Conventionally, when you borrow, you borrow from an institution, say a bank or a Non-Banking Finance company (NBFCs). In the case of Peer-to-Peer lending, you don’t borrow from an institution. Instead, the lenders are common individuals like you and me.

To put it another way, in case of peer-to-peer lending, both the borrower and the lender are common individuals. Please understand I am not talking about local money lenders.

Fair enough. This does not sound too complex.

However, if you are a borrower, where do you find such individuals who want to lend? Or if you are a lender, where do you find borrowers who may be willing to pay you a high rate of interest?

This is where Peer-to-Peer lending platforms can come in handy. These are online platforms that bring interested borrowers and lenders together.

In this post, I will discuss Peer-to-Peer Lending platforms, regulations surrounding the practice and the risks and rewards of participation.

What do regulations say about such Peer-to-Peer Lending Platforms?

The Reserve Bank of India (RBI) is the regulator in this case.

In October 2017, the Reserve Bank came out with regulations (master directions or guidelines) for Peer-to-Peer lending platforms. This will provide much needed credibility boost to the entire industry. You can read the RBI circular here. You can read the circular in PDF format too.

Here are the key points of those regulations.

For Lenders

- Your aggregate exposure (as a Lender) to all the Borrowers across Peer to Peer lending platforms shall not exceed Rs 10 lacs at any point of time. Technically, Rs 10 lacs is the maximum amount that you can invest across P2P lending platforms at any point of time.

- Your aggregate exposure (as a Lender) to a Single Borrower across all the P2P platforms shall not exceed Rs 50,000. In my opinion, this is a good move. This move ensures diversification.

- The lender must provide a certificate that such limits are being adhered to.

- You are entitled to details about the borrower including personal identity, required loan amount, interest rate sought and credit score and risk rating (as determined by P2P lending platform).

For Borrowers

- Your aggregate borrowing from all the Lenders across P2P platforms shall not exceed Rs 10 lacs at any point of time. Clearly, you can’t borrow more than Rs 10 lacs (in total) across P2P platforms.

- You can’t borrow more than Rs 50,000 from a single lender across all P2P lending platforms.

- The borrower must provide a certificate that such limits are being adhered to.

- As a borrower, you will get details about the proposed loan amount (from the lender) and interest rate demanded. You are not entitled to identity and contact details of the lender.

- Your loan request may be funded by multiple lenders.

For Peer to Peer Lending Platform

- The maximum duration of the loan on Peer to Peer lending platform can be 36 months.

- The Peer to Peer lending platform must register with Reserve Bank as a Non-Banking Financial Company. RBI refers to such platforms as NBFC-P2P.

- The P2P lending platform must only serve as an online marketplace or platform to bring borrowers and lenders together.

- The P2P lending platform cannot raise deposits.

- The Peer-to-Peer lending platform cannot lend on its own.

- P2P platforms cannot provide or arrange any kind of credit enhancement or credit guarantee. Therefore, if you are a lender, the risk of lending is entirely yours.

- As I understand, the loans on P2P platforms have to be unsecured loans. As a lender, you wouldn’t have any security. Frankly, this may not be as bad a rule. Creating security will only add to the cost to the borrower.

- P2P lending platforms must obtain a certificate from the borrower/lender that the borrowing/lending limits (as mentioned earlier) are being adhered to.

- The interest rates displayed on the website shall be in Annual Percentage Rate (APR) format.

- P2P lending platform is not allowed to cross-sell any products expect for loan insurance products.

- P2P platform must undertake due diligence on all participants. It must undertake credit assessment and risk profiling of the borrowers and disclose this to the prospective lenders.

- P2P lending platforms are required to register with all the Credit Information Companies (CICs or Credit Bureaus) such as CIBIL and provide credit information to the CICs on a regular basis (atleast on a monthly basis). This is quite important if you are a borrower. If you thought you could escape the eyes of credit bureaus even if you didn’t pay back, you are wrong. Everything is recorded.

- The P2P platform must facilitate documentation and assist in disbursal and repayment of loan amounts.

Funds Transfer Mechanism: Source: RBI Circular dated October 4, 2017

Which are the prominent Peer to Peer lending platforms?

The prominent ones are Faircent, i2iFunding and LendBox.

Please understand I have not used any of the platforms. I am merely going by the results thrown up by Google. There are many others around. I also do not vouch for the aforementioned platforms. You must do due diligence on your own. I must disclose I have interacted with the Founder of i2iLending in the past.

As a borrower, you can put up your loan request with the amount and the interest rate sought.

The P2P lending platform may ask for additional information that can be furnished to the prospective lender. Do note it is possible that the P2P platform may reject your application outright based on their eligibility criteria.

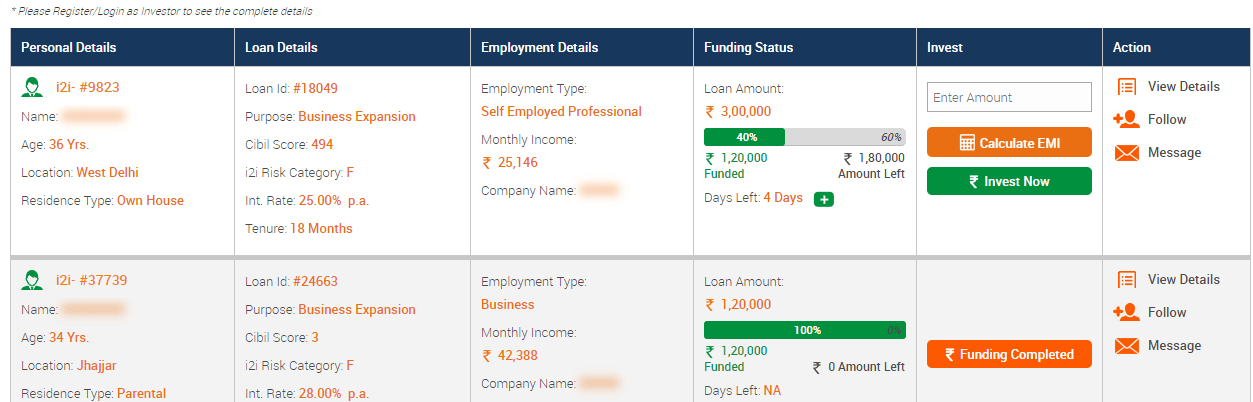

If you loan application is accepted and listed here is a snapshot of the information that is available to every lender on i2iFunding before they make up the choice. You can see details such as location, monthly income, nature of employment, CIBIL score, risk category etc too. Please understand different P2P platform may choose to display different pieces of information.

Lenders can review the information and make the choice.

A P2P platform may also do physical verification of the borrower.

What are the interest rates for borrowing on Peer to Peer lending platforms?

The interest rates can go up to as high as 30-36% p.a.

When I took a cursory glance, I couldn’t find any loan below 20% p.a., which is quite high. And this is merely the interest cost.

The P2P platform also needs to make some money. I checked the fees on a couple of platforms (Faircent and i2iFunding). The fee depends on the risk rating of the borrower. Lower the rating, higher the fees.

The processing fee ranged from 3% to 8% of the loan amount. And yes, GST will be applicable over and above this fee.

Therefore, the real cost to the borrower can be quite high.

As a lender, what should you do?

Firstly, never forget that you are lending to borrowers who might be struggling to borrow elsewhere.

Though you might feel that you are being compensated for the risk in terms of high-interest rate, the odds may not really be in your favor to begin with.

If the borrower can’t keep up with the high rate of interest, you are the eventual loser. For you to make money off the borrower, the borrower must be in a position to repay.

Beyond a point, it is virtually impossible to assess credit risk in every case. I doubt the borrower will provide you the level of detail.

Even though you have a legal recourse, the quantum of the loan may not justify the cost of legal proceedings. Remember peer-to-peer loans are unsecured loans.

Though I can’t say with certainty, there will be a lot of people who may take this route to raise funds to avoid the scrutiny of banks or any other credit institution. Even they are aware that you may not follow up with the legal proceeding. So far as borrowers are concerned, there is a clear case of adverse selection.

Additionally, please understand, the interest income from such lending will be taxable at your marginal income tax rate (as per your income tax bracket).

Please understand I am not asking you to stay away from such Peer-to-Peer lending. However, you must appreciate the risks involved.

If you are planning to lend on such platforms, suggest you diversify your exposure. When I talk about diversification, I mean lend to all types of borrowers. Do not just stick with those who are willing to pay you the highest rate.

As a borrower, what should you do?

If you are a genuine borrower, do assess the all-in-cost. You just don’t have to pay the interest rate. You have to pay the processing fees, platform charges etc. If you consider such charges too, the cost of borrowing can be extremely high.

I believe, for any borrower, a peer-to-peer lending platform, must be the last resort for borrowing. If the bank or the NBFC were willing to lend, they will most likely lend at much lower rates.

As with any loan, make sure that you can repay. Even though such loans are unsecured, the lenders still have legal recourse in case of non-payment.

Your credit history will also be damaged if you do not pay back the money on time.

PersonalFinancePlan Take

Frankly, I am quite excited about the opportunity to earn high rates of interest. However, at the same time, we must appreciate the high risk involved. In addition to the repayment ability, the adverse selection of borrowers poses a major problem.

If you must participate as a lender, lend in small amounts to different kinds of borrowers (with different risk ratings). Do not simply chase the highest rate of return.

You can set up a maximum for each borrower (10% of your capital earmarked for P2P lending) and do not breach those limits.

Be prepared for a few defaults. Hopefully, the high rates from other loans will keep your net return high enough to justify the risk taken.

Disclosure: I have not participated in peer to peer lending opportunity as yet (as on February 17, 2019).

Image Credit: Pixabay