Mutual Fund Direct plans have been around for over 5 years now.

Under direct plans of mutual fund schemes, you invest directly with the mutual fund house. There is no intermediary or distributor involved. Hence, you save on intermediary costs. This reflects in better returns as compared to regular plans of MF schemes.

Under regular (or distributor) plans, you invest through a distributor or an intermediary. AMC compensates the intermediary on our behalf. Thus cost (expense ratio) is higher for regular plans. Remember you do not pay anything directly. AMC does and that results in higher cost and lower returns.

Everything else (portfolio, fund manager etc) is the same for direct and regular plans.

That direct plan of an MF scheme will provide better returns than the regular plan of the same MF scheme is a known fact. It is a mathematical construct. Nothing can change that. But how much better?

Must Read: Why you should invest in Direct plans of Mutual Fund Schemes?

How have Direct plans fared as compared to Regular plans?

Now that we have data for over 5 years, let’s assess the outperformance of direct plans over regular plans of MF schemes.

I have picked up a few popular funds across categories.

You can see both the plans (direct and regular) started with the same value on January 1, 2013. Over the years, NAV of direct plans has risen faster than NAV of regular plans. This is because direct plans provide better returns than regular plans.

Do note this gap will only continue to widen.

You can also see that the difference in NAV varies across the different types of funds. Looks much higher for equity funds as compared to debt funds.

Do note I have picked just one fund from a category. These funds are not representative of their fund categories. For instance, the difference in return between direct and regular plans need not be the same as ABSL Frontline Equity Fund. It may be higher or lower depending on intermediary compensation or other accounting policies followed by the fund house.

Let’s see what this leads in terms of absolute returns.

You can see the difference between the value of your investments in mutual fund direct and regular plans. As mentioned earlier, this difference will only grow over a period of time.

If you feel this is not a big difference, note this is the difference for only 66 months (5.5 years). You invest in equity mutual funds for a much longer duration.

You can see that the difference is not as high in the case of debt funds.

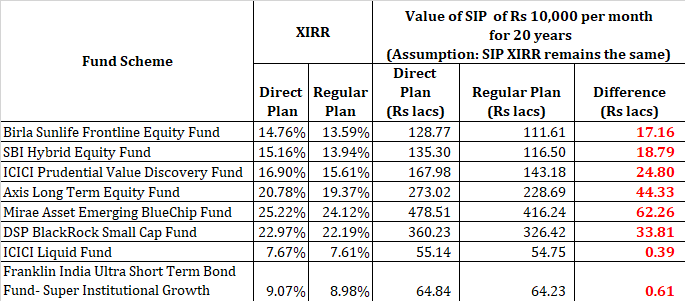

What will be the difference between mutual fund regular and direct plans over the long term, say 20 years?

Nobody can tell with certainty.

If we make an assumption that the difference in returns (XIRR) will be same as has been in the past 5.5 years, then we can try to assess the impact. However, there is no guarantee that the difference in returns will stay as it is. It can be higher or lower.

All you can say is that direct plans will certainly provide better returns than regular plans.

I have considered XIRR for 66 months for direct and regular plans (from MorningStar). I assume the performance (XIRR) of direct and regular will remain the same for the duration of 20 years. I know the assumption is unrealistic but it gives an idea (so, please play along).

If this wouldn’t nudge you to invest in direct plans of MF schemes and switch your existing regular plans investments to direct plans, nothing would.

Depending upon the MF scheme, the difference in corpus over 20 years varies from Rs 61,000 to a massive Rs 62 lacs.

And this is the power of compounding. What looked like a small difference in percentage returns leads to this massive difference in absolute numbers in the long term.

If you were having second thoughts about investing in direct plans, the above numbers will clear out all the confusion.

And the difference could have been bigger. From what I have seen with at least a few AMCs, they charge a transaction fee if you are investing in regular plans. The transaction fee goes to the distributor. For instance, if you are investing Rs 10,000 (lump sum or through SIP), Rs 100 (1%) will go to the distributor and only remaining Rs 9,900 will get invested in regular plans. I have not considered the impact of this Rs 100 in the above numbers.

What should you do?

Simple. Invest in direct plans.

Now, there are many mutual fund direct plan websites. You can register with these websites in a few minutes and start investing in schemes across AMCs.

If you have been investing in regular plans, you can also switch your existing investments in regular plans to direct plans once the exit load period is over (typically 1 year for equity funds) and capital gains taxability becomes benign.

Switch from regular plan to direct plan of an MF scheme is considered redemption from the regular plan and fresh investment in the direct plan. Hence, exit load and capital gains liability may arise on redemption of such units in regular plans. Moreover, your investment is direct plan will be subject to fresh lock-in, if applicable and exit load period

Read: You can get discounts on MF investments too

However, there is a caveat

Direct plans are meant for Do-it-Yourself (DIY) investors. DIY investors have time and skill to research select and review mutual funds on their own. Not just that, they have requisite investment discipline. When it comes to investments, investment discipline is paramount.

If you are a DIY investor, then it is almost criminal to invest in regular plans. So, if you are investing through portals such as ICICIDirect, it is time to move on to direct plans.

Alternatively, you can seek professional advice from a SEBI registered Investment Adviser (RIA) or a fee-only financial planner. Such an advisor can help you select the right funds for you and inculcate investment discipline. Subsequently, you can invest in direct plans.

A SEBI RIA will charge a fee for the service. The fee can be a flat charge or a percentage of your MF portfolio. Try to find an RIA who charges a flat fee (rather than a percentage of your assets). You will pay much less over the long term if you opt for flat fee structure, especially for large portfolios.

On the other hand, if you are not confident about your research skills, your investment discipline is suspect and still do not want to pay the fee, you will do well to stick to a good local distributor and invest in regular plans.

Do not fall for a mere 0.5% to 1% p.a. excess return in direct plans. I concede that a difference of 1% p.a. will compound to a large difference over the long term. However, cost of bad fund selection, portfolio design and poor investment discipline can be much higher.

I have seen portfolios where investors have invested in 40 mutual funds and not more than Rs 10,000 in each of those funds. They feel they are diversifying by investing in 40 mutual fund schemes. A few invest in mid and small-cap funds only. A few think 25-26% p.a. is a given in equity funds. Such investors must seek professional advice.

So, if you are not Do-it-yourself investor, you must decide whether you want to go to a distributor or a SEBI RIA.

Disclosure: I am a SEBI registered Investment Adviser and hence I may have vested interest in asking you to seek services of a SEBI Registered Investment Adviser.