Pradhan Mantri Vaya Vandana Yojana (PMVVY) was launched in May 2017 to provide a long-term income option for senior citizens in the country. This assumes importance in the wake of the low-interest rate scenario we find ourselves in. Fixed deposits are getting renewed at lower rates. This poses problems to those senior citizens who rely on interest income to meet regular expenses.

LIC came out with a PMVVY product with a guaranteed interest rate of 8% for 10 years.

The PMVVY scheme was extended by the Government multiples times until March 31, 2020. The original PMVVY product expired on March 31, 2020. If you invested on or before March 31, 2020, you would have earned 8% p.a. for 10 years. Now, even though the Government has extended the product until March 31, 2023, it has made important changes to the PMVVY scheme. In this post, let’s find out.

Updates to Pradhan Mantri Vaya Vandana Yojana (May 20, 2020)

The erstwhile PMVVY (with 8% p.a. rate of interest) expired on March 31, 2020. The Government of India has extended the PMVVY scheme until March 31, 2023 with a few changes to interest rates. Govt. Press Release dated May 20, 2020)

Note this change does not affect investors who had invested on or before March 31, 2020. They will get 8% p.a. until the product maturity (10 years).

The change will apply to the new subscribers of PMVVY. If you apply in this financial year (April 1, 2020-March 31, 2021), you will earn 7.4% p.a. And you will earn this interest for the next 10 years.

Do note, even though the Government has extended the scheme until March 21, 2023, the Govt. will decide the interest rate every year (much like it does not small savings schemes every quarter). For FY2021, the interest rate is 7.4% p.a. For the next year, the rate could be different from 7.4% p.a. Thus, investors who invest in FY2022 may earn a different rate of return than 7.4%. Do note, if you invested in PMVVY in FY2021, you will continue to earn 7.4% p.a. for 10 years. Subsequent changes in the interest rate will not affect your returns. It is like a bank fixed deposit or a Senior Citizens Savings Scheme, where you lock-in the rate of interest until product maturity.

Additionally, the Government has specified that the interest rate for PMVVY will be along the lines of SCSS (interest rate of SCSS as on May 21, 2020: 7.4% p.a.). The rate of interest for PMVVY is further capped at 7.75% p.a. This cap will be revisited at regular intervals. Frankly, I don’t understand the need for a cap. As I see, PMVVY is now just like SCSS with 10-year maturity and interest rate lock-in.

The minimum monthly pension is Rs 1,000. The minimum annual pension is Rs 12,000. Owing to the reduction in interest rate (for investments made in FY2021), the minimum investment for a monthly pension of Rs 1,000 has gone up to 162,162 (earlier it was Rs 1.5 lacs). The minimum investment for an annual pension of Rs 12,000 has gone up to Rs 156,658 (earlier it was Rs 1.44 lacs. My calculations show it should be Rs 156,735).

Salient Features of Pradhan Mantri Vaya Vandana Yojana (PMVVY)

- Minimum Entry Age: 60 years (completed)

- Maximum Entry Age: No Limit

- Policy Term: 10 years

- You will be paid pension for 10 years

- You can choose pension payment frequency i.e. monthly, quarterly, half-yearly or annual

- Minimum Pension: Rs 1,000 per month, Rs 3,000 per quarter, Rs 6,000 per half year or Rs 12,000 per year

- Maximum Pension:

Rs 5,000 per month, Rs 15,000 per quarter, Rs 30,000 per half year or Rs 60,000 per yearRs 10,000 per month, Rs 30,000 per quarter, Rs 60,000 per half year or Rs 1.2 lacs per year - Since the interest rate is fixed at

8% p.a.7.4% p.a. now, you can derive the minimum and maximum investment amounts from the minimum and maximum pension levels. You can use monthly compounding to calculate such amounts.The table below contains the minimum and maximum investment at 8% p.a. I have never been able to calculate the exact numbers here (not sure how LIC figures this out. They use different rates of interest for different payment frequency). Will update once LIC releases for 7.4% p.a. Do note, since the interest rate has gone down, you will need to invest a higher amount to get the same level of income.

- The limit on maximum investment is per senior citizen (and not per family). Therefore, if your spouse is also a senior citizen, he/she can invest Rs 15 lacs in PMVVY too. Therefore, the two of you can invest a maximum of Rs 30 lacs in PMVVY scheme. Link to Government Press Release dated May 2, 2018

- The scheme is exempt from Goods and Services Tax (GST).

- With monthly compounding, the effective annual return is 8.3% p.a.

This ceiling of pension is for the entire family. The total amount of pension under this policy to a family cannot exceed the maximum pension limits as mentioned above. The family includes self, spouse, anddependants.The scheme is open till May 3, 2018 March 31, 2020. Quite possible when the scheme is re-launched next year, the interest rate on offer may be quite different.(The previous statement has actually come true) Even though the scheme has been extended to March 31, 2023, the interest rate has been reduced to 7.4% p.a. for investments in FY2021. The interest may change again in FY2022 and FY2023.- The amount of pension is not dependent on age. This is not the case with other pension plans or annuity plans.

- You can take a loan up to 75% of the purchase price after 3 years.

- There is no exclusion on account of suicide. The purchase price will be returned to the nominee even in case of suicide.

You can read about various product features in detail on LIC website.

PMVVY: Pension Payment, Death Benefit and Maturity Benefit

These are along expected lines.

The pension will be paid for a maximum of 10 years as per the payment frequency chosen.

In the event of the death of the policyholder during the policy term of 10 years, the purchase price shall be returned to the beneficiary.

In the event of survival till maturity, the purchase price along with the final pension installment shall be payable.

Premature Exit in PMVVY

The premature exit is allowed only if the pensioner needs money for the treatment of any terminal/critical illness of self or spouse. In case of such surrender, there will be a premature exit penalty of 2%. You will get back 98% of the purchase price.

Tax Benefit for Investment in Pradhan Mantri Vaya Vandana Yojana (PMVVY)

There is no tax benefit for investment in PMVVY.

How is Pension Income taxed?

Such pension income will be taxed at your marginal income tax rate.

There is no tax charged when the purchase price is returned at the time of maturity or death.

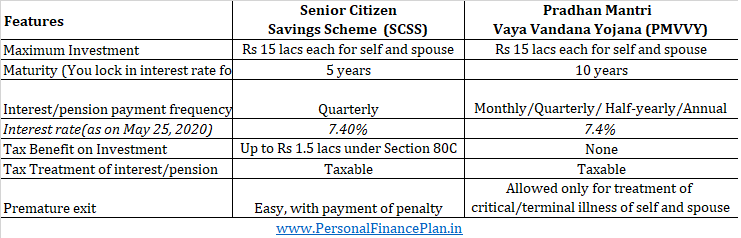

SCSS vs. PMVVY

When I think about PMVVY, one of the existing schemes that deserves attention is Senior Citizen Savings Scheme (SCSS).

PMVVY provides a guaranteed return of 8% for 10 years. For investment made in FY2021 (April 1, 2020 to March 31, 2020), the PMVVY shall offer 7.4% per annum. SCSS provides a slightly higher return at the moment (8.3% p.a.). SCSS is also offering 7.4% p.a. currently (May 25, 2020).

As the Govt. press release dated May 20, 2020, the interest rate of PMVVY will be in line with the interest rate of SCSS. Hence, there is little point in comparing the interest rates of SCSS and PMVVY now. The only difference(with respect to interest rates) will be on the account of interest reset frequency. SCSS interest rate can change every quarter. PMVVY interest rate will change every year.

With SCSS, you can lock in the interest rate for only 5 years. If you want to extend or renew, you will get the prevailing rate. SCSS interest rate is announced by Ministry of Finance every quarter. With PMVYY, you can lock in the interest rate for 10 years.

With SCSS, you get the tax benefit under Section 80C of the Income Tax Act. No tax benefit under PMVVY.

With SCSS, you can invest Rs 15 lacs each in your and your spouse’s name i.e. Rs 30 lacs in total.

On the other hand, with PMVVY, you can invest a maximum of Rs 7.5 lacs for the entire family.

In PMVVY too, you can invest Rs 15 lacs each under your and your spouse’s name. Therefore, as a family, you can invest up to Rs 30 lacs in PMVVY. Of course, both you and your spouse need to be senior citizens.

With SCSS, payment frequency is quarterly. With PMVVY, the payment frequency can even be monthly.

Income from both the schemes will be taxed at your marginal income tax rate.

With SCSS, you can exit (prematurely) quite easily as compared to PMVVY.

In my opinion, SCSS is a better product due to its higher interest rate and better liquidity. However, I can see PMVVY can be more useful in many cases.

Between SCSS and PMVVY, it is difficult to pick one over another. The interest rate is likely to be the same for both the products (albeit with a lag). SCSS provides better flexibility. However, with PMVVY, you can lock-in the rate of interest for the long term.

PersonalFinancePlan Take

Positives of PMVVY

PMVVY is a simple and easy to understand product. You get what you see.

If you compare with a bank fixed deposit, the scheme offers a much better interest rate than a plain vanilla fixed deposit (at the moment).

You can lock in the interest rate for 10 years. Well, this can be a double-edged sword.

Premium (purchase price) does not depend on age. Good for those who are in their 60s. For those in early 60s, the annuity rates, even for without return of purchase price variant, are likely to be lower than PMVVY interest rate.

Hence, it might make sense for such investors to pick up PMVVY in their early 60s. After 10 years, they can consider an annuity plan without return of purchase price to generate a good level of income.

In my opinion, this is a decent option at present for those who want to keep things simple.

Negatives of PMVVY

Do note PMVVY is not an annuity product. Therefore, you do not lock in the interest rate for life. You do it only for 10 years. After 10 years, if the scheme is still on offer, the interest rate offered may be way different than 8% p.a 7.4% p.a..

The investment is capped at Rs 7.5 lacs for the entire family. There is maximum investment limit of Rs 15 lacs per senior citizen. Therefore, the quantum of income from this scheme is capped.

You cannot access money except in case of serious illnesses. There is a facility of loan after 3 years but I wouldn’t go that far. I don’t like to pay to access my own money.

Income is taxable. Effective returns can be low for investors in the highest income tax bracket.

You need to see applicability

For instance, someone who falls in the 30% tax bracket, the effective return is only 5.6% per annum. If this person is willing to take some risk, a Systematic withdrawal plan (SWP) from a good quality debt fund (and not equity fund) may be a good choice (more tax efficient).

Do note SWP can be a bit complex. It is not difficult to select a wrong fund for setting up a SWP. Recently, SBI MF deliberately tried to mislead customers into selecting a wrong fund for setting up a SWP. You need to select the right debt mutual fund for STP.

(Update: May 25, 2020): Debt mutual funds have made investors anxious recently. Hence, you need to consider your risk appetite too before going the STP route from debt mutual funds. If you can appreciate or digest the risk, stick with simpler products such as FDs, PMVVY, RBI Savings Bonds and SCSS.

If you are quite old, say 75 or above, you may get a much better income with an immediate annuity plan.

However, PMVVY may be a good idea for those investors who fall in the lower income tax bracket (and who are in their early 60s) and are looking for a simple product.

Remember that PMVVY is an income product. Do not invest in this product unless you need regular income.

The post was first published on July 26, 2017 and has been updated since.