I do not like traditional life insurance plans and always advise readers to stay away from such plans. Traditional life insurance plans provide low life coverage and poor returns.

But what about those who have already purchased such a plan? Should such policyholders surrender the plan? Well, not always.

If you have already purchased the plan, surrender of the policy may not always be a prudent choice. The reasons include front loaded commissions and heavy surrender penalty.

If you work out the numbers, it may actually make a lot of sense to let the plan run its full course if you have paid premium for a few years. The outcome will depend on the plan features, surrender value, number of years of premium paid and the policy term. So, do not jump to any conclusion. Do some maths and make a decision subsequently.

The rationale is that the surrender value and the future premiums should yield much better results than the expected maturity value of the insurance plan. For instance, if you need to earn 14% return on surrender value and future premiums just to match expected maturity value of the insurance plan, it may actually make sense to continue. If the required return is only 6%, it is better to surrender the plan. Go through the following post for more on this.

Must read: Surrender, continue or paid up: What should you do?

If you have decided to continue the plan, you will do well to be aware of a fringe benefit that traditional insurance plans can provide.

Are you aware that you can take loan against your LIC policy?

In this post, I will discuss loans against LIC policies, eligibility, repayment structure or whether it makes sense to opt for such loans.

I pick up LIC New Jeevan Anand, a very popular participating non-linked endowment plan from LIC. The term and conditions will be similar for other plans too. The analysis in this post will be based on LIC New Jeevan Anand.

Must Read: Stay away from LIC New Jeevan Anand

How much can I borrow against my LIC plan?

You can borrow up to 90% of the Surrender Value of the plan (85% in case of paid up policies) as on date of application.

You can make an application for loan only once you have paid premium for three years.

It goes without saying that you can take a loan only once your policy acquires surrender value. Typically, LIC plans acquire surrender value only after 3 years.

You have to assign the policy to LIC as security.

How is the loan repaid? What is the loan tenure?

You get a lot of flexibility.

You have to pay interest every six months.

About the principal, you can repay the loan till maturity of the policy.

You just need to keep making the interest payments on time and you won’t hear from LIC about principal repayment.

Alternatively, if you wish, you can also repay principal along with interest.

In fact, if you do not repay principal even till maturity/death, LIC will automatically square off the outstanding loan amount against maturity/death benefit and pay the balance to you/ your nominee.

You borrow for a minimum of six months (minimum tenor). Even if you want to foreclose the loan before six months, you will have to pay interest for at least six months.

Book Suggestion: How to Retire Rich: Invest Rs 40 a day? (P V Subramanyam)

What is the applicable interest rate?

The interest rate is declared by LIC and may vary according to the insurance plan. You can enquire about the prevailing interest rate from the LIC.

As I understand, the prevailing rate of interest is 10.5% per annum.

Book Suggestion:How to Retire Rich: Invest Rs 40 a day? (P V Subramanyam). Hindi version is available too.

What If I default on my interest payment?

If you do not pay interest amount within 30 days from the due date, LIC reserves the right to foreclose the policy and settle the loan amount against the proceeds.

Illustration

If you are planning to borrow against your LIC policy, you need to find the current Surrender Value of the plan. Surrender value will determine your loan eligibility.

How to find the Surrender Value?

Well, you can simply call your agent or walk in to the nearest LIC branch to find out the Surrender Value. You do not have to go through the following exercise.

In this post, I will try to assess the Surrender Value for the particular scenario for LIC New Jeevan Anand. I do not guarantee that the value is accurate. But it will give an idea about how loan eligibility is calculated.

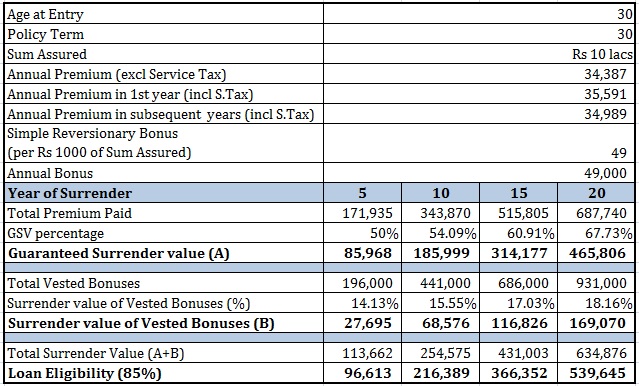

Let’s say you purchased LIC New Jeevan Anand 15 years back (by the way, the plan didn’t exist at the time) when you were 30. The Sum Assured is Rs 10 lacs and the policy term is 30 years. You have paid premium for 15 years.

The annual premium is Rs 34,387 (before Service Tax). For the first year, the premium will be Rs 35,590 (including service tax of 3.5%). For the subsequent years, the annual premium will be Rs. 34,988 (including service tax of 1.75%).

For LIC New Jeevan Anand, Surrender Value is the sum of

Guaranteed Surrender Value of Premiums paid (GSV)

And

Surrender Value of Vested Reversionary Bonuses (SVV)

There is also provision for the payment of Special Surrender Value, if it is more beneficial to the policy holder. However, I will ignore special surrender value for the purpose of this exercise. In any case, you don’t have to calculate this value on your own since it is readily available with your agent or at the nearest LIC branch.

Guaranteed Surrender Value is the percentage of total premiums paid till date excluding any tax or rider premiums. The percentage is a function of policy term and number of years of premium paid. The tabulation is provided in the policy document.

For instance, if you surrender the policy after 15 years, the applicable percentage is 70% for a policy term of 20 years and 60.91% for policy term of 30 years.

Guaranteed Surrender Value

= No. of years of premium paid * Annual Premium before Service tax * GSV percentage

=15 * 34,387 * 60.91% = Rs 3.14 lacs

Surrender value of vested reversionary bonuses is calculated in the same manner. You have a separate tabulation for applicable percentage in the policy document.

Let’s assume LIC announced Simple Reversionary bonus of Rs 49 per thousand of Sum Assured for each of those 15 years. Your annual bonus will be Rs 49,000.

You will have received 14 annual bonuses. Total Simple Reversionary bonus = Rs 49,000 * 14 = Rs 6.86 lacs.

Surrender percentage after paying 15 premiums in 30 year policy is 17.03%.

Surrender value of vested bonuses = 17.03% * 6.86 lacs = Rs 1.17 lacs

Surrender value of the policy = Rs 3.14 lacs + 1.17 lacs = Rs 4.31 lacs

Loan Eligibility = 85% * Rs 4.31 lacs = Rs 3.66 lacs

I have calculated the loan eligibility for the same plan in different years.

You can see loan eligibility grows as your policy grows older.

What are the benefits of loans against LIC policies?

- Quick disbursal. It is your money. You can expect the loan disbursement to be swift.

- Not much documentation required. Only the policy to be assigned to LIC. No additional security.

- At interest rate of 10.5% per annum, it is much cheaper than personal loans.

- You get a lot of flexibility. There is no EMI like repayment schedule. You can repay the principal and when you want. Can be very useful when you are facing cash flow pressure.

What are the drawbacks?

Since loan amount is linked to surrender value, you cannot expect to take a high value loan against the policy. You can see even after paying premium for 20 years, the loan eligibility is only 5.39 lacs (in the example discussed above).

There is no tax benefit for repayment of loan against LIC policy.

Points to Note

- Loans are offered against traditional life insurance plans only.

- Financial institutions other than LIC also offer loans against LIC policies. However, the rate of interest is typically higher than the rate charged by LIC. Can’t see why anyone would do that when LIC offers at a lower rate.

- Even though I have calculated surrender value many times in this post, you do NOT have to surrender the plan to take the loan. You merely need to find the surrender value. If you surrender the plan, you won’t get any loan.

- You can also request a second loan against the same policy while first loan has not been repaid. The cap of 90% of Surrender value shall apply to the combined amount.

How to apply for loan against LIC policy?

You need to submit Form 5196 to your agent or the nearest LIC branch to take out a fresh loan. For a follow-up loan (second loan), you need to submit Form 5205.

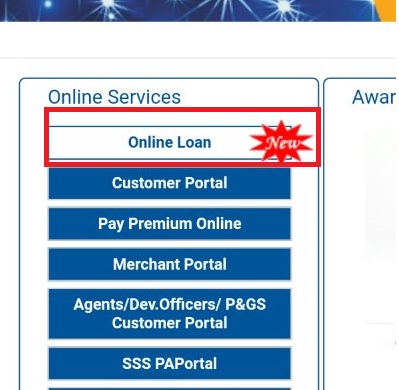

Now, you can apply for Loan from LIC and even make loan payments online

Do note that the loan application can only be initiated online. It cannot be completed online. There is an offline step involved.

You need to do is to register on LIC website. To register, you will need a few pieces of information such as your LIC Policy Number and a few personal details. You can go to the following link (https://licindia.in/Home-(1)/LICOnlineServicePortal) and click on “New User”.

Once you have registered, you need to login by clicking on “Registered User”.

However, your job is not yet done. Once you log in, you need to subscribe for “LIC Premier Services”. You can apply for a loan against your LIC policy only once you are a Registered LIC Premier Services User.

To register as Premier User, you need to download an auto-generated form, take a print-out, sign the form and upload on the LIC site.

Hopefully, within a few days or weeks, your request for Premier Services Registration will be approved. Subsequently, you can apply for a loan online through the LIC portal.

Do note the link to Apply for loan online is available on the home page too. (https://www.licindia.in/). You can click on that link too. However, you will still need to log in (after registering) into LIC portal and be a “Registered Premier Services User” before you apply for the loan.

A few screenshots of how to apply for Loan against LIC policy online

Link on the loan Page on LIC Home page or directly click on the following link (https://www.licindia.in/home/policyloanoptions)

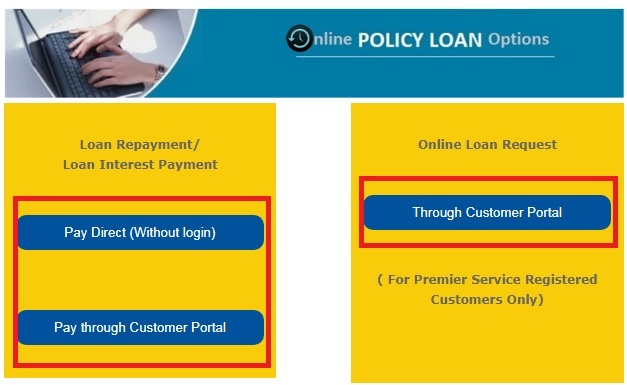

You can apply for the loan online. You can make loan repayment or interest payment online too.  To apply for the loan online, you need to log into customer portal.

To apply for the loan online, you need to log into customer portal.

Once you have logged in, you need to register for LIC Premier Services. Alternatively, you can click on Service Registration–>Service Request–>Premier Services Registration to complete the process.

To register for premier services, you need to follow a 3-step process. You need to download an auto-generated form, print, sign, scan and upload on the portal.

Once your registration for LIC Premier Services is accepted, you can apply for loan online by clicking Service Registration–>Service Request–>Online Loan Request.

Once you have completed this step, you need to submit the following documents at the nearest branch (and not your base branch).

- Printed and signed Loan application form

- Policy Document

- NEFT Mandate form (for loan disbursal)

You need to submit these documents within 4 days of making the online application. If you fail to do so, your application will be automatically rejected and you will have to apply again.

You can track the status of your loan application or your application for Premier Services Registration under Registration–>Service Request–>Request Status.

PersonalFinancePlan Take

Traditional life insurance plans are poor products. However, if you are trapped in one, loan against the policy is one feature you can explore if you are looking for low cost debt.

Loan against LIC policy can be a cheaper alternative to personal loans.

Do note interest rate is important. 10.5% may be okay. However, if you get a loan at 13-14%, it may be prudent to actually surrender the plan and use the proceeds for your requirement rather than taking out a loan against the same LIC policy.

88 thoughts on “All you need to know about Loan against LIC policy”

Hi,

I paid all the 5 installments of ICICI PRULIFE PINNACLE SUPER LP. Policy term is 10 years.Should I keep this policy or surrender it?

Hi Srinivas,

I will have to go through the plan for the same. Can’t comment beyond a point without going through the plan.

It is a ULIP. A lot depends on the funds you chose.

Not much issue even if you continue.

Hi Deepesh,

After 5 years, the absolute return is 13%. I opted for 20%-40%-40% for highest NAV fund B, dynamic P/E fund and Multicap growth fund a year back. Before that it was 100% under highest NAV fund.5 years are completed now.All premiums are paid. policy Tenure is 10 years. Also, I am planning to buy a term policy, sum assured between 1 crore – 3 crores.Keeping all the above mentioned in view, how do you look at it?

Regards,

You can take out the money then and invest in mutual funds. Assume there is no surrender penalty.

Yes, bridge the insurance deficit by purchasing a term plan.

sir can I pay interest amount through check, and what are the possible ways to pay out the interest amount online?

Dear Isha,

Please check with your agent/branch.

sir I’m not a lic policy holder but I want a personal loan from lic should it will be possible

I doubt LIC offers personal loans to non-customers. Please approach a LIC branch.

Hi,

Does LIC send a letter once the loan against LIC policy is disbursed? or I have to check online?

Disbursal will happen through either through cheque or NEFT.

Please check with LIC branch for such operational details.

I want to surrender my 2 years old New Jeevan Anand policy! My sum assured is 15 lakh, tenure 25 years and I pay monthly 5300 rupees premium for this!

If I surrender after 3 years how much will I get? I understand that it’s 30% of the premium paid so far if surrendered after 3 years, I am not sure. Also, will I get Surrender Value of Vested Reversionary Bonuses (SVV)? Note that it has been 2 years since policy and to complete 3 years I have to pay 12 more installments.

Which would be beneficial; surrender now or after one more year? If I surrender now I won’t get anything.

The best thing what i can say is…Don’t think of surrendering the policy. It is one of the Best Policy. If u can pay for one more year , u just continue ur premiums and after 3 years u just apply loan and start paying interest along every 6 months.

If u have already made up ur mind to surrender, then i shall advice u to leave the policy as such than paying it for 1 more year, which would result in lesser returns.

Regards

Mithun R G ( LIC Advisor)

(mithunrg_born2win@yahoo.co.in)

I have my LIC and paying for last 2years can I tacke alone against it

You can do that once your policy acquires paid up status.

Typically, it is 3 years.

Can i get loan second time against same policy???

Yes. The cap on the loan amount will still apply.

Please check with your agent or local branch.

What things are required to apply a loan.

Please constant your LIC agent or your nearest LIC branch.

Do i need to go same branch to take the loan as it is mentioned in Policy?

Contact the nearest branch.

Can a policy holder avail a second loan on a policy ( of course subject to 90% of SV) before the earlier loan is fully repaid?

I think so. Please talk to your agent or contact your nearest LIC branch.

Sir, I have a Jeevan Tarang policy of SA for 20lakhs for 20yrs term. I completed 6 yrs and now paying 7th yr premium. Got the below info from LIC branch:

Total premium paid = 6,25,000

Total vested bonus = 6,00,000(approx)

Surrender value = 4 lakhs plus(approx)

Loan eligibility = 7 lakhs.

If i opt to take this loan of 7 lakhs and decided not to pay it back and discontinue the premiums, will there be any problem?

Yes, there will be a problem.

Loans are meant to be repaid.

Thanks for the prompt reply. But i got this suggestion of taking loan and not paying back from the LIC agent. He told me that since loan is taken from the policy value 12 lakhs (6.25 lakhs premium paid+ 6 lakhs bonus), if the loan is not paid back the policy will be closed and hence there won’t be any problem. And i’ll be benefited through this option since the surrender value is less than the paid premium.

Appreciate if you could tell, what kind of problems this option(loan taken not payed back) will lead to.

If your LIC agent has said this, you should first stop working with that LIC agent.

Perfect Response sir

Hello Sir,

we have paid lic loan of Rs. 1,28,000/- just now

I just want to know, is its interest part or loan repayment part is tax deductible .?

Please suggest..

Hi Pooja,

No tax benefit for repaying such loan.

I have taken money back lic policy in 2007. Paying premium of 32400 per annum(opted quarterly payment). Every 5years I can withdraw the money and I did so in 2012. Now this year I might get some money which I can with draw only in November 2017. Now I need urgent 2lakhs is possible i can take inadvance whatever money am eligible or should I go for loan? Please suggest?

Hi , I have taken ICICI prudential life insurance policy , The minimum lock in period is 5 yers. I paid 3 annual premiums. The NAV is less than what ever I paid. I am paying Rs. 1.00 lacs p.a . Till date I paid 3.00 lacs. But the NAV is less than 3.00 lacs. Is is wise to continue the the payment????

Hi Vijay,

Can’t comment without knowing more about you, your policy and the fund choices. As I understand, it is a ULIP.

ULIP provide market linked returns. Therefore, scenario as mentioned by you can happen.

Sir can I apply for a loan against my policy from any branch in an state.

Not sure. You can check with your agent.

Sir how can I apply for lic loan

Hi Nikhil,

Please contact your LIC agent or the nearest LIC branch.

can loan be taken against market linked plans.

I doubt that. Some insurance companies or NBFCs may offer.

LIC,

What amount of interest I have to pay if I want to settle principal from claim amount ?

No extra interest, regular interest rate for your loan

Hello Sir,

I have Jeevan Anand policy with paying yearly 42K and till now i have paid 9 times. I would plan to take loan for this policy so how much i will get OR if i surrender the policy how much i will get.

If i take loan how to pay the amount.

SA is 600000

Kindly suggest me.

Thank you for your kind help.

Srinivas

Hi Srinivas,

Please talk to your agent. He/she will help you with more accurate numbers.

Sir, During my policy period, I have taken housing loan from LICHFL against my policy document. Now, My policy came for maturity. I have submitted my maturity form to my home branch. They asked endorsement against my home loan. What form to be submitted to them ?

Please talk to your LIC agent.

Can I pay loan interest only by partly of Lic policy

Can I pay loan interest by partly only of LIC policy

Atleast the interest has to be paid in full.

Sir I want to know best single premium plans and when can I avail loan on this single premium policy

Strange. Why do you want to purchase a single premium plan and taken loan on it?

Simply use the funds for the purpose for which you want to take the loan.

Can I pay the interest of my loan against lic policy in any of the branches or should it be paid only in the branch from where the loan is issued.

Please check with the agent or the nearest branch.

If I take loan against my traditional LIC policies which had bonus accrual option, is it so that bonus accrual is stopped because I realise that my accrued bonus amount has stayed the same ever since I took the loan in Feb, 2016. My LIC Agent is clueless and not able to answer.

Why would bonus stop if you take a loan?

Loan does not affect policy payouts.

Hi Deepesh Sir,

I have followed the steps and completed the Premier Services Registration. And surprise! they validated it in 1 day!!

I have Jeevan Shree (Plan-112) and Sum Assured is Rs. 5,00,000 and Policy Status is “Fully Paid-Up”. The premium was Rs. 24472 and payable for 16 years starting from Feb-2002 and ending in Feb-2017. Date of maturity is in Feb-2017.

The problem now is the loan amount is appearing to be Rs. 0.0. And LIC website says that policy is not eligible for loan. Can you please see why this is so?

Thanks in advance for your reply!

— Anurag

Correction: Date of maturity is Feb-2027

Hi Anurag,

Difficult for me to comment.

For all you know, this could be a technical glitch.

Contact LIC if you are facing problems.

I assume your policy is eligible for loan.

Dear Sir,

I need a loan against my LIC policy,but i am not clear how loan EMI is paid.. means it will adjusted in Policy premium amount or i have to pay EMI additional to my LIC Premium ?

Please help !!

Dear Rajiv,

Yes, you have to pay additional amount.

If I take loan on a policy then later can I make it paid up?

I don’t see a problem. Will have to check if you can do that during the term of the loan. If you don’t pay premium, the policy automatically becomes paid up.

sir ,I have requested to grant a loan but the request is taken and when I went to track the loan status it shows that no request has taken but on my email a message has came of confirmation that the request has received with the request Id***************.Now, I’m confused that my loan is requested or not And if not what to do now because when I went again to apply for loan a notification came of not eligible.And if yes how can I track that.

Hi Ankur,

To be honest, difficult for me to comment.

I have never applied for LIC loan. Therefore, I do not have operational knowledge.

In my opinion, since you got an e-mail, something should have gone through.

Suggest you try their phone helpline.

thanks sir for your opinion

That is a technica glitch i think. i did the same and the status is missing. I am approaching my home branch today to submit my documents. lets see what happens there.

PS: Submit the policy to your HOME LIC Office only.. otherwise there is wide spread confusion even amongst LIC employees too on this ONLINE systems even after all this time..

Thanks Nish for your inputs.

Really appreciate your input.

Hello, Sir how much time it will take to get loan amount after applying for the loan ..?

What is the best policy for my daughter in LIC ?

I am a middle class family man, I have 3 years old daughter.

Dear Babu

Can’t comment about the time it takes to get the loan amount in your account. Suggest you talk to the nearest/home LIC branch.

Your daughter does not need life insurance. You do.

I suggest you purchase pure term insurance plan for yourself. You can purchase from LIC too.

For your daughter, suggest you look at PPF and Sukanya Samriddhi Scheme.

IF you can take some risk, you can invest some portion in equity mutual funds too for her education.

I have taken lic endowment policy for 10 years am\nd yearly premium is Rs.5000/-. I have paid the premium for 7 years without any default. During the 8th year I have borrowed a loan of Rs,27000/- and after that I am not in a position to repay the premium as well as interest for loan. In this situation if I am foreclosure the policy how much amount I will get? Pl. comment

LIC will give you back the money only after squaring off the principal and interest amount.

Please contact the branch in this case.

I have jeewan saral policy from april 2010. I have paying 12250 quterly. What is death amount, maturity amt, loan amt, surrender amt. My present age is 32 years. Is a real for this policy known for death policy or also benefit for maturity. May i close or not this policy

Continue the plan.

Sir,

I have a jeevan anand policy paying 20K annually. I have paid 10 times. How much loan I can get, What is the process of availing online. In how much time I can get the loan amount in my account.

Ashish,

The details and the process are provided in the post.

For the exact loan amount, please contact your agent or the LIC branch. It is 90% of the surrender value. Therefore, unlikely you will get loan for more than 1.25-1.75 lacs.

I have not tried the process myself. Not sure of the turnaround time.

Hi Sir,

I lost original bond..

What I need to do?

It is required one?

Please contact your LIC branch.

I am paying premium for the past 15 years and now I am planning to avail 40000/- loan from LIC but at the same time i am not interested to repay the loan now I have the following doubts to be clarified

1) Is that Mandatory that i have to repay the loan

2) I came to know that interest alone has to be paid on a half yearly basis if not the interest will be compounded

3) If I dont pay the loan amount of 40000/- is there any provision that they can deduct the same from the maturity value and pay back the balance ex: my maturity value is 175000/- (175000-40000=135000/-) will they credit 135000/- to my account or is there any other hidden charges i have to pay

can you just clarify on the above

Any loan that you take has to be repaid. If you don’t repay, the amount will be squared off from your maturity proceeds.

If you pay interest regularly, there can be no compounding.

Hi Deepesh Raghaw sir Iam Sam I have one doubt I applied online loan the application says please submit all required documents at any near branch but my problem is the Lic policy belongs to my mom and she was in mnj cancer hospital how can I take her into a Lic branch. In this case can I go to submit the forms in Lic office is that sufficient r any process there. Definitely my mom didn’t come Bcz she in hospital how can go further process is the candiat mandatory ans me sir

Hi Sam,

I understand your concern.

I am not very sure about this. Believe you can give it a try (visit the home branch with documents).

You can get the documents signed by your mother and see if it helps.

Sir after applying for loan online on my lic policy

Is payment is account transfer or by check

I have not applied.

But, I believe you will get an option to specify how you want the money.

Hi sir,

I wanna know that if I take loan on my lic policy of which I m paying premium since 8 to 9 years and then I don’t pay interest as well as other premium then what will happen to my policy..

LIC will foreclose your policy and recover funds.

please sir tell me

sir mein 1000 rupai per month deta hoon lic mein

aur meri money back policy hai

5 years complete ho gaye hai policy ko

first money back bhi aa gaya hai 30000

agar mein money back lene ka baad loan leta hoon to kitna amount mil jayega

Hi

I have applied for loan against my LIC policy

How many days it will take to disbursement ??

Hi Im 59 years old and purchased lic old jeevan anand policy in 2008 for ppt of 30 years and paying premium for last 12 years. should i surrender the policy or leave it as paid up policy or continue paying premium till maturity. what is your suggestion as term plan at this age are very costly.

sir mein 1000 rupai per month deta hoon lic mein

aur meri money back policy hai

5 years complete ho gaye hai policy ko

first money back bhi aa gaya hai 30000

agar mein money back lene ka baad loan leta hoon to kitna amount mil jayega

Does it affect CIBIL if loan on LIC policy is not repaid and LIC adjusts it?