If you are an NRI and are returning to India permanently, you need to convert your non-resident accounts (NRO, NRE) to resident accounts. You should be allowed to continue your NRE FDs as resident FDs at contracted rate till maturity. However, when you visit the bank branch to change your residential status, you are in for a surprise.

What Banks typically force returning NRIs to do?

NRE account holders face major issues when they try to re-designate their NRE fixed deposits to resident deposits. Banks typically ask the customers to break their NRE FDs and re-open resident fixed deposits. This can easily be attributed to lack of knowledge.

By the way, the issue is not just limited to NRE accounts. Returning NRIs face issues in re-designating NRO Fixed deposits too.

What is the problem?

You face three major issues if you have to break your NRE FD

- You may have opened your NRE Fixed Deposit at a higher rate. Subsequently, interest rates may have moved down. For instance, you may have opened your NRE FD for 5 years at 9% p.a. After two years, when you have break NRE FD and open a new resident FD, you can open a new FD at only 7% p.a. So, essentially, you lose 2% interest for 3 years.

- Breaking (premature withdrawal) of NRE FD may attract penalty. Apart from that, you get interest for only the period for which you maintained the fixed deposit. Continuing with the above example, let’s assume the rate for 2 year FD was 8.5% p.a. Therefore, if you break the 5-year NRE fixed deposit after 2 years, you will earn only 8.5% p.a. for two years (and not 9% p.a.) If the bank charges a penalty for premature withdrawal, it can further reduce your income.

- NRE FD does not earn any interest if you break the FD before 1 year. Therefore, in extreme scenarios where you have to break before 1 year, you do not get anything.

Even though banks should permit you to continue your NRE FD as resident FDs at the earlier contracted rate, banks don’t allow you to.

Returning NRIs: What happens to your NRE, NRO and FCNR accounts?

Read: How can NRIs invest in Mutual Funds in India?

Someone chose to challenge the Banks

Many investors do not take up the fight with the banking system for they think their efforts will not yield any results. However, Suren (name changed to hide identity), a regular reader of this blog, thought differently and took up the issue with the banks.

He had NRE FDs with 8 banks. He approached all the banks and referred them to Master Directions. He met branch officials, dropped e-mails, dropped reminders and finally was able to get his NRE FD as resident fixed deposits i.e. he did not have to break his NRE FD. With a few banks, it took him up to 6 months to sort out the matter.

He was kind enough to share his experience in a comment and even shared his e-mail communication with the banks with me. And he didn’t stop at that. He also gave me permission to share his e-mails so that others could also benefit.

In this post, I will share his communication with the banks. I have hidden his e-mail details to maintain privacy. If you need his e-mail id, you can drop an e-mail at my support id. I will discuss with Suren. If he agrees to share his e-mail id with you, I will pass on the details.

Suren had NRE FDs with the following 8 banks.

- State Bank of India

- Corporation Bank

- Syndicate Bank

- Bank of Baroda

- Canara Bank

- Karnataka Bank

- Axis Bank

- Vijaya Bank

If you have NRE FDs with any of aforementioned banks and the bank official is not permitting you to re-designate NRE FD as resident FD, you know what to do.

Even if you have NRE FDs with other banks, you can escalate to the senior management of the bank and get it done. Do note the local branches may not be aware of the rules. Hence, it may be necessary to escalate this to senior management.

As Suren pointed out, “Some banks have poor co-ordination between Head Quarters and their branches and they consider it as a not so important matter for sharing with their staff across the country.”

Thank you Suren for sharing your experience.

Excerpts from Communication with some of the Banks

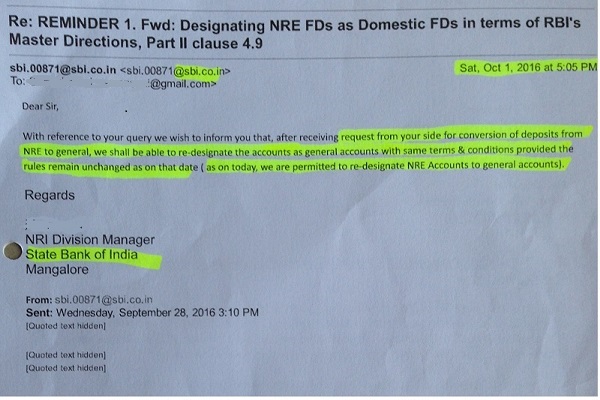

State Bank of India

Syndicate Bank

Canara Bank

On Mon, Oct 3, 2016 at 5:00 PM, CANARA BANK

BALMATTA <cb1333@canarabank.com> wrote:

Dear Sir / Madam,

Facility of re-designation accounts i.e. conversion of Non Resident Indian account to Resident account and vice versa is not available in CBS at present and the same has been taken up with vendor as change request.

Hence system is not deducting TDS for NRE term deposits even though customer category changed from NRI to Individual. The same has to be handled manually till functionality enabled in CBS.

Karnataka Bank

From: mlr.bejai@ktkbank.com

Dear Sir,

We are once again sorry for the inconvenience caused in this matter and once again we clarify that

1. As per RBI guidelines, We will convert the NRE status to Resident without altering due date and interest rate of existing NRE fixed deposits.

- TDS will be deducted as per Resident status on Converted NRE Fixed deposits with effective from the Conversion date( not retrospective).

We hope our answers will satisfy.

Axis Bank

From: nodal.officer@axisbank.com

Dear Sir,

We apologize for the inconvenience caused to you in the matter.

With regards to your concerns we would like to reply as below

- i) to continue maintaining NRE FDs and thereby incur penalties under FEMA law , *while they are mandated by FEMA to get their NRE a/cs re-designated by Banks as Resident accounts, immediately upon return to India,* .

Reply: Please refer RBI Circular-

https://www.rbi.org.in/scripts/ECMUserParaDetail.aspx?Id=525&CatID=14

Quote:

NRE accounts should be redesignated as resident rupee accounts or as RFC accounts (if eligible), at the option of the account holder immediately upon the return of the account holder to India if authorised dealer is satisfied that he has returned to India for taking up employment or for carrying on a business or vocation or for any other purpose with the intention of residing in India for an uncertain period. Where the account holder is only on a short visit to India, the account may continue to be treated as NRE account even during his stay in this country. In respect of funds held in fixed deposits in NRE accounts, interest will be payable at the rate originally fixed, provided the deposit is held for the full term even after conversion into resident account.

Unquote

The Returning NRI can keep the NRE/FCNR Deposit till maturity. However, except the provisions relating to rate of interest and reserve requirements as applicable to FCNR(B) deposits, for all other purposes such deposits shall be treated as resident deposits from the date of return of the account holder to India. The customer can also convert all the deposits to a resident deposit without changing the rate of interest.

Vijaya Bank

From: bijai1300@VIJAYABANK.co.in

Referring to the trailing mail received from the customer, please be informed that :

1) Upon returning to India permanently, the existing NRE FD account of the account-holder is required to be converted to Domestic FD A/c. without changing the maturity pattern. Rate of Interest will remain the same.

2) Applicable TDS will be collected by the system once transfer of account from NRE sub-head to Domestic sub-head is done by the branch.

Interesting Case with Bank of Baroda

With Bank of Baroda, the bank acknowledged that Suren was right. However, it mentioned that its technical systems didn’t support such changeover (re-designation) and that the matter has been taken up with the technical staff of the team. Subsequently, the changes were made.

In fact, it made changes to the web page for facilities available to returning Indians (as told by Suren).

You can check the web page for returning Indians on Bank of Baroda website where it is clearly mentioned NOW that you can continue NRE FD as resident FDs at agreed rate of interest.

You can see what knowledge of regulations coupled with persistence can do.

What about tax treatment of such Fixed Deposits?

Since you NRE FDs have become resident FDs, the interest will no longer be exempt from tax and you will have to pay. The interest income will be taxable and may even be subject to TDS (Tax deduction at source).

In any case, if you are no longer resident as per FEMA, even the interest from NRE account is taxable. Section 10 of the Income Tax Act exempts interest income from NRE account/deposits only for non-residents as per FEMA. By the way, the definition of NRI is different as per FEMA and Income Tax Act.

Interest on NRO deposits is taxable even for NRIs. Therefore, nothing changes on taxation front.

Additional Read

Book: In the Wonderland of Investments for NRIs by A.N.Shanbhag/Sandeep Shanbhag