The tax on LTCG from equity funds was introduced in Budget 2018. This made ULIPs attractive to a number of investors. The insurance companies have jumped onto this opportunity and have launched a number of Unit-Linked Insurance Plans or ULIPs.

In this post, let’s look at the two broad categories of ULIPs. Type I and Type II ULIPs. The only difference between the two types of ULIPs is in the death benefit. The death benefit defines the amount that the nominee (under the policy) gets in the event of demise of the policyholder during the policy term. However, this difference in death benefits also impacts the returns of the two types of ULIPs.

How ULIPs work?

Unit linked insurance plans (ULIPs) are insurance products that provide the dual benefit of insurance and investment. A ULIP has many charges. Some of the charges (premium allocation, policy admin) are recovered upfront from the premium while the others (mortality charge) are recovered through the cancellation of fund units.

Sum assured is the minimum amount that one gets in the event of the death of the policyholder. Investors/policyholders are offered various investment options (equity, debt, balanced etc). You can choose the investment fund as per your requirement. The value of your investments (“fund value”) grows over a period of time through regular premium payments and the return on your investments.

ULIPs can be broadly classified into two types: Type-I and Type II ULIPs.

Death benefit under the two types of ULIPs

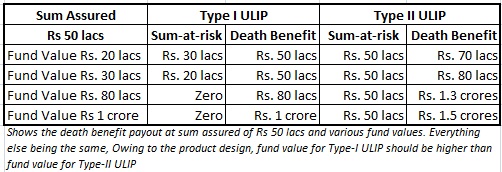

Type-I ULIP

In the event of the death of the policyholder, the insurance company pays the higher of fund value or sum assured to the nominee/beneficiary. Suppose a person has paid the premium for 8 years, the fund value has grown to 30 lacs. The Sum Assured is Rs 50 lacs. In the event of the death of the policyholder, the beneficiary will be paid Rs 50 lacs (higher of 30 lacs, 50 lacs).

Type II ULIPs

In the event of the death of the policyholder, the insurance company pays the sum of fund value or sum assured to the nominee/beneficiary. Considering the same scenario, the beneficiary would have received Rs 80 lacs (Rs 30 lacs + Rs 50 lacs)

How does this impact the return?

Among other charges, an insurance company charges a mortality charge on sum-at-risk for the insurance company. The Sum-at-Risk is the amount insurance company will have to pay from its own pocket in the event of the death of the policy holder. Expectedly, the higher the sum-at-risk, the higher the mortality charge. Additionally, the mortality charge increases with the age of the policyholder.

Under type I ULIP, since the insurance company only needs to pay the higher of the fund value and sum assured, the sum-at-risk goes down as the fund value grows. Considering the above example, if the fund value after 5 years is Rs 20 lacs, the sum-at-risk will be Rs 30 lacs (Rs 50 lacs – Rs 20 lacs). This is because in the event of the death of policyholder, the insurer needs to pay only Rs 30 lacs from its pocket. Rs 20 lacs is already there with the company in the form of fund value.

If the insured event (death of the policyholder) occurs after the fund value has grown to Rs 30 lacs, the sum-at-risk for the insurance company will go down to Rs 20 lacs. If the fund value grows to Rs 50 lacs (or higher), there is zero sum-at-risk for the insurance company. This is because its entire liability (Rs 50 lacs or higher) can now be met through fund value only. Therefore, under Type I ULIP, sum-at-risk keeps decreasing as the fund value grows and eventually becomes zero. As sum-at-risk keeps decreasing, the mortality charge also goes down and eventually goes to zero.

On the other hand, in the case of a type II ULIP, sum-at-risk is constant (sum assured) during the term of the policy. Therefore, the mortality charge does not go down and infact increases every year as the policyholder ages.

Thus, the investor/policyholder pays much lower mortality charges in a type-I ULIP. Since your returns are net of all the charges including mortality charges, Type-I ULIP provide better return due to lower incidence of mortality charges.

Under Type-II ULIPs, sum-at-risk remains the same and hence mortality charges are higher. This impacts the returns adversely. Thus, type-I ULIPs offer better returns than type-II ULIPs (everything else being same).

PersonalFinancePlan Take

Type-I ULIPs offer far superior returns than Type-II ULIPs if the policyholder survives the policy term. However, Type-II ULIPs perform far better if the policyholder passes away during the policy term.

You can go through our ULIPs vs MF + Term Insurance for comparison. So, which one is better? One provides better maturity benefits (policyholder survives the policy term) while the other provides better death benefits.

To answer the question, you have to look at why you purchase insurance products.

If you want to invest in a ULIP purely from an investment angle, Type I ULIP is better.

If you want to invest in a ULIP and get good life coverage too, Type II is better. However, you must note you can purchase life cover through a term insurance plan at a much cheaper cost.

I prefer that you keep your investment and insurance needs separate. However, if you must invest in a ULIP, I suggest that you invest in a Type-I ULIP. Ensure that you have adequate life cover.