The Finance Minister made a few favourable announcements for home loan borrowers in the Union Budget, 2016. In this post, I will discuss the two changes in detail and how these changes affect home loan borrowers.

First proposal was to provide an additional tax deduction of Rs 50,000 for interest payment on housing loan under Section 80EE. Second proposal was to increase in time-period for construction/acquisition of property for claiming interest deduction under Section 24.

Both the changes will be applicable for Assessment year 2017-18 and subsequent years.

Let’s look at the changes in detail.

Must Read: Union Budget 2016: Key Takeaways

1. Additional benefit of Rs 50,000 towards interest payment under Section 80EE

However, there are a few pre-conditions to be met before you avail this tax benefit under Section 80EE.

- The loan must be sanctioned between April 1, 2016 and March 31, 2017.

- The loan amount sanctioned for acquisition of residential property shall not exceed Rs 35 lacs.

- The value of residential property shall not exceed Rs 50 lacs.

- The tax-payer must not own any residential property on the date of sanction of loan.

Clearly, the benefit is only for first time home buyers. Given the restriction on loan amount and value of residential property, you may not be able to take benefit if you reside in bigger cities. The cost of residential property in such places is likely to exceed Rs 50 lacs.

As I understand, only the sanction needs to happen between April 1, 2016 and March 31, 2017. Even disbursements after March 31, 2017 (for the loan sanctioned between April 1, 2016 and March 31, 2017) will be eligible for this benefit.

Points to Note

- This tax benefit under Section 80EE is over and above tax benefit of up to Rs 2 lacs towards interest payment for a self-occupied property.

- The benefit shall be available for AY 2017-18 and subsequent years.

- The benefit shall be utilized by self-occupied properties only. In case of let-out properties, entire interest amount is already eligible for deduction.

How does this affect cost of your loan?

This could result in additional cost saving of up to Rs 15,450 per financial year for borrower in 30% tax bracket.

The exact nature of benefit depends on multiple factors including loan amount, tenor, interest rate and your marginal income tax rate.

The impact will greater for larger loan amount as you pay higher interest amount.

Let’s consider an example.

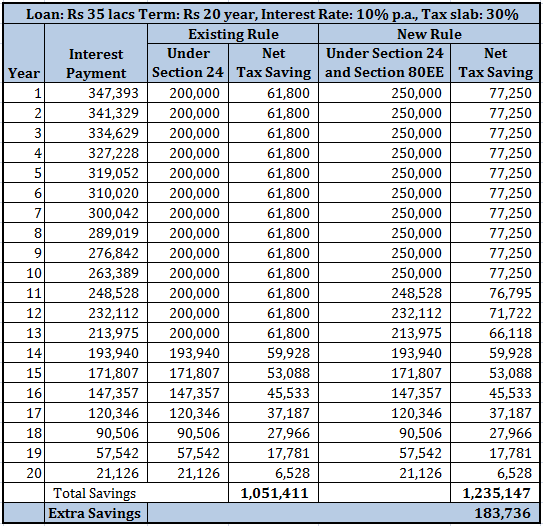

- Loan Amount Rs 20 lacs, Tenor 20 years, Interest Rate 10% p.a.

- Loan Amount Rs 35 lacs, Tenor 20 years, Interest Rate 10% p.a.

Assumptions:

You do not take any benefit for Principal Repayment under Section 80C. Your EPF, life insurance premium payments, tuition fees etc utilize the entire limit.

Interest rate remains constant during the term of the loan.

In case of Rs 20 lac loan, there is no benefit because you won’t pay more than Rs 2 lacs of interest in any year during the loan repayment term. Hence, you won’t be able to utilize this additional tax benefit of Rs 50,000 under Section 80EE.

In case of Rs 35 lacs loan, this will result to net savings of Rs 1.83 lacs over 20 years for borrower in 30% tax bracket.

If you are in 20% tax bracket, your savings will be Rs 1.22 lacs over 20 years.

If you are in 10% tax bracket, you savings will be Rs 61,245 lacs over 20 years.

You can see major portion of excess tax savings will come in the initial years when you pay more interest.

Must Read: Tax Benefits on Home Loan Repayment

2. For maximum tax benefit, you must get possession of house within 5 years

For you to get maximum benefit of Rs 2 lacs for interest payment for home loan (taken for self-occupied property) under Section 24, the construction/acquisition of the residential property must be completed within 5 years (changed from 3 years in Finance Act, 2016) from the end of financial year in which the loan was taken.

Otherwise, the tax benefit gets capped at Rs 30,000 per financial year.

This change from 3 years to 5 years brings relief to many home buyers.

Many reasons due to which the projects get stalled or possession gets delayed are beyond their control. Not only such buyers had to pay rent and EMI at the same time, they got lesser tax benefits too.

This change is applicable for existing projects too.

Though these changes do not take care of high real estate prices and construction delays by builders, these can at least ease some burden on your pocket.

2 thoughts on “Benefits for Home Loan Borrowers introduced in the Union Budget 2016”

sir, you are very good in content writing easy explained .the best thing is you give example/case.

Thanks Ashwani!!! Please do share with friends and family.