You visit an electronics store to purchase your favorite gadget. At the time of payment, you notice an EMI offer at 4% rate of interest. You need to pay EMI for 12 months.

You get interested. After all, you can easily get an interest of 6-7% on a bank fixed deposit. You feel you might end up earning on the entire deal.

Even though you have savings to easily finance this purchase, you find the offer quite attractive.

Before you jump to take this offer, do you really think any financial institution will offer you loan at 4%? How will they make money? Let’s find out more about the offer.

The offer goes like this:

You pay a processing fee (or the processing fee is adjusted with the loan amount). The loan amount is net of first EMI. You pay EMIs for the next few months.

Come on, no financial institution will offer you loan at 4%.

If you work out the actual cost, it will come to 11.25% p.a. (assuming a processing fee of 1%). Well, the devil is in the detail.

If you had been told that the cost of loan is 11.25%, would you have gone for the loan? Unlikely, especially if you have the money.

Let’s see how this happens.

Why this difference in Advertised Cost and Actual Cost?

It is due to timing of payment.

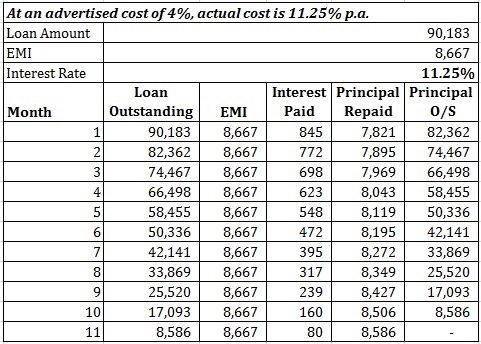

Let’s consider example of purchase of Rs 1 lacs and an advertised interest rate of 4% p.a.

For a purchase of Rs 1 lac, you will have to pay a total of Rs 1.04 lacs.

Well, the cost would have been 4% if the amount had to be paid at the end of the year. But that’s not how it is.

You have to pay in EMIs of Rs. 8,667 (Rs 1.04 lacs/12) and not in lump sum towards the end of the year.

First EMI is to be adjusted at the time of purchase itself. Hence, effectively the loan amount is only Rs 91,333 (Rs. 1 lac – Rs. 8,667). You have to pay back Rs 95,333 (Rs 1.04 lacs – Rs 8,667).

And don’t forget the processing fee and the associated service tax. If the processing fee is 1%, you will have to pay an additional 1,150 (including service tax).

Effective loan amount from your perspective becomes Rs 91,333 – Rs 1,150 = Rs. 90,183.

You may argue that the service tax does not go to the lender/NBFC. However, from the perspective of the buyer, service tax is a cost.

So, you pay Rs 95,333 (11 EMIs of Rs 8,667) on a loan of Rs 90,183. That’s an interest cost of 5.7% p.a.

But, is that the real cost?

What about the timing of payment?

You are not paying the amount of the end of the year. You are paying it at the end of every month for 11 months.

As you know, in case of reducing balance payment, portion of EMI goes towards interest payment while the remaining goes towards principal repayment.

The timing takes the cost to 11.25% p.a. Here is the proof.

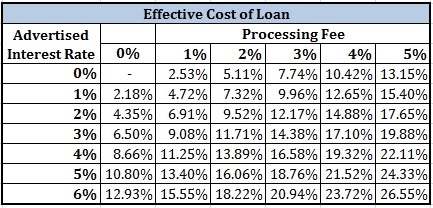

The effective interest cost won’t be 11.25% p.a. in all cases. The effective interest cost will depend on number of EMIs, processing fee charged and the advertised rate.

Here is the effective interest rate for different values of advertised rate and processing fee.

You can see that how increase in processing fee or the advertised rate increases the effective cost of loan.

By the way, only NBFCs can indulge in such tactics. Banks have been forbidden by RBI to indulge in such tactics. Therefore, you will mostly see such schemes from NBFCs such as Bajaj Finserv, Mahindra Finance etc.

What is in there for NBFCs?

The actual cost to you is the return for the lender.

Service tax will not go to the lender. That will bring down the return to the lender.

However, you can expect the lender to negotiate a discount with the dealer/seller, say 2%.

So, the cost for you is 1 lac but for the lender, it is only Rs 98,000 (essentially a kickback of 2% from the seller).

Hence, in the above example, while effective loan for you is 90,183 (Rs 1 lac – Rs 8,667 – Rs 1,150), loan offered by lender is only Rs 88,333 (Rs 1 lac – Rs 8,667 – Rs 1,000 – Rs 2,000).

That is a return of 15.52% p.a.

So, your effective cost is 11.25% p.a. but the return to the lender is 15.52% p.a.

Quite handsome by any standards!!!

And you thought that you were getting a good deal. It is the lender who is getting a much better deal.

To be fair to NBFCs, they do business to make money. Can’t fault them for that. And going for loan is your discretion.

PersonalFinancePlan Take

Well, do you have an option? If you do not have enough savings but need to make the purchase, you may have to go for this offer. There is no other option. Regular readers of this blog will know that I am not a big fan of taking on unnecessary debt. For me, taking a loan to purchase a gadget is unnecessary. For you, it may not be so.

Hence, if you have to make a purchase and you are short on funds, you may consider these options. To be honest, effective cost of loan in some cases may be better than the rate you would get for a personal loan. But yes, you will need to work out the maths.

However, if you have money in your bank account, you might just be better off paying from your pocket. Do not fall for such offers.