RBI announced a Covid-19 regulatory relief package in the last week of March 2020. Under the package, if your bank permits, you can skip your loan EMIs and credit card payments for the payment due dates falling between March 1, 2020, and May 31, 2020.

After the RBI announcement, many banks have come forward and listed out the process for availing the relief or opting out of it. With a few banks, you can request for a moratorium. With others, the moratorium is the default option and you must request to opt out of it. This Money Control article discusses the process for opting in or out of the moratorium offer for a few banks.

As a borrower, if you can afford to pay the EMIs, should you still opt for moratorium or stay clear of it? Remember, even though you don’t have to pay EMIs, the interest meter keeps running i.e. the interest keeps getting accrued and gets added to the principal outstanding.

In this post, let’s look at the impact of opting for moratorium for loan and credit card payments.

Home Loans, Education Loans, Personal Loans, Auto Loans and other term loans

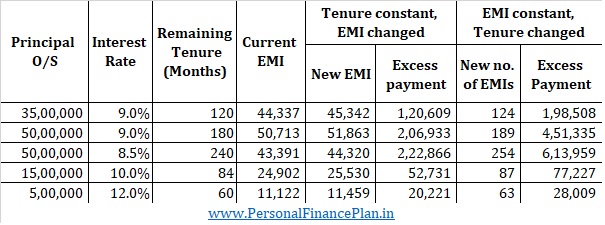

If you opt for EMI moratorium, the interest keeps accruing and gets added to the principal. For instance, let’s say you have an outstanding home loan of Rs 50 lacs at 9% and the remaining loan tenure is 15 years (180 months). EMI is Rs. 50,713

At the end of 3 months, the principal would have grown to Rs 51.13 lacs (due to accrual of interest). Now, you have two options. You can keep the EMI constant and increase the loan tenure. OR you can keep the loan tenure constant and increase the EMI.

If you keep the EMI constant, you will now have to pay 189 EMIs to close the loan i.e. you will have to pay Rs 4.5 lacs more to close the loan.

If you keep the loan tenure constant, your EMI will increase to Rs. 51,863, an increase of Rs 1,150. You will have to pay Rs 2.06 lacs to repay the loan.

I discuss various permutations and conditions in the following two tabulations. Note that these calculations consider moratorium for 3 months.

You can see, by not paying EMIs for these 3 months, you will have to pay many more EMIs later. The excess payment can run into lacs of rupees.

Do note the cost of the loan does not change simply because you avail the moratorium. It remains at 8.5% or 9%. The absolute pay-out, however, increases if you do not pay the EMIs for the 3 months.

Credit Card Payments

For the credit cards, if you avail the moratorium, you will face the following problems.

- The interest cost is very high. It can range from 3% to 3.5% per month. Annualized rate is over 40% p.a.

- You lose the benefit of interest-free credit period. You will be charged interest on the fresh purchases from Day 1. Even for the existing purchases (but not paid), you will be charged the interest from the date of purchase.

- Heavy late fee and penalty. RBI package is silent on this. Even though I believe late fee and penalty shouldn’t apply, it is better to clarify with your bank.

- 18% GST on all the above. Yes, on credit cards, you pay GST even on the interest.

Let’s say you have Rs 75,000 outstanding on your credit card. If you avail the moratorium and do not pay for 3 months, the outstanding amount will grow to Rs 83,206. That is a lot of extra payment.

What should you do?

As is evident from the illustrations above, you should not opt for moratorium if you can afford to pay.

I understand this lockdown does not affect everyone in the same manner. For some, nothing changes financially except that they must work from home. It is a temporary issue, and everything goes back to normal when the lockdown is lifted. For these borrowers, it does not make sense to avail moratorium. Keep the EMI and card payments regular.

For the others, this lockdown may mean a drop or even total stoppage in income (think about hospitality sector). The employment and income prospects may have dipped. For such people, the after-effects of the lockdown won’t go away so soon. For these borrowers, despite the mathematical argument against availing moratorium, opting for the relief may make sense. There is quite a bit of uncertainty on the income front. Skipping EMIs might give that breathing space. I trust your judgement.

From the financial planning perspective, it is during such times that a robust emergency fund would have helped. If needed, you could have simply accessed those funds to make the payments. If you don’t have a few months of expenses in an emergency fund, this is a wake-up call. For the more cavalier among us, an emergency fund may be a waste of time and money. It is an unnecessary drag on returns. However, it is during times such as these you will appreciate the value it brings to the table. It is never too late.