In an earlier post, I discussed how NRIs can invest in mutual funds and the challenges they face while investing in India. In this post, let’s look at mutual fund taxation for NRIs (non-residents).

NRI Mutual Fund Taxation: How is it different from residents?

There are a few minor differences.

#1 Long-Term Capital Gains Tax on Debt Funds

For residents, LTCG (holding period > 3 years) are taxed at 20% after indexation.

In the case of Non-residents, the tax treatment depends on whether the mutual fund units are listed or not.

For the units that are listed (close-ended funds, FMPs etc), LTCG is taxed at 20% after indexation. For unlisted units, the LTCG is taxed at flat 10% (without allowing for indexation). Now, most funds that we invest in are open-ended funds and these funds are not listed. Therefore, no benefit of indexation for NRIs in case of open-ended debt funds.

If a resident sells units of HDFC Liquid Fund and makes LTCG of Rs 40,000, he will have to pay LTCG at 20% after indexation. On the other hand, an NRI will have to pay LTCG tax at 10% (Rs 4,000) on such gain.

For more clarity on this, refer to Section 112 of the Income Tax Act.

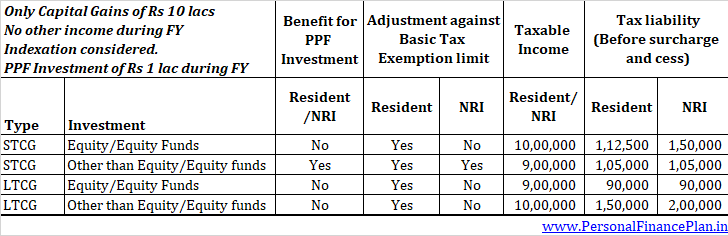

#2 Adjustment against Basic Exemption Limit

For a resident, if the total income (before including capital gain) falls below the minimum tax exemption limit, the long/short term capital gain can be reduced by the amount of such shortfall.

In the case of non-residents, the above can be done only for short-term gains on non-equity funds (debt funds, gold funds etc). Long-term capital gains on the sale of equity/debt funds or STCG on the sale of equity funds can’t be revised downwards even if your total income is short of minimum tax exemption limit.

By the way, the minimum tax exemption limit for Non-residents is Rs 2.5 lacs irrespective of age.

It is easier to explain this with the help of an example.

This aspect is discussed in detail in this post.

#3 For NRIs, Capital Gains are subject to TDS

In the case of residents, AMCs (mutual fund houses) do not deduct any tax at source. No TDS on capital gains for residents.

In case of NRIs, the redemptions (and the resulting capital gains) are subject to TDS.

For STCG on equity funds (holding period <= 1 year), TDS on such gains shall be deducted at 15%.

For LTCG on equity funds (holding period > 1 year), TDS on such gains shall be deducted at 10%. Even though such LTCG is exempt to the tune of Rs 1 lac per year, TDS on these gains shall still be 10%. The reason is AMC does not know about your other LTCG.

For STCG on debt funds (other than equity funds, holding period <= 3 years), TDS on such gains shall be deducted at 30%. Even though such gains are taxed at your marginal rate and your marginal rate can be lower than 30%, TDS is still deducted at 30%. AMC does not know about your marginal income tax rate.

For LTCG on debt funds (other than equity funds, holding period > 3 years), TDS on such gains shall be deducted at 10% or 20% after indexation.

If excess tax has been deducted by way of TDS, you can claim it back while filing income tax return.

For more on TDS on capital gains for NRIs, refer to this post.

NRI Mutual Fund Taxation: How is Dividend Taxed?

The tax treatment of dividends is exactly the same for residents and non-residents.

Dividend paid from mutual funds is exempt from tax for both resident and non-residents.

Just that the AMC deducts Dividend Distribution Tax (DDT) before paying dividends to investors.

DDT is 10% in case of equity funds and 25% in case of debt funds. Surcharge at 12% and Cess at 4% (FY2019) is applicable on the DDT.

Since the DDT is calculated on gross basis, the effective tax hit is slightly higher than the aforesaid rates.

For more on how DDT is calculated and whether it makes sense to invest in dividend option of MF schemes, refer to this post.

In this post, I have mentioned about taxation in India. Depending upon tax laws in your country of residence, capital gains and dividends from MF investments in India may be subject to taxes there as well. If India has DTAA with your country of residence, you can get credit for the taxes paid in India.

Disclaimer: I am not a tax expert. You are advised to consult a Chartered Accountant before acting on information provided in the post.