In this post, I will focus on certain aspects of capital gains taxation for non-resident Indians (NRIs). Even though the rate of capital gains tax is same for residents and non-residents, there are a few differences that affect taxation for NRIs.

- Tax exemption limit for NRIs is Rs 2.5 lacs irrespective of age.

- In case of Resident Indians, the tax exemption limit is Rs 2.5 lacs (< 60 years), Rs 3 lacs (>=60 and < 80) and Rs 5 lacs (>=80)

- Interest income on NRO account is taxed at marginal income tax rate.

- Interest income of NRE or FCNR accounts is exempt from income tax in India.

- Capital gains tax rate for NRIs is same as that for residents.

- Short term capital gains (holding period<=1 year) on the sale of equity/equity funds are taxed at flat 15%.

Long term capital gains (holding period > 1 year) on sale of equity/equity funds are exempt from tax.Long term capital gains on the sale of equity/equity funds (in excess of Rs 1 lac per financial year) will be subject to a tax of 10%. This was introduced in Budget 2018.- The aforesaid capital gains tax on equity/equity funds applies to only those units on which Securities Transaction Tax (STT) has been paid (under Section 111A).

- Short term capital gains (holding period <= 3 years) on the sale of debt mutual funds/gold/real estate etc are taxed at your marginal income tax rate (as per income tax slab). For real estate, the holding period for the capital gains on sale of property to qualify as LTCG has been reduced to 2 years (introduced in Budget 2017).

- Long term capital gains (holding period > 3 years) on the sale of debt mutual funds/gold/property etc are taxed at 20% after indexation. There are a few assets such as listed bonds or tax-free bonds where long term capital gains are taxed at flat 10% (without the benefit of indexation). Go through this post for more on long term capital gains tax.

Set off of Capital Gains against the Basic Tax Exemption limit

The treatment depends on the type of capital gain.

1. Short-Term Capital Gains on sale of equity/equity mutual funds

Set off against the basic tax exemption limit is NOT available to NRIs for short-term capital gains of equity shares/equity mutual funds (defined under Section 111A).

For instance, if you (NRI) made short term capital gains of Rs 4 lacs on the sale of equity shares and have other income of Rs 75,000 in India, you will still have to pay tax at 15% on gain of Rs 4 lacs. Hence, your tax liability will be Rs 60,000 (before surcharge and cess).

In case of a resident, he/she will get the benefit of adjusting short term capital gains against shortfall in income from the basic tax exemption limit.

Example: A resident Indian makes short term capital gain (STCG) of Rs 4 lacs on sale of equity funds units and other income of Rs 75,000 in a financial year, he/she will have to pay capital gains on only Rs 2.25 lacs. His total income (excluding STCG on equity funds) is only Rs 75,000. Since there is shortfall of Rs 1.75 lacs from basic tax exemption limit, this shortfall can be adjusted against short term capital gains on redemption of equity fund units. Total tax liability will be Rs 33,750 (15% of Rs 2.25 lacs).

Read: How can NRIs invest in Mutual Funds in India?

2. Long Term Capital Gains on sale of equity/equity mutual funds

Long term capital gains on sale/redemption of equity shares/equity mutual funds are exempt from tax. Hence, there is nothing to worry about.

LTCG in excess of Rs 1 lac per financial year is taxed at 10%. To understand the impact of LTCG on equity returns, go through this post.

Residents can set-off LTCG against basic tax exemption limit but non-resident can’t.

3. Short Term Capital Gains on the sale of Debt/Gold/Real Estate etc

Set off against basic tax exemption limit (Rs 2.5 lacs) long term capital gains of any capital asset (other than equity) is permitted for both resident and non-residents.

You can adjust such short-term capital gains against basic tax exemption limit.

For instance, you have short term capital gains on the sale of debt funds/property to the extent of Rs 4 lacs and other income of Rs 75,000. Total income for the year is Rs 4.75 lacs (including capital gains). The entire income will be taxed as per income tax slab. You will have to pay tax of Rs 22,500 (irrespective of residential status).

4. Long Term Capital Gains on sale of Debt/Gold/Estate etc

This treatment is similar as in case of Short Term Capital Gains Tax on equity/equity fund units. Residents can set off LTCG against basic tax exemption limit while non-resident can’t.

Rate of taxation is 20% after indexation or 10% without indexation depending upon the type of asset.

Deduction for investment under Chapter VI-A (Section 80C to 80U)

There is no difference in treatment for residents and non-residents.

You can claim deduction for such investments only against Short Term Capital Gains (STCG) on non-equity investments.

For capital gains for investments defined under Section 111A (capital gains in equity/ equity funds) and Section 112 (long term capital on other assets), you cannot reduce the amount of capital gains by investment/expenses in life insurance, PPF, ELSS, health insurance premium etc.

Essentially, you CANNOT reduce your capital gains by investments/expenses made under Section 80C to Section 80U. The only exception is STCG on non-equity investments.

There is no relief under Section 80C to Section 80U when it comes to LTCG on sale of non-equity investments (debt/gold/property etc) and capital gains on equity investments.

Example 1

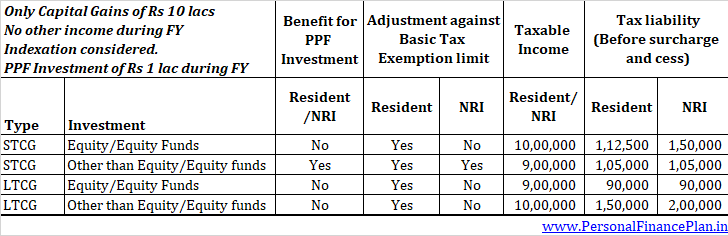

You made short term capital gains of Rs 10 lacs on sale of debt mutual funds/gold/property. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You can take benefit for investment in PPF for short term gains on equity investments. Hence, total taxable income will become Rs 9 lacs.

First Rs 2.5 lacs is exempt (for both residents and non-residents). You pay 10% for income up to Rs 5 lacs and 20% on income above Rs 5 lacs (till Rs 10 lacs).

Total tax liability will be Rs 25,000 + Rs 80,000 = Rs 105,000.

Example 2

You made SHORT term capital gains (STCG) of Rs 10 lacs on sale of equity mutual fund units. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF. Hence, total taxable income will become Rs 10 lacs.

Residents can adjust short term capital gains on equity MF units against basic tax exemption limit. You will pay a flat 15% of such short capital gains (over Rs 2.5 lacs).

Total tax liability (for residents) will be Rs 1.125 lacs (15% of Rs 7.5 lacs)

Non-Residents cannot adjust short-term capital gains on equity MF units against basic tax exemption limit. You will have to pay 15% on the entire Rs 10 lacs towards capital gains tax i.e. Rs 1.5 lacs (before cess and surcharge).

Example 3

You made LONG term capital gains (LTCG) of Rs 10 lacs on the sale of equity mutual fund units. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF for long term capital gains.

However, since long-term capital gains on equity funds are exempt from tax, there will no capital gains tax liability.

Since the first Rs. 1 lac is exempt per financial year, you will have to pay tax at 10% on the remaining Rs 9 lacs.

Therefore, your total tax liability will be Rs 90,000 (Rs 9 lacs X 10%).

Example 4

You made LONG term capital gains (LTCG) of Rs 10 lacs on sale of DEBT mutual fund units. The capital gains amount is after accounting for indexation. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF for long-term capital gains.

Hence, the taxable income will stay at Rs 10 lacs.

If you are a resident, you can set off such gains against the shortfall in basic tax exemption limit. You will have to pay tax at 20% on Rs 7.5 lacs.

If you are a non-resident, you CAN NOT set off such gains against the shortfall in basic tax exemption limit. You will have to pay tax at 20% on Rs 10 lacs. Capital gains tax for NRIs in this case will Rs 2 lacs.

Must Read: Income Tax and TDS Rates for NRIs

Investments in Foreign Currency

If you have purchased shares or debentures of an Indian company in foreign currency, rupee depreciation may affect your returns.

It is quite possible that you may have made gains in rupee terms but made losses in foreign currency terms. Is there a relief?

Suppose you invest 1,000 USD (Rs 70,000) in equity shares of a company at Rs 70/USD. You exit investment at value of Rs 90,000 making rupee gain of Rs 20,000. During the interim, let’s suppose the USD has moved from Rs 70 to Rs 1,00 (rupee depreciation). So, in USD terms, the value of your investment is USD 900 only. Hence, you are incurring a loss of USD 100.

For such cases, there is relief under Section 48. Your capital gain/loss will be calculated in foreign currency and reconverted into Indian Rupees for finding out capital gains.

In the aforesaid example, you will incur a capital loss of Rs 10,000 (100USD X Rs 100/USD) and not a capital gain of Rs 20,000.

Do note the relief is only for shares and debentures of an Indian company (and not for any other capital asset).

An additional point to note is that this provision can be a double-edged sword. Your gains will get enhanced in case of rupee appreciation.

Set off/Carry Forward of Capital Losses

The rules are same for both residents and non-residents.

- You CAN NOT set off income from any other head (Salary/House Property/Business/Other sources) against Short term or long term capital loss (STCL or LTCL). Only income from capital gains can be set off against STCL or LTCL.

- Short term capital losses (STCL) can be set off against both long term and short term capital gains (STCG and LTCG).

- On the other hand, Long term capital losses can be set off against only Long term capital gains (and not short-term gains).

- For capital assets where long term gains are exempt from tax, no set off against long term capital losses in such assets shall be allowed.

For instance,long termcapital losses in equity mutual funds cannot be used to set off any capital gain. This is because long-term capital gains onsaleof equity funds are exempt from tax. - In the event you do not have enough capital gains to set off against capital losses, you can carry forward the losses for the next eight years. Such losses, therefore, can be used to set off capital gains in the next 8 years.

- Both long-term and short-term capital losses can be carried forward for 8 years.

- To carry forward capital loss, you must file the return before the due date.

For more on this set-off of losses, suggest you go through the following post.

How to save Long Term Capital Gains Tax?

There are provisions under Income Tax Act that allows investors to avoid paying tax on long term capital gains. The relief is provided under Section 54, Section 54EC and Section 54F of the Income Tax Act.

Quite expectedly, the relief comes with multiple conditions. I have a detailed post on this topic. You can go through this post to find out more on this topic.

Do note the relief is available for only long-term capital gains. No such relief is permitted for short-term capital gains.

Read: How to save tax on Capital Gains from the sale of house?

Special Provisions for NRIs

In addition to general provisions mentioned above, NRI get the benefit of special provisions under Section 115-C to Section 115-I for specified assets purchased in foreign exchange.

Specified assets include shares/debentures in an Indian company, deposits with an Indian Company or securities issued by Central Government.

For a financial year, you can choose whether you want to be governed by general provisions or specific provisions (Chapter XIIA). It is entirely your choice.

If you choose to governed by Special provisions for a particular year,

- Your investment income and long term capital gains on assets (other than specified assets) are taxed at flat 20%.

- Long term gains on specified assets are taxed at 10%.

- There is no benefit of indexation.

- There is no adjustment against basic tax exemption limit and deduction for investment/expenses under Chapter VI-A (Section 80C to 80U).

Capital gains tax regime (under general provisions) is already quite benign. Hence, specific provisions may be useful only in select cases.

Points to Note

- Your income tax liability may not be over by paying capital gains tax in India. You may have to pay additional tax in your country of residence.

- You may get credit for taxes paid in India.

- For NRIs, TDS is deducted at the maximum possible rate for the transaction. For more on NRIs and TDS rates, go through this post. If excess tax has been deducted, you can claim it back at the time of filing income tax return.

Disclaimer

This is a very simplistic representation of the Income Tax laws. There are many conditions which may completely alter taxation in specific cases. Covering such conditions is beyond the scope of this post. Moreover, I am not a tax expert. You are advised not to make decisions solely on the basis of this post. You are advised to consult a Chartered Accountant or a tax consultant before making any decision.