You are NOT comfortable with the low interest rates on your bank fixed deposits. Rightly so since you would not have seen such low FD interest rates ever in your life. Low interest rates hurt even more when you rely on interest income to fund your monthly expenses.

You are desperately looking for solutions to enhance your income without taking too much risk.

You come across Covered Bonds (or Covered Market Linked Debentures) that offer you 10%-12% p.a. These products are showcased as low-risk products and an alternative to your bank fixed deposits.

Isn’t this exactly what you were looking for?

However, before you invest, shouldn’t you understand how these bonds work and the associated risks?

In this post, let us find out what Covered Bonds are? How are these bonds structured? How do you get such high interest rates? What are the risks? How is the income from these bonds taxed? Should you invest?

Please understand Covered Bond or Covered Market linked debentures can be structured in many ways. That’s what makes these bonds very difficult to analyze. I will look at a very generic structure in this post.

What are Covered bonds?

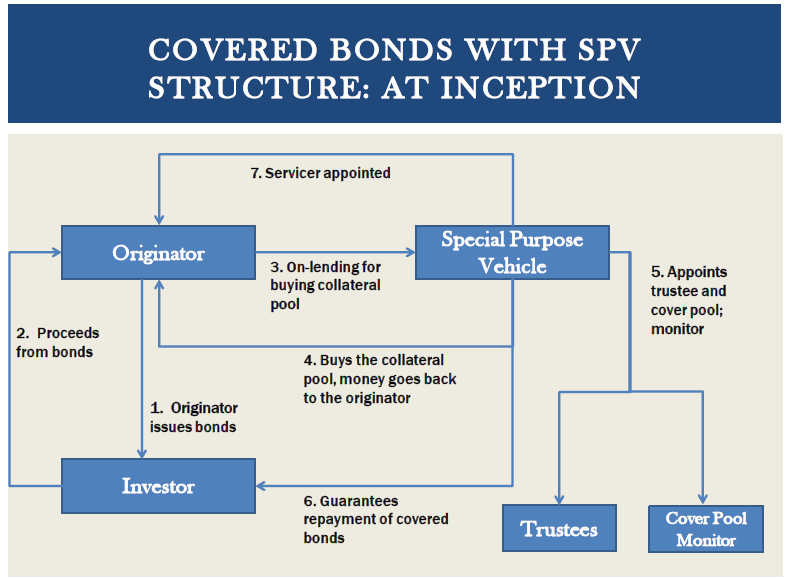

Let us first look at the structure of such a bond.

- An NBFC (or any lender) issues loans to its borrowers.

- Packages some of those loans into a pool and assigns (hypothecates) to a special purpose vehicle (SPV Trust). These loans could be gold loans, vehicle loans or any other kind of loan. Exclusive first charge is created on this pool of assets (loans) in favour of the SPV Trust. While I do not understand much legal details, this helps if the NBFC goes bankrupt. This pool of assets will not be clubbed with other assets for liquidation. For this, these covered bonds are called bankruptcy protected

- Covered bonds issued against this collateral of pool of loans.

- The pool of the loans (assigned in favour of SPV Trust) acts as collateral for the Covered Bonds. The collateral value is higher than the quantum of covered bond issuance. For instance, the NBFC issuer may be required to maintain a security cover of 1.25 times the outstanding loan amount.

- On covered bond maturity date, the NBFC will pay back the entire amount and take back the pool of loans from the SPV.

Have skipped details in my explanation. Found this brilliant chart on VinodKothari.com that explains how this structure exactly works.

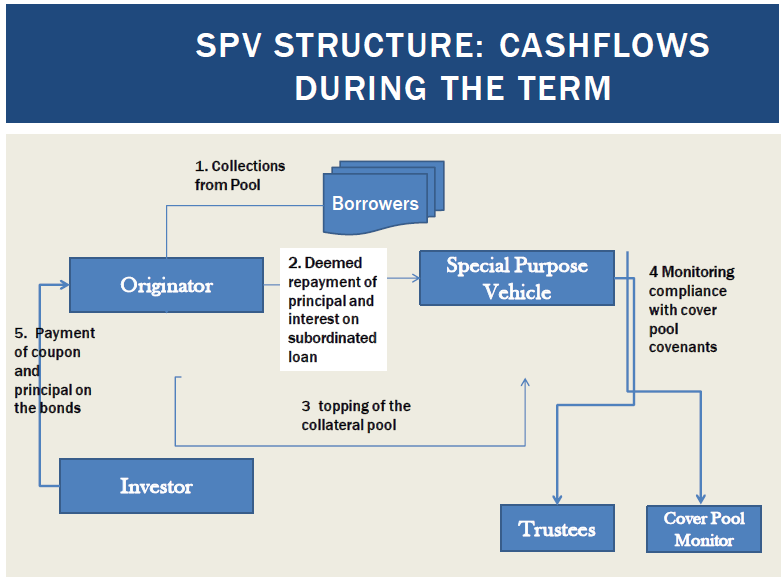

How does this structure increase your comfort?

- The issuing NBFC is responsible for making interest and principal repayments from its cashflows. This is important.

- The bond payments are not made from cashflows from pool of loans (that happens in case of securitization). In the case of covered bonds, the pool of loans is retained on the balance sheet of the issuer (and not transferred to SPV).

- If this issuing NBFC defaults (or in case of a credit event), you still have claim over collateral (which is the pool of loans). Security cover is more than the size of bond issue (say 1.25 or 1.5 times). And the NBFC is required to maintain the security cover by furnishing additional loans if required.

- The cashflows from those underlying pool of loans will flow to the SPV and can be used to pay back the investors. OR you (the debenture trustee) can sell the assets in the pool to recover the money.

- If the pool of loans starts failing, you can sell security for those respective loans to recover money.

- So, you have dual recourse. You can rely on cashflows of NBFCs for repayment. If NBFC fails, you can bank upon those pool of loans to meet the repayment obligation.

- Additionally, there are covenants built into the needs structure which can expedite bond repayment. For instance, in case of a credit downgrade, the repayment gets expedited.

I reproduce another set of charts from VinodKothari.com

What is the problem with Covered Bonds?

#1 You are lending to a low rated NBFC.

The NBFC is responsible for making payments to the borrowers. However, this NBFC won’t be HDFC or Bajaj Finance. They won’t borrow from you at 11% p.a. when they can borrow at much lower rates in the market.

Therefore, the borrowing NBFC will likely be a low-rated NBFC.

For instance, under Wint Gold June 2021, the borrower (Dhanvarsha Finvest Limited) was BBB rated (barely investment grade). Under Wint Bricks May 21, the borrower (Ugro Capital) was rated A.

Will you be comfortable lending to such NBFCs outside of this covered bond structure? Remember, under a covered bond, you are lending to a single NBFC.

Therefore, if this NBFC cannot repay, you have a problem.

But why?

Don’t you have a pool of loans as collateral?

You do.

However, who made these loans? The NBFC itself.

This brings us to another question: Why would the NBFC fail?

Frauds or poor-quality asset book. An NBFC can also fail because of liquidity issues but such issues usually emanate because of the two reasons mentioned earlier.

And your security (pool of loans) is a portion of that asset book. So, if the NBFC is failing because of poor quality loans, how do we trust the quality of this security?

Yes, distributors/arrangers such as Wint Wealth say that they try to select the best loans for that pool. I do not doubt their good intention. I am sure they have done their due diligence but how do we know they got their selection right? We will know this once a borrowing NBFC fails and repayments happen through cashflows from the pool of loans.

Note: I am not saying that no one should lend to low rated NBFCs. Such NBFCs play a vital role in the economy by providing credit to the underbanked. Provide loans to such borrowers who banks and top rated NBFCs won’t touch. Unless such NBFCs can borrow fund themselves, how will they lend to others? However, if you want to invest in covered bonds, you must appreciate the risk.

#2 Security enforcement can be a problem

I must concede my knowledge in this matter is limited.

While there is collateral in the form of a pool of loans, enforcing security is super complicated in our country. Remember the IL&FS case where the cash-generating toll road SPVs were not allowed to make payments to lenders. While I didn’t follow on what happened next, this shows that even SPV structures may not be sacrosanct.

That Covered Bonds have been claimed as “Bankruptcy protected” may not count for much. If bankruptcy protection does not work out as expected, it will be a long-drawn battle to get your money back.

#3 Liquidity

Even though these bonds will be listed in secondary markets, there may not be much liquidity in the secondary market. Therefore, if you want to exit before maturity, you may face issues.

#4 Maturity of pool of loans may be different from Covered Bond Maturity

In Wint Gold June 21, the security pool has loans that are maturing in 2 years, but the covered bond maturity is 15 months.

In Wint Bricks May 21, the security pool even has loans maturing in 2029, but covered bond matures in November 2022.

Wint Wealth believes, in case of NBFC default (or covenant breach), the pool of loans should be able to complete repayment obligation much earlier (since there is over-collateralization).

Ideally, the residual pool maturity should be in line with residual covered bond maturity.

#5 There is Call option (and not put option)

This is important.

In Wint Gold June 21, the covered bond maturity was 24 months, but the website mentioned it was 15 months, didn’t it?

Here is the interesting part.

The Covered Bond (Wint Gold June 21) has an inbuilt call option for the issuer. Call option gives the issuer the right (not obligation) to buy back the bond at a specific price on a specific date.

Now, the Wint Gold covered bond gives the issuing NBFC an option to repay the bond after 15 months. And the exercise price is such that you get an XIRR of 12.25% p.a.

What if the issuer does not exercise the call option?

Nothing much. Such non-exercise won’t be considered default (only a credit event). A default will happen only if the issuer does not pay you back even after 24 months.

However, you can trigger accelerated redemption. i.e., the SPV will direct cashflows from a pool of assets to the bond holders (which is good).

Additionally, if the issuer does not exercise the call option (repay the loan) after 15 months, it will have to pay an interest rate of 14.25% p.a. instead of 12.25% p.a. So, a penalty is imposed on the issuer.

Hence, Wint Wealth’s claim about maturity of 15 months is a bit misleading. The maturity is 24 months. The maturity of 15 months is contingent on the issuer exercising the call option after 15 months.

On the other hand, if the investors or debenture trustee had a put option (force issuer to buy back the bonds) on those bonds, it would have been a different matter.

#6 Each covered bond is different

Each bond will have different terms and conditions, covenants, security etc. If you want to understand, you will have to go through information memorandum of those bonds. These can easily run into hundreds of pages. Difficult to analyze.

An additional concern is that, in this current low interest rate environment, the most conservative investors (low risk appetite) will find these products the most attractive.

Why?

Because these are the investors who have their entire financial holdings in bank fixed deposits and their incomes have been severely affected by low interest rates. These are the investors who want and need higher interest rates. And these investors can get into these risky products without understanding the risk.

The portfolios that have growth investments such as stocks, equity funds in their portfolios would not have felt so much pain because their equity portfolios would have done well (at least over the last year) and hence they will not be much uncomfortable.

Remember there is no free lunch. At a time when 10-year yields are ~6% p.a. (Govt. of India borrows for 10 years at ~6% p.a.), you are lending money to an NBFC at 11% p.a. and your security is a pool of loans at 24% p.a.). The covered bond is a risky investment. You can lose your capital.

How are the Covered Bonds taxed?

The interest income from the covered bonds will be taxed at your marginal tax rate.

Further, the taxation of capital gains will depend on your holding period and whether the bond is listed.

For listed covered bonds

If you sell the bond before completing one year, any capital gains will be taxed at your marginal tax rate. If you hold the bond for over a year, the resulting capital gain, if any, gets taxed at 10%.

For unlisted covered bonds

If you sell the bond before completing 3 years, any capital gains will be taxed at your marginal tax rate. If you hold the bond for over a year, the resulting capital gain, if any, gets taxed at 20% after indexation.

Clearly, you would expect these bonds to be listed.

However, there is still a problem.

These products have usually been targeted at HNIs. Such investors wouldn’t want to pay the tax on interest at the marginal income tax rate.

What to do?

A bit of financial engineering.

Structure the product so that there is no concept of interest income.

In come the market linked debentures (MLDs).

MLDs do not have usual coupon-bearing structure but the pay-out is linked to the performance/movement of a benchmark. The benchmark may have no linkage to the performance of NBFC or the performance of the pool of loans given as collateral.

For instance, in the Wint Wealth Gold-Jun-21 covered market linked debenture, the benchmark was Sensex.

If at the time of bond maturity, Sensex is 80% down from its level on start date, you will get only the principal back. Or else, you will get the promised return (~11.6% p.a.).

So, if Sensex is at 50,000 as on reference date, you are ok if it does not fall below 10,000. Not impossible, but low probability event.

What does this do?

The performance of this bond has nothing to do with the performance of Sensex. However, this changes the taxation of a covered bond (or covered market linked debenture).

No concept of interest. No tax on interest. Since the pay-out is linked to the performance of the benchmark, you cannot consider the unpaid interest as accrued interest either (and be forced to pay taxes). Smart.

If you sell after one year (or if the bond matures after 1 year), the resulting gains will be taxed at 10% without indexation.

If you sell before completing one year, the resulting gains will be taxed at your marginal tax rate.

Note: Please understand I was not able to find supporting clauses in the Income Tax Act. However, I have read about this at multiple places on the internet. Assume this is true.

I am not sure about the tax treatment of payments if accelerated redemption is triggered (non-exercise of call option or any other credit event). For instance, in case of a credit event happening, the pay-out is not linked to the performance of benchmark index. The XIRR goes up to 14.25% p.a. And accelerated redemption gets triggered. As I understand, in such a case, you will get the money as and when the SPV gets the money from pool of loans (and not single payment). However, in such cases, I will be more concerned about return of capital than the post-tax returns.

Should you invest in Covered Bonds?

The covered bonds (covered market linked debentures) provide good returns for a fixed income product. There is credit enhancement through collateral of pool of loans too. There are covenants that can expedite repayment if things are not right for the NBFC. The product is tax efficient.

All good.

However, since the NBFC owns the primary responsibility for bond repayment, I would not be keen to invest unless I can trust the NBFC. So, don’t invest.

Do you still want to invest?

Let us take a detour and understand how you should construct fixed income portfolio.

For your fixed-income portfolio, think in terms of core and satellite portfolios.

Many of us take this approach for our equity portfolios, don’t we?

But what could be core and satellite portfolios in fixed income?

Fixed income investments usually carry the following two major risks.

- Credit risk (that bond issuers defaults on the repayment obligations)

- Duration risk (when Interest rates go up, the bond prices go down and vice-versa. Higher the bond maturity, greater the duration risk)

The core portfolio should control for both credit risk and duration risk. i.e., you invest in good credit quality and shorter maturity bonds (or mutual funds). PPF, EPF, and bank fixed deposits will fall here. Your core portfolio should comprise at least 65-70% of your fixed-income portfolio. Nothing wrong if you have 100% here.

In the satellite portfolio, you relax on one or both the risks. So, you can invest in

- Low credit quality but short duration bonds (or mutual funds). OR

- High credit quality but long duration bonds (or mutual funds) OR

- Low credit quality and long duration bonds (or mutual funds)

Franklin debt mutual funds had (1). We know how that panned out for its investors. While the investors have gotten back a good portion of their money, it could have been much worse.

(2) is fine. Long-term gilt securities fall in this bucket. Yes, you can get the interest rate cycle wrong and that can result in some principal loss, but it is still better than losing your entire money (which can happen in low credit quality bonds). A relatively less risky way to play this theme is to invest in fixed maturity ETFs/index funds like Bharat Bond ETF or fixed maturity gilt index funds.

(3) is the domain of experts. Retail investors better stay away from this.

Covered bonds (or the type arranged by Wint Wealth) would fall in category (1).

If you must invest (despite all the caveats I mentioned), these Covered Bonds (or covered market-linked debentures) can form part of your satellite fixed income portfolio. Do not invest more than 5-10% of your fixed-income portfolio in such products. Appreciate the risks before investing. You can lose money. Note each covered bond is different. Understand the product (issuer, security etc) before investing.

A caveat: I gave similar advice to invest in Franklin Ultra Short Bond Fund to some of my investors. We know how that backfired. With high-risk debt, everything is fine until it isn’t. The same applies to covered bonds.

A word about platforms such as Wint Wealth

I have nothing against platforms like Wint Wealth. In fact, such platforms are doing a good job by bringing such products to retail investors. These structured products have been around for a long time. However, these were available only to HNIs and UHNIs. The ticket sizes were big.

Through these platforms, even you and I can invest in these products, with investment amount as low of Rs 10,000.

If you have the risk appetite for such products, you can consider such bonds as part of your satellite fixed income portfolio. Appreciate the risk and limit exposure.