatment by the Government. Such long-term gains had to start getting tax sooner or later. In my opinion, it is a step in the right direction. However, there is a hit to the investors.

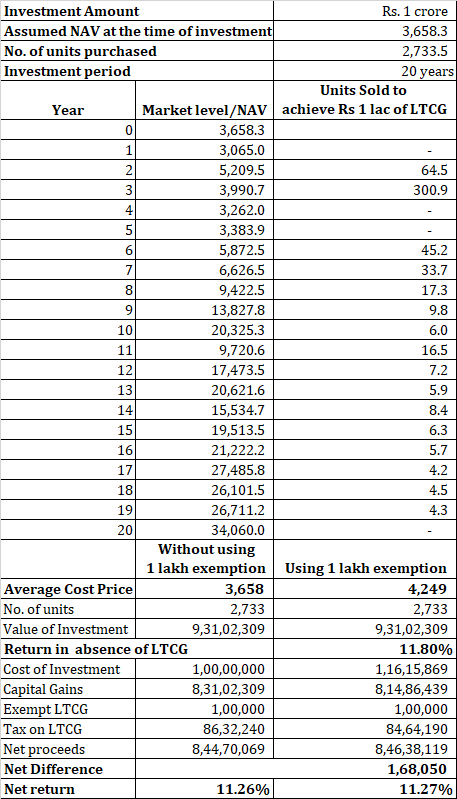

What about the impact of utilizing Rs 1 lacs exemption on LTCG every year?

In my above example, I have taken the benefit of LTCG taxation of Rs 1 lac per year only in the final year. However, I could have taken this every year.

Essentially, you sell MF units one day and buy those back at the same price (assumption) booking long-term gains to the extent of Rs 1 lac per year.

Suppose you invest Rs 10 lacs (10,000 units at NAV of Rs 100). After1 year, the amount becomes 11.5 lacs (NAV is 115). So, you sell 6666 units worth Rs 7.66 lacs resulting in a net gain of Rs 1 lac.

Then, you use the amount to purchase the units in the fund again. Therefore, the number of units remains the same.

After churning once, you have 6666.67 units at cost price of Rs 115 and 3333.33 units at cost price of Rs 100. The average cost price is Rs 110. Had you not sold and booked profits, your average cost price would have still been Rs 100.

Therefore, by booking gain of Rs 1 lac, you have been able to increase your average cost price. This will effectively reduce your tax liability whenever you finally sell the units.

As I see, by doing this, you can increase your corpus by a maximum of Rs 10,000 per annum. Of course, this amount gets invested and earns your return.

Well, even though such analysis can be done, it requires another set of assumptions to be made.

For instance, I need to assume asset price (Fund NAV) at periodic intervals. Why?

Because I need to sell to book profits. And for that, I need the price of the asset (NAV). For all you know, during bad times, you may not even have gains to book. If there is no gain, you can’t take benefit of Rs 1 lac exemption for that year. By the way, in that case, you can book losses and carry forward the losses to be set off in the future years. However, since your average cost price will also be reset downwards by booking loss, there may not be any impact.

In any case, you can see it can get quite complicated.

For the analysis, I have considered calendar year Sensex data from 1998 till 2018 (Jan 1) and try to assess the impact on return.

I have considered an initial investment of Rs 1 crore to have a very high number of units. This ensures that, for the all 20 years, I have units (acquired at the base price) to sell and repurchase at the prevailing price.

Please understand unit redemption works on FIFO basis and the oldest units get sold first. A lesser number of units would have complicated the analysis. Not really needed to present my point.

As you can see, for a big portfolio, churning the portfolio may not really make much of a difference. Net tax saving (for the data used) is about 1.68 lacs (when the ending corpus is 9.31 crores).

If you had simply stayed put for 20 years, you would have earned a return of 11.26% p.a.

By continuously churning for 20 years to get the benefit of Rs 1 lacs LTCG exemption, you would have earned 11.27% p.a.

A difference of 0.01% p.a.

Having said that, with good technology, implementing this portfolio tweak wouldn’t take more than 5 minutes. Therefore, it may not really be a bad idea to utilize this benefit. I assume these regular tweaks won’t play around with your investment discipline.

Do note, for a smaller portfolio, the difference in returns could have been a bit bigger.

What about the impact on SIP?

A similar analysis can be extended to impact on Systematic Investment plans too.

However, since the amount involved is small, the units will get churned on a regular basis making the analysis slightly complicated (for my excel skills).

I will consider the impact on SIPs in another post.