LIC Jeevan Labh (Plan 936) is a limited premium and non-linked participating life insurance plan.

“Limited Premium” implies that the premium payment term is lower than the policy term.

“Non-linked” means LIC Jeevan Labh (Plan no. 936) is not a ULIP. It is a traditional life insurance plan.

“Participating” means you will participate in the profits of the insurer. Your bonus (reversionary or final) will depend on LIC’s performance and therefore can’t be known upfront. Thus, you cannot calculate your returns upfront. You can do that in “Non-participating” plans.

We have seen time and again that traditional life insurance plans are poor products. Such products neither provide you good life cover, nor provide your good returns. And I do not expect this new avatar of LIC Jeevan Labh to be any different.

Let’s find out more about this plan in this post and see if makes sense to invest in such a plan.

Note: I had first written this post about LIC Jeevan Labh (836) in 2016. The LIC withdrew LIC Jeevan Labh 836 in 2020 and launched a new plan LIC Jeevan Labh 936. As I see, there is only a minor difference between the 2 variants. I have updated the post for LIC Jeevan Labh 936.

Buying an insurance product: How to figure out what you are buying?

It is not easy to pen down all the thoughts about a product. Therefore, I have also reviewed the LIC Jeevan Labh (936) in greater detail in this video. Do check out.

LIC Jeevan Labh (Plan 936): Salient Features

- Limited premium payment plan i.e. premium payment term is less than policy term

- Premium Payment Terms of 10/15/16 years for policy terms of 16/21/25 years respectively

- Minimum Entry Age: 8 years

- Maximum Entry Age: 50/54/59 years for policy terms 25/21/16 years respectively

- Minimum Basic Sum Assured: Rs 2 lacs

- Maximum Basic Sum Assured: No upper limit

You can find out more about LIC Jeevan Lab plan on LIC website.

You can see there are only three possible combinations. If you pick up plan with premium payment term of 15 years, you will pay premium for 15 years while you will get life cover for 21 years. You will get the maturity amount at the end of 21 years (if you survive the policy term).

I do not see much difference between LIC Jeevan Labh and LIC New Endowment plan. The only difference I see is that LIC Jeevan Labh is limited premium payment plan. LIC New Endowment plan is a regular premium payment plan.

Difference between LIC Jeevan Labh (836) and LIC Jeevan Labh (936)

There are only a few minor differences.

Changing the Death benefit definition is a major change. For life insurance maturity proceeds to be tax-free, the minimum death benefit must be at least 10 times the annualized premium.

Therefore, there is a possibility that maturity proceeds from LIC Jeevan Labh (936) may not be exempt from tax. However, I tried to calculate premiums for various combinations of age and policy terms for LIC Jeevan Labh (936). The Base Sum Assured was always more than 10 times the annual premium. And since Sum Assured on Death is higher of (Base Sum Assured, 7 times annualized premium), you are safe. The maturity proceeds will be exempt from tax under LIC Jeevan Labh (936) too. Still, do ensure this if you plan to invest in LIC Jeevan Labh (936).

LIC Jeevan Labh (Plan 936): Death Benefit

In the event of demise during the policy term, the nominee gets

Sum Assured on Death + Vested Simple Reversionary Bonus (till date)+ Final Additional Bonus (if any)

Sum Assured on Death = Higher of (Base Sum Assured, 7 times annualized premium)

Simple Reversionary Bonus is announced every year by LIC. It is announced as per thousand of Base Sum Assured. So, if the Sum Assured is Rs 10 lacs and the bonus is announced as Rs 40 per thousand of Sum Assured, your annual bonus is Rs 40,000.

The caveat is that LIC does not credit your bank account with reversionary bonus every year. The bonus merely gets added to maturity amount and is paid at the end of policy term. No compounding benefit. Continuing with the same example, if LIC announces the same bonus for the next 25 years, your policy would accrue 40,000 X 25 = Rs 10 lacs in the next 25 years and this amount is payable to you at the time of maturity (25 years). In the event of demise too, the LIC will pay the accrued bonuses till date. As you can see, no returns on the accrued bonus.

Final Additional Bonus is applicable only in the year of maturity/death. So, it is a roll of dice. It is also expressed as per thousand of Sum Assured.

LIC Jeevan Labh (Plan 936): Maturity Benefit Illustration

Maturity Benefit = Base Sum Assured + Vested Simple Reversionary Bonus + Final Additional Bonus (if any)

LIC Jeevan Labh (836) has bonus history for 6 years. LIC Jeevan Labh (936) has bonus history for 2 years.

As you can see, the bonus value can change every year. For the illustration, I will use an optimistic estimate for Simple Reversionary Bonus. Moreover, the bonuses for Plan 836 and Plan 936 are the same. That’s expected.

Bonus increases with policy term. A 16-year policy earns a lower bonus compared to 25 year policy.

Final Additional Bonus, in any case, depends on your luck. I will consider various value of FAB to assess investment performance.

Now, these returns are not special for a long term investment. We considered a 25 year policy term.

At the same time, the returns are tax-free and do not look too bad for a fixed income product. Currently (as on September 8, 2022), PPF offers 7.1% p.a. and it does not offer any insurance. Of course, these returns from LIC Jeevan Labh are not guaranteed and a lot depends on the bonuses that LIC will announce over the policy term. We have already seen that the bonuses can go down (went down from 50 to 47 in 2020 and has stayed there since). I have considered a value of 50 for this analysis. It is possible that these bonuses may reduce further (or increase). Such changes will impact your returns.

Now, consider these returns with the lack of flexibility in LIC Jeevan Labh. You can’t surrender your plan without a heavy penalty. And there are these usual problems with all traditional plans. Therefore, I would advise you to stay away from LIC Jeevan Labh. There is no LABH in LIC Jeevan Labh.

Point to Note: With traditional plans, the returns depend of the entry age. Thus, everything else being the same (Sum Assured, policy term, same year of purchase), a 35-year-old investor would earn better returns from the plan compared to a 45-year-old (at the time of entry). This happens because the premium goes up as the age goes up.

For instance, a 45-year-old would have to pay an annual premium of Rs. 50,937 for the same policy (Rs 10 lacs, Policy term of 25 years). The maturity amount would be the same since bonuses are linked to Sum Assured. Higher premium reduces effective returns. IRR for 45-year-old would be 5.89%, 6.13%, 6,37% and 6.59% for various values of FAB as shown above.

Moreover, the returns will be higher for longer policy terms. You just need to look at the bonuses announced. Lower the policy, lower the bonus. And this applies to both reversionary bonus and the Final Additional bonus.( FAB) Yes, FAB also depends on the policy term. For instance, in FY2021, the FAB announced for 25 year policy was 450 per Rs 1000 Sum Assured. For a 16 year policy, it was Rs 25 per Rs 1000 Sum Assured.

I considered a 16-year policy. 35-year-old. Sum Assured of Rs 10 lacs. Annual premium of Rs 85,181 per annum. Simple Reversionary bonus of 43 for the entire term. FAB of 0. The IRR was 5.78% p.a. For 25-year policy, it was 6.34% p.a. (for FAB of 0).

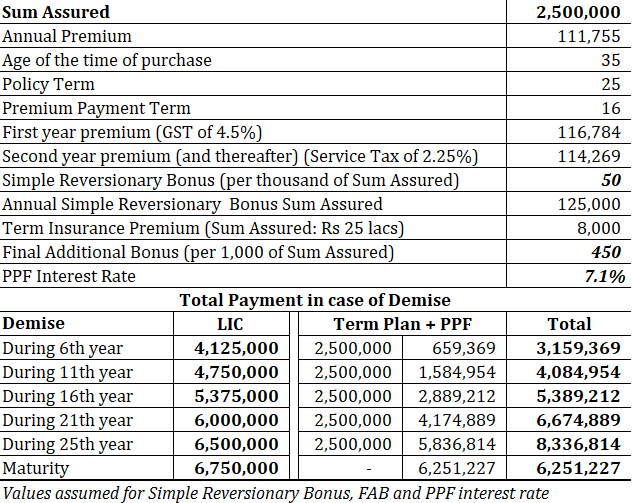

Could you have done better with Term Plan and PPF?

And I am not even talking about equity mutual funds.

I checked the annual premium rates for 25 lac cover on Policy Bazaar. For 35-year-old and 25 year policy term. The premiums were in the range of 6,000-10,000 per annum. So, instead of putting money in LIC Jeevan Labh, we buy a term life insurance plan and invest the remaining in PPF.

You can see combination of term plan and PPF is right there with LIC Jeevan Labh (expect at maturity). In my earlier analysis, PPF + Term plan was a clear winner. However, PPF rates have come down since then. But I have kept the bonus rates high. Thus, tilting the results in favour of LIC Jeevan Labh.

Had you replaced PPF with equity funds (or a balanced portfolio), you could have ended up with a much higher maturity corpus.

Since LIC Jeevan Labh premium payment term is only 16 years, how do you account for term insurance premium in the years 17 till 25th. I have withdrawn term insurance premium from accumulated PPF corpus. Yes, you can withdraw from PPF after initial maturity of 15 years.

What should you do?

I do not like traditional plans. And I do not deny my opinion is biased.

We saw earlier that LIC Jeevan Labh does not provide good returns for a long term investment, even though returns may not be bad for fixed income product.

Keep your insurance and investment needs separate. It is just so simple. You buy better life coverage. You may need a life cover of Rs. 1 crore. If you try to purchase life cover through a product like LIC Jeevan Labh, you will have to shell out Rs 4-5 lacs per annum. Now, that’s a very high premium. You might settle for a lower life cover (based on your premium payment ability). And this exposes your family to a huge financial risk. On the other hand, a term plan of Rs. 1 crore may cost only 10-15K per annum. With a term plan, you will likely not remain underinsured.

Plus, you get more flexibility with money.

Moreover, you can replicate (and perhaps even outperform) performance of traditional plans using a combination of term life plans and PPF (or mutual funds). There is no LABH in LIC Jeevan Labh. Stay away.

Additional Links

- LIC New Jeevan Anand

- LIC New Money Back Plan-25 years

- LIC Children’s Money Back Plan

- LIC Jeevan Tarun

- LIC New Endowment Plan

Featured Image Credit: Unsplash

The post about LIC Jeevan Labh was first published in September 2016 and has been updated since for LIC Jeevan Labh (936).