Investment decisions shall never be driven by tax considerations alone. I have reiterated this point in many of my previous posts. However, that does not mean taxation shall not be considered while selecting an investment product. Taxation is an important parameter and should be part of every investment decision.

A product X may be offering you better pre-tax returns. However, as an investor, you should be more concerned about post-tax returns. For instance, if you have to pay 30% tax on 8% interest, the effective return is only 5.6% p.a. In comparison, a product that offers 7% tax-free interest fares better in terms of post-tax returns.

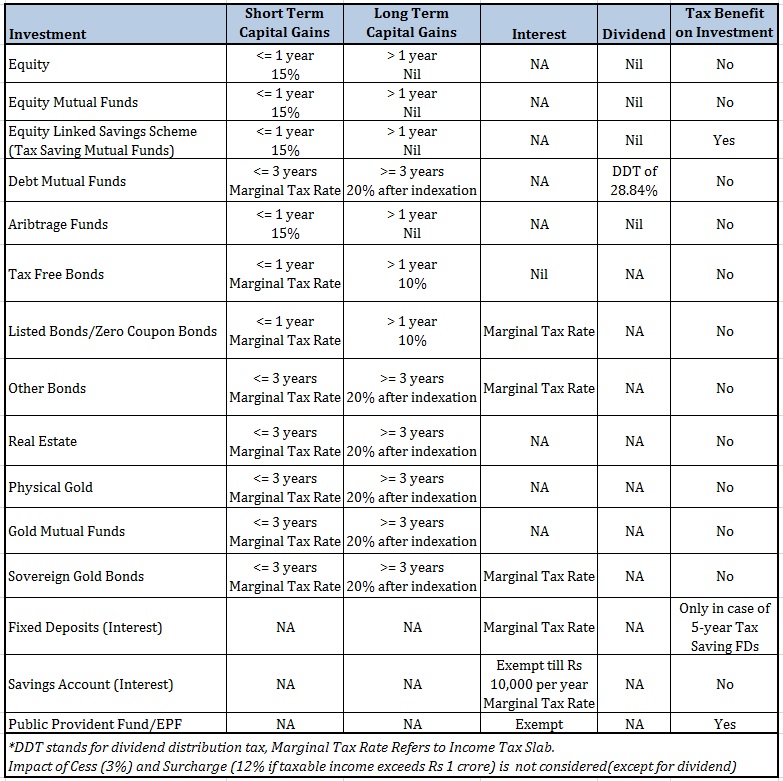

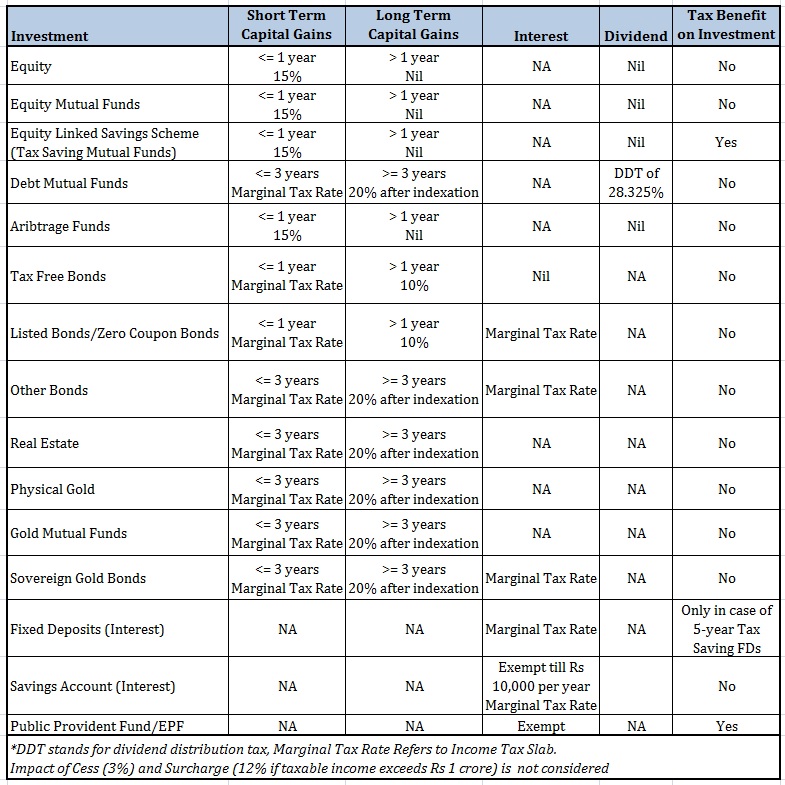

In this short post on taxation of various investment products, I will tabulate the tax treatment of various asset classes. This will act as tax reckoner for your investments.

Must Read: All you need to know about Short Term Capital Gains Tax

Must Read: All you need to know about Long Term Capital Gains Tax

Some of the examples mentioned above may have certain exceptions.

If you are dealing in unlisted shares (say shares in a startup firm), you need to hold the shares for at least 36 months for your investment to be classified as Long Term Capital Asset (Section 2(42A)).

Moreover, for tax treatment of capital gains on equity and equity mutual funds (including ELSS), the aforesaid rate is applicable only if Securities Transaction Tax (STT) is paid on sale of such instruments (Section 111A).

If STT is not paid, short term capital gain will be taxed at the marginal income tax rate (or income tax slab). And long term capital gains will be taxed at 20% after adjusting for indexation.

You need not worry about these conditions. Most readers of this blog would only trade on stock exchanges. Hence, STCG at 15% and LTCG (tax-exempt) will apply.

![]()

{kind=link}

You can use tax information about taxation to make investment decisions.

Let’s suppose you are planning to invest in a debt product for medium term (3-5 years). You want to decide between a bank fixed deposit and a debt mutual fund.

If you invest in a fixed deposit, the interest income will be taxed at marginal income tax rate. If you invest in a debt mutual fund and sell after 3 years, your capital gains will be treated as long term capital gains and taxed at 20% less indexation.

Thus, for someone in 30% tax bracket, investment in debt mutual funds can be beneficial at least on the taxation front. As mentioned, taxation shall not be the sole criterion for selecting investments. If you invest in debt MF that invests in low quality credit instruments, you face some credit risk. A default by any of the underlying securities can wipe off the capital gains.

Moreover, by investing in debt mutual funds, you are exposing yourself to market risk. Bond prices (underlying investments of mutual funds) have inverse relationship with interest rates. Hence, if the interest rates go up, the bond prices will go down and the debt MF performance will suffer. This is especially true for debt MF with high interest rate sensitivity (high duration).

Bank Fixed Deposits do not typically face such issues. Of course, even banks can default but the chances are less (Government or RBI would come to your rescue).

Do note if you are planning to invest for less than 3 years, the taxation of fixed deposits and debt mutual funds is similar.

Additional Read: Mutual Funds: Growth or Dividend?

Other Investment Avenues

There are a few investment avenues that I have not mentioned in the table above. Some of them are New Pension Scheme (or pension plans in general) and insurance products (ULIPs and traditional plans).

With NPS and insurance products, there are many conditions that determine tax treatment. Hence, rather than capturing the tax treatment in a table, I am listing out individual posts that will help you understand their tax treatment.

Must Read: NPS: Tax Benefits and Tax Treatment at Maturity

Must Read: All you need to know about Tax Implications of Life Insurance

Do consider the tax treatment in mind while comparing and selecting investment products.

Image Credit: Tax Credits, 2012. The original image and information about usage rights can be downloaded from Flickr/TaxCredits.net