Will you prefer to receive Rs 100 today or Rs 100 five years later?

Will you prefer to receive Rs 10,000 today or receive Rs 100 per month for the next 100 months?

The answer is quite clear to all of us.

Rs 100 today is better than Rs 100 five years later. You can invest Rs 100 at 6% today and end up with Rs 133 five years later.

And you would prefer to receive Rs 10,000 today rather than Rs 100 per month for the next 100 months. The present value of Rs 100 for the next 100 months is much less than Rs 10,000.

Reason: Time Value of money. To put it in another way, time is money.

While almost everyone can understand the simple logic and mathematics behind these answers, we can’t look through the tricks that insurance companies play with us.

How?

Let’s consider traditional life insurance plans.

Under most traditional plans, even though the bonuses are announced every year, these bonuses get paid only at the time of maturity.

I have highlighted many problems with traditional plans in my earlier posts. In this post, I will merely focus on how minor adjustments in timing of cash flows affect your returns.

That’s how a sales pitch for a traditional endowment plan may go like.

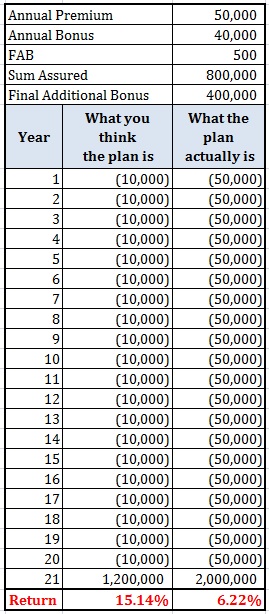

“You pay an annual premium of Rs 50,000 and you get bonus of Rs 40,000 every year (Insurance company is very kind).

At the end of 20 years, you get additional Rs 12 lacs (Sum Assured + Final Additional Bonus). And don’t forget about the life cover. Not just that, you also get tax benefit on the premium amount too. There is life cover of Rs 8 lacs too.

You fall in 30% tax bracket and will save Rs 15,000 worth of tax every year. Maturity amount is exempt from tax.”

Implicit in this approach (you are under the impression) is that you pay a net annual premium of Rs 10,000 per year. You pay Rs 50,000 per year and get a bonus of Rs 40,000.

The product is irresistible.

Do note Insurance companies may follow different nomenclature for bonuses. Moreover, these bonuses are announced (as per Rs 1000 of Sum Assured) every year and can change.

What happens in reality?

In reality, you do not get a bonus (Rs 40,000) every year. This bonus merely gets added to the maturity amount. You do not earn any returns on the amount. Therefore, for 20 years, this amount merely gets added to the maturity amount. You get an additional Rs 8 lacs (20 * 40,000) at maturity.

Let’s see how this simple change affects your returns.

The only difference between these two plans is the timing of payment of annual bonus (simple reversionary bonus). In the first case, we have considered that the bonus is being paid annually while in the other case the bonus gets paid only at maturity.

This leads to a massive difference of 8.92% in returns.

Rs 40,000 wasn’t paid to you every year (What you think the plan is) but was paid only at maturity (what the plan really is). And you know that Rs 40,000 today is not the same as Rs 40,000 20 or 15 years later. Still, you cannot assess the impact on returns.

Under both cases, you are paying a premium of Rs 10 lacs and getting Rs 20 lacs from the insurance company. The difference in return is simply due to the timing of cash flows. And this is the time value of money for you.

It is quite possible that you are aware of low returns in traditional life insurance plans but still purchase such plans because you get peace of mind. Fair enough. It is your choice. And I am no one to comment.

However, if purchased a traditional life insurance plan because you didn’t realize the impact of timing of cash flow on returns, you need to rethink.

The next time somebody asks you to invest some amount X amount and get 2X amount, you always ask “When”. Because the timing of cash flow determines the return you get.

If you invest Rs 1,000 per year for 10 years and get Rs 20,000 at the end of 10 years, you earn a return of 12.3% p.a.

If you invest Rs 1,000 per year for 10 years and get Rs 2,000 every year for the next 10 years, you earn a return of Rs 7.2%

In both cases, you pay Rs 10,000 and get back Rs 20,000. The difference in return is due to timing of cash flow. After all, time is money.

Credit: I read a post on Time Value of Money by Prof. M.Pattabiraman on FreeFinCal and borrowed the idea for writing this post. You can go through the post by Prof. M.Pattabiraman here.