If you are an NRI, you may be able to get a loan at a very low rate of interest in your country of residence?

If you have such an option, you may feel tempted to take a low cost loan and invest in India. For instance, let’s say you can borrow at 3% p.a. abroad and invest in India in NRE fixed deposits at 7.5% p.a. Looks a very good deal, isn’t it?

Alternatively, if you have to take a loan in India, you could instead borrow abroad and send that money to India? Taking loan abroad at 3% instead of taking a loan at 10% in India.

Well, there is nothing wrong with investing in India. You may want to a in India for the lack of investment opportunities in your local country or your general comfort with investments in India. Similarly, there is nothing wrong in trying to lower your cost of funds. However, there are a few things that you must keep in mind.

Here are 5 things you must keep in mind when you are taking a loan abroad for making an investment in India or for replacing a loan that you would have taken in India.

#1 Flat Rate vs Reducing Balance Loan

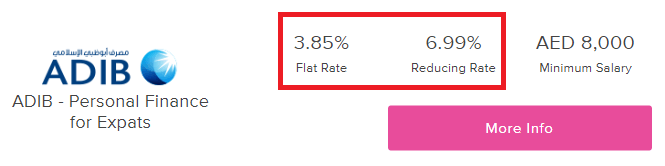

The cost of your loan may not be as low as you think it is. Here is a snapshot from a loan comparison website in Middle East.

You can see the two rates of interest for the same loan. 3.85% flat rate and 6.99% reducing balance rate.

What is the difference?

Under a flat rate loan, interest for each EMI installment is calculated on the original loan amount (and not the outstanding amount as under reducing balance loan). Therefore, principal repaid and interest paid remains constant for all the EMI installments.

Under a reducing balance home loan (like your home loan), interest is calculated on the principal outstanding. Therefore, the interest component of EMI is quite high in the initial years but goes down with time. Refer to this post to see how EMI calculations work under the two methods.

Let’s understand with an example.

You take the flat rate loan Rs 12 lacs (rupee equivalent) at 3.85% p.a. for 5 years.

Principal component = Rs 12 lacs/ 60 months = Rs 20,000

Interest Component= Rs 12 lacs*3.85%/12 = Rs 3,850

EMI per month = Rs 20,000 + Rs 3,850 = Rs 23,850

You have to pay an EMI of Rs 23,850 for 60 months to repay a loan of Rs 12 lacs. If you had received a reducing balance loan at 3.85% p.a. for 5 years, the EMI would have been Rs 22,018.

Is the real cost of flat rate loan only 3.85% p.a.? Clearly, no. You are paying a much higher rate of interest than you think. You can figure out the real cost for this loan by using XIRR function. The comparable cost of the loan (under reducing balance loan) is 7.12% p.a.

This means, under a reducing balance loan, the EMI for a loan of Rs 12 lacs for 60 months at 7.12% p.a. would have Rs 23,850 (the same as for flat rate loan at3.85% p.a.).

To put it another way, if the cost of loan was indeed 3.85% p.a., you could have got a loan of 12.99 lacs at an EMI of Rs 23,850 for 5 years.

If you have taken a loan abroad as a replacement for a rupee loan in India, do compare the right numbers. You borrow abroad instead of borrowing in India because the interest rate is lower abroad. However, you must compare the right rates. Now, you know that the right number to compare in the above example is 7.12% p.a. (and 3.85%).

If you have taken a loan to invest in India, you must ensure that the return from the investment is more than 7.12% p.a. By the way, I have not considered the risk of rupee depreciation yet.

#2 Do not ignore the potential impact due to Rupee Depreciation

This is more of a problem if you take a loan abroad to invest in India.

You may feel that you can earn risk-free returns by borrowing in a foreign currency at a low rate of interest and investing in India at a higher rate of interest (or potentially higher returns). It is not that simple. What about Rupee Depreciation? Rupee may depreciate in the interim and can affect your net returnsin foreign currency.

Depreciation poses an even bigger risk if you plan to use the returns generated from Indian investment to repay the loan. The USD-INR exchange rate was 63 a few months back. Now, it hovers around 71. If you brought money in at 63 and have to convert back at 71, you will have to take a hit. Even if you made 12% on this rupee investment post-tax in 1 year, your net return in USD terms is about NIL. Moreover, since the loan carries some rate of interest, you have made a loss of this entire transaction.

Appreciate the currency risk involved.

By the way, if you are taking a loan abroad to invest in a volatile asset in India such as stocks and mutual funds (and plan to repay from returns generated), you are taking a much bigger risk (Rupee depreciation may be a lesser concern). I would advise you to stay away from such high-risk deals. However, this is a not a topic of this post.

Many investors borrow abroad, convert the foreign currency funds to Indian Rupee and use the proceeds to make a purchase or invest in India. However, instead of relying on returns from Indian investments thus made, they rely on local funds(their salary abroad) for loan repayment. This is a smarter approach in my opinion.

Firstly, since they are clear that the loan has to be repaid from income abroad (and not through returns from Indian investments), there are lesser chances of over-borrowing.

Secondly, even though rupee depreciation can still mess up your net returns in foreign currency, it will not mess up your loan repayment at least.

I understand many NRI investors also invest in India because they eventually plan to come back to India after a few years. Such investors may argue that rupee depreciation may not affect them as badly. Fair enough but it is an issue nonetheless.

#3 There is processing fee and other ancillary charges

Interest cost is not the only cost that you incur. Charges such as processing fee also add to the overall cost of your post. Shorter the loan tenure, greater the impact of processing fee or other fixed one-time charges. Assess the all-in cost.

#4 There is currency conversion cost too

You incur cost in converting currency. The bank or the exchange house will make money on the transaction by offering an exchange rate which is slightly inferior to the market rate. That adds to the overall cost of the transaction and the loan.

If you have to repatriate money abroad after some time, you will have to incur the cost again.

You may argue, there will be conversion costs either way.

- Borrow abroad and convert to India. Or

- Borrow in India and send money from abroad for loan repayments (unless you have cashflows in India to service the loan).

I agree but you must appreciate the costs involved especially when you are borrowing abroad to invest in India (and not to replace a loan in India).

#5 You may lose out on tax benefits

This is important if you are borrowing to replace a loan in India.

Repayment of education loan (80E for interest payment) or home loan (Section 80C and Section24) qualifies you for tax benefits in India. You will not get tax benefits in India under Section 80C and Section 80E if you have taken the loan abroad.