PFRDA increased the maximum age of joining under National Pension System from 60 to 65 years. Here is the link to the circular.

The joining age has been increased for All Citizens model (including Corporate Sector NPS). No such provision for Government sector NPS.

Please understand investors were already allowed to continue their existing NPS accounts until the age of 70. It is the joining age that has been increased from 60 to 65.

I cannot fathom any reason except for the exclusive tax benefit under Section 80CCD(1B) why a senior citizen would want to join NPS. Well, that applies to everyone.

Now, the question that begs is whether senior citizens should consider investments in NPS.

A few things to know if you are joining the NPS after the age of 60

If you join after the age of 60, you will have both Active and Auto investment choice.

Under the Active mode, the maximum exposure to equity can be 75%. The maximum equity exposure under Active mode was hiked from 50% to 75% in May 2018.

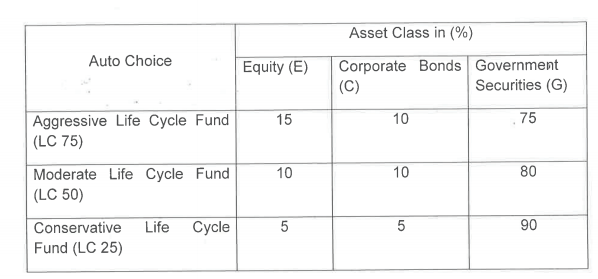

Under the Auto mode (lifecycle funds), the allocation will be as follows.

Normal Exit is allowed after 3 years. For other investors (those who join before the age of 60), the normal exit is allowed only at the age of 60 (or thereafter). Other aspects remain the same. 40% of the corpus needs to be used to purchase an annuity plan. If the accumulated corpus is less than Rs 2 lacs, you can withdraw the entire corpus lumpsum.

Exit from NPS before 3 years is considered premature exit. For other investors (those who join before the age of 60), the premature exit is not allowed before 10 years and any exit before the age of 60 or superannuation is considered the premature exit. In case of premature exit (irrespective of joining age), 80% of the corpus must be used to purchase an annuity plan. If the accumulated corpus is less than Rs 1 lac, you can withdraw the corpus lumpsum.

In the event of the death of the subscriber (who entered NPS after the age of 60), the entire corpus will be paid to the nominee of the subscriber. There is no option of annuity purchase by the nominee.

Before you decide, do consider the following aspects

The only reason why you can consider investing in NPS is that of tax benefits.

If you are retired and not working anymore, you may not have much taxes to save anyways.

The money gets locked in and you can’t exit before completing 3 years. In case of pre-mature exit, 80% goes towards the purchase of an annuity plan, effectively defeating the purpose of pre-mature exit in case of an emergency.

In any case, there is no reason why you should not invest more than Rs 50,000 per annum in NPS.

And if you are investing only Rs 50,000 per annum and you must exit NPS at the age of 70, you can’t expect to accumulate a very big corpus under NPS. Since 40% of the corpus at the time of exit must be used to purchase an annuity plan, you can expect an insignificant annuity income from the corpus. I wouldn’t be comfortable with that. I would rather take money lump sum.

PersonalFinancePlan Take

In my opinion, it is not prudent to join NPS after turning 60 (or even close to retirement).

NPS has its share of problems. However, for those who want to invest in NPS, they must:

- Have marginal tax rate of 30%

- Be sure they won’t need these funds until the age of 60

- NPS is not the only investment for retirement.

- Investment in NPS does not crowd out other investments.

- Not invest more than Rs. 50,000 per annum in NPS (because the maximum tax benefit under Section 80CCD(1B) is Rs 50,000)

For a senior citizen who plans to open NPS account, (2) is not applicable. For them, the earliest normal exit is 3 years from the date of opening the account. For senior citizens, you can tweak Point (2) to “Be sure you won’t need these funds until the age of 70”.

For a senior citizen, there are additional points/problems to consider.

- Pre-mature exit (before 3 years) is quite meaningless because you would think about premature exit only in case of an emergency. In an emergency, you wouldn’t want 80% of your money to be stuck into an annuity plan.

- Even a normal exit would provide an insignificant annuity stream.

- You can’t defer annuity purchase. You must purchase an annuity plan at the time of exit from NPS. Annuity interest rate also depends on the age. Lower the age, lower the annuity return.

What do you think?