I have reviewed many traditional plans in this blog. The conclusion was same in all the cases that the plans were strictly avoidable.

In this post, I will review LIC New Endowment Plan (814) and see how it fares against a simple combination of term plan and Public Provident Fund (PPF).

LIC New Endowment Plan (Plan no. 814) is a traditional participating non-linked life insurance plan.

Must Read: Say No to Traditional Life Insurance Plans

LIC New Endowment Plan: Key Features

- Minimum Sum Assured: Rs 1 lacs, No maximum limit

- Policy Term: 12 to 35 years

- Premium payment term is same as policy term.

- Minimum Entry Age: 8 years, Maximum Entry Age: 55 years

- Maximum Age at Maturity: 75 years

How LIC New Endowment Plan works?

You pay an annual premium for the duration of the policy.

If you survive the policy term, you get Sum Assured + Vested Simple Reversionary Bonus + Final Additional Bonus, if any.

Let’s try to understand this with the help of an example.

Every year, LIC announces a simple reversionary bonus. This bonus is awarded as per thousand of Sum Assured. So, if the Sum Assured (life cover) under the plan is Rs 10 lacs and LIC announces a reversionary bonus of Rs 40 per thousand of Sum Assured, your bonus for the year will be Rs 40,000 (40*10 lacs/1,000).

Do note the simple reversionary bonus merely gets vested. You do not get anything in hand. You get this amount only the time of maturity. And you don’t earn any return on the bonus amount. There is no element of compounding of returns.

It is not difficult to see Rs 40,000 today is not same as Rs 40,000 20 years hence. Inflation will eat into the value.

Assuming the plan is 20 years and reversionary bonus stays at Rs 40 per thousand of Sum Assured, you will earn Rs 8 lacs (20 X 40,000 per year).

In addition, you also get Final Additional Bonus (FAB). Even though FAB is announced every year, it is applicable to your policy only in the year of maturity/demise. So, if LIC does not announce any FAB in the year of maturity of your plan or demise, you (your nominee) do not get any Final Additional Bonus. FAB also depends on Sum Assured and policy term.

Let’s not get so harsh. Let’s assume in the above example, LIC announces a FAB of Rs 200 per thousand of Sum Assured. Your FAB will be Rs 2 lacs (200 X Rs 10 lacs/1,000).

Maturity Value = Sum Assured + Vested Simple Reversionary Bonus + FAB = Rs 10 lacs + Rs 8 lacs + Rs 2 lacs = Rs 20 lacs.

Death Benefit (if the policy holder dies during the policy term)

In the event of death of the policy holder during the policy term, the policy holder gets the sum of Sum Assured, vested Simple Reversionary Bonus and Final Additional Bonus, if any.

You can read policy wordings here.

Benefit Illustration: LIC New Endowment Plan

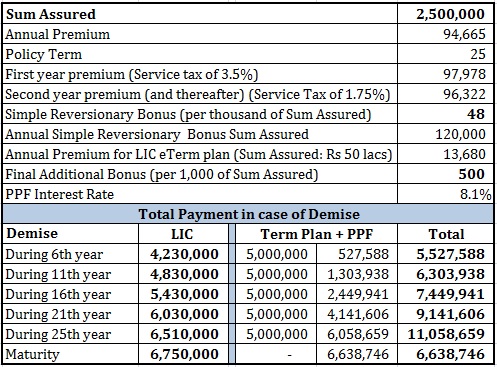

I have considered premium for a 35 year old for Sum Assured of Rs 10 lacs. Policy term is 25 years. You can find out the premium for the plan here.

Let’s consider various scenarios if the policy holder survives the term.

As for the values of Simple Reversionary Bonus, LIC has announced bonus of Rs 48 per Rs. 1,000 of Sum Assured for the last two years (for LIC New Endowment plan with policy term of over 20 years). So, Rs 48 is a fair assumption.

For Final Additional Bonus, I have considered various values of FAB and tried to assess the impact.

You can see the returns are extremely poor. The safest PPF gives 8.1% at present (August 25, 2016). You can argue PPF interest rate is subject to change every quarter. However, so is LIC bonus. You cannot expect LIC to announce the same bonus if the PPF interest rate goes down to 6% p.a.

Comparison with combination of Term Plan and PPF

You may argue that PPF is a pure investment product while LIC New Endowment plan has an insurance element too.

I agree. To make a fair comparison, I will add term insurance too. I take a term plan of Rs 50 lacs (Age: 35 years, Term: 25 years). Since many of us have distrust towards private insurers, I have picked up eTerm plan from LIC itself. The annual premium for eTerm plan is Rs 13,680.

To compare, I reduce the annual premium of term plan from annual premium for LIC New Endowment plan. The remaining gets invested in PPF.

You can see a simple combination of term plan from LIC and PPF easily outperforms money back plan in every scenario except when the policy holder survives the term.

You can argue LIC New Endowment plan better in case the policy holder survives the policy term.

However, you must note, I have taken a very generous value of Final Additional Bonus (Rs 500 per thousand of Sum Assured). At a lower value of Final Additional Bonus, you will end up lower than PPF + Term plan combination.

Additionally, I have considered term plan from LIC. Plans from private players are cheaper.

For a term of 25 years, you could also have taken exposure to equity mutual funds, which would have given you better returns. At 10% return, you could have ended up with a corpus of ~90 lacs.

In any case, if maturity corpus was your concern (and not life cover), you could have skipped term cover and invested the entire amount in PPF. You would have got higher corpus (~Rs 77 lacs) in PPF.

Read: Which is the best Term Insurance Plan for you?

Issues with LIC New Endowment Plan?

- Insurance and investment are mixed. If you opt for such products, your premium payment ability will determine your life cover. This shouldn’t be your approach. With this approach, you are likely to remain underinsured. For instance, in this LIC plan, you need to pay ~Rs 98,000 to get a life cover of Rs 25 lacs. Many of us may not be in a position to spend so much. What can this lead to? You will settle for life cover which you can afford. If you can pay premium of Rs 50,000, you will settle for cover of say Rs 12 lacs. Not the right approach.

- The correct approach is to assess your life insurance requirement. Purchase term life cover for the amount. Invest what is left after purchasing the life cover.

- You are getting guaranteed poor returns and low life cover.

- You cannot exit without incurring a heavy penalty. Surrender charges are very high.

PersonalFinancePlan Take

You are better off staying away from LIC New Endowment Plan. Keep things simple. Keep your insurance and investment needs separate. Purchase a pure term life cover and invest the surplus.

By the way, I have nothing against LIC. All private insurers sell such plans. You are advised to avoid such plans from private insurers too.