Balaji and I have been working together for many years. When I recently shared my review of LIC Jeevan Labh (Plan 936), he wrote to me, “When you never recommend traditional plans, what is the point of reviewing such plans?”

I responded, “It is important to rule out bad investments before you make good investments with conviction. Otherwise, you will keep going back to bad investments. Therefore, even a poor review is useful for many investors. At least you know what to avoid.”

Moreover, these plans are sold so aggressively that my clients regularly seek my feedback about such plans. And it always helps if you support the analysis with numbers and data. Unlike me, numbers don’t have any biases. And hence such posts.

In this post, let’s review yet another traditional life insurance plan. SBI Life Smart Platina Plus.

SBI Life Smart Platina Plus: Important Features

- Non-linked (It is a traditional plan and NOT a ULIP)

- Guaranteed Returns

- Non-participating (You can calculate upfront how much you will get and what will be your net returns). To find out what kind of life insurance plan you are buying, refer to this post.

- Limited Premium (Policy term is longer than premium payment term)

- Minimum age at entry: 30 days Maximum entry age: 60 years

- Maximum age at maturity: 99 years

- Premium Payment Term: 3 options (7, 8 or 10 years)

- Payout period: You get regular income during the payout period. Payout period begins exactly 3 years after you pay your last premium (assuming annual premium payment). 4 options: 15, 20, 25 and 30 years. 30 years option is not available for 10-year premium payment term.

- Policy Term = Premium Payment Term + Payout Period + 1

- Two variants: Life Income and Guaranteed Income

- The nomenclature “Life Income” is misleading since it gives the impression that you will get income for life (like an annuity plan). You won’t get income for life.

- SBI Life Smart Platina Plus offers 3 benefits: Death Benefit, Survival Benefit and Maturity Benefit

SBI Life Smart Platina Plus: Death Benefit

Death Benefit = Highest of the following 3 numbers

- Basic Sum Assured = 11 times Annualized Premium (this ensures that any payouts from this policy will be exempt from tax. OR

- Annual Guaranteed Income * Death Benefit Factor for Guaranteed Income Benefit + Maturity Benefit * Death Benefit Factor for maturity benefit

- 105% of the total premiums paid up to the date of demise

For (2), the policy wordings provide the data in Death Benefit factor. From what I observed, the (1) will be greater than (2) in the initial years. After that, (2) will be greater.

The calculation is the same under both the variants (options).

Life Income Option

In the event of the demise of the policyholder anytime during the policy term, the Death Benefit will be paid out to the nominee and the policy will terminate.

Guaranteed Income Option

Demise BEFORE commencement of Payout period: The Death Benefit is paid out to the nominee and the policy terminates.

Demise AFTER commencement of the Payout period: The Death Benefit is paid to the nominee. In addition, the nominee continues to get the Guaranteed Income Benefit (Survival benefit).

And that’s the only difference between the two options.

In the Life Income Option, if the policyholder dies during the payout period, the nominee gets only the Death Benefit.

In the Guaranteed Income option, if the policyholder dies during the payout period, the nominee gets the Death Benefit + Survival Benefit.

Since the insurer must pay more in the Guaranteed Income option, the returns will be lower in this variant (everything else being the same).

SBI Life Smart Platina Plus: Survival Benefit

During the payout period, the policyholder receives a “guaranteed income”. And you get this guaranteed income under both “Life Income” and “Guaranteed Income” variant. Confusing, isn’t it?

The product designers could have called this benefit “Fixed income” or “pre-determined income”. Or changed the name of the variant from “Guaranteed Income” to something else. I am not sure if this is deliberate or plain oversight. Irrespective, this is quite confusing.

To avoid confusion, I would call this “Guaranteed Income Benefit“.

Guaranteed Income Benefit is expressed as a percentage of Annualized Premium.

And the percentage depends on the

- Age at entry (higher the entry age, lower the percentage)

- Premium Payment Term

- Payout period

- Payout frequency (monthly, quarterly, half-yearly and annual)

Caveat

If your variant is Life income, the Guaranteed Income Benefit (Survival Benefit) will cease from the date of death of the Life Assured. Your nominee will get the death benefit and the policy will terminate. We saw this above in the description for death benefit too.

If your variant is Guaranteed income, the Guaranteed Income Benefit will be paid over the payout period

SBI Life Smart Platina Plus: Maturity Benefit

Maturity benefit is payable if the policy holder survives the policy term.

Maturity benefit = 110% of the Total Premiums paid.

Therefore, if your annual premium is Rs 1 lac (before taxes) and the premium payment term is 7 years, you would have paid a total premium of Rs 7 lacs.

Maturity Benefit = 110% * 7 lacs = Rs 7.7 lacs

The maturity benefit calculation is the same for both the variants.

SBI Life Smart Platina Plus: What are the returns like?

The policy wordings do not provide the values for Guaranteed Income Benefit percentage. However, the good part is that you can enter your details (age, gender, premium payment, and payout terms) on SBI Life website, and the insurer emails you the benefit illustration.

First, I pick up the illustration that is provided in the policy brochure. Then, I will consider an illustration I generated from the website.

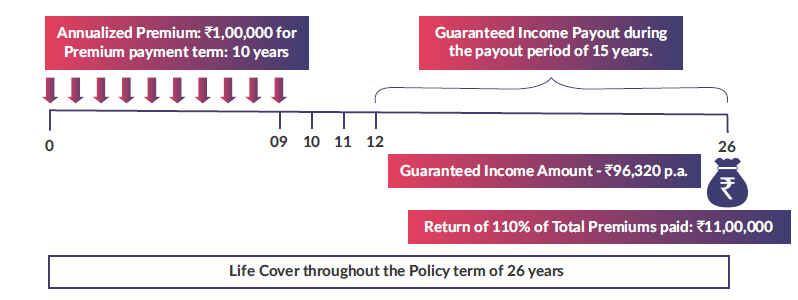

Illustration 1

- Entry age: 35 years

- Annual Premium: Rs 1 lacs (before taxes). 4.5% GST in the first year. 2.25% GST in the subsequent years

- Premium Payment term: 10 years

- Payout term: 15 years

- Policy Term: 26 years

- Variant: Life Income

So, you pay premium for the first 10 years. Rs 1.04 lacs in the first year and Rs 1.02 lacs in the subsequent years. You pay your last premium at the beginning of the 10th policy year.

From the end of the 12th policy year, you start getting the Guaranteed Income Benefit. As per the illustration, you will get Rs 99,210 per annum for the next 15 years.

At the end of 26th year, you will get the maturity benefit. 110% of Total premiums paid = 110% of 10 lacs = 11 lacs.

What is the net return (IRR)?

5.58% p.a.

Illustration 2

Everything same as Illustration 1 (except the variant is now Guaranteed Income)

From the end of the 12th policy year, you start getting the Guaranteed Income Benefit. As per the illustration, you will get Rs 96,320 per annum for the next 15 years. You can see it is lower than the value in the previous illustration (Rs 99,210).

Maturity benefit shall be the same as Rs 11 lacs.

Net return = 5.46% p.a.

We know that in traditional plans returns go down with entry age.

Let’s increase the age and see what happens.

Illustration 3

Everything same as Illustration 2 (Entry age is 50 years)

From the end of the 12th policy year, you start getting the Guaranteed Income Benefit. As per the illustration, you will get Rs 95,320 per annum for the next 15 years. You can see the benefit as gone down from Rs 96, 320 to Rs 95,320 per annum.

Maturity benefit shall be the same as Rs 11 lacs.

Net return = 5.41% p.a.

If you are interested in this product, you can enter details on SBI Life website and get the illustration over email. You can input the cash flows in excel and calculate IRR.

By the way, the illustration has a small mistake and a deliberate one at that. To rectify the mistake, just shift the payout period by 1 year.

Point to Note: There is not much difference in IRRs for Life Income option and Guaranteed Income option. But in the Life Income option, your nominee loses out on the Survival benefit (Guaranteed Income Benefit) in the event of demise during the payout period. Therefore, if you must invest in this product, suggest you select the Guaranteed income option (variant).

SBI Life Smart Platina Plus: Should you invest?

You need to weigh the pros and cons.

Let’s start with the pros.

- You lock in the rate of return at the time of purchase.

- You know upfront what your returns will be.

- Returns are guaranteed unless you expect SBI Life to default

- Okayish returns for a long-term fixed income product

- Tax-free returns

What are the cons?

Apart from the usual flexibility issues with traditional plans, the returns are too low for such a long maturity product. We considered a 26-year policy term. And the returns hovered around 5.5% p.a. Even though these returns are tax-free, it is not good enough.

I will recommend NOT to invest in this product.

However, if you must invest in SBI Life Smart Platina Plus, select the Guaranteed Income option.