Healthcare costs in India are rising fast. And it is becoming increasingly expensive to provide quality healthcare to the family. Regular health insurance plans take care of the hospitalization expense, which is typically the biggest expense in any medical treatment.

However, your medical expenses don’t just end with hospitalization expenses. I do not deny that hospital bill can make the biggest dent on your pocket but there are other expenses too which can put a significant burden on your pocket. One of such expenses is Outpatient treatment (OPD) expense.

Outpatient Treatment is different from Day care procedures. As per IRDA, OPD treatment is one in which the Insured visits a clinic / hospital or associated facility like a consultation room for diagnosis and treatment based on the advice of a Medical Practitioner. The Insured is not admitted as a day care or in-patient.

A visit to a doctor comes under OPD.

Your family may avoid hospitalization for many years at a stretch. However, you have to be really fortunate to avoid doctor consultation for even a few months. Something or the other would come up and you will have to visit Out-patient Department (OPD) in a hospital or a clinic to seek doctor’s opinion.

Regular health insurance plans do not cover OPD expenses. With regular plans, the coverage is typically limited to hospitalization expenses (or pre and post hospitalization expenses).

Of late, insurers have started offering plans that cover OPD expenses too. Needless to say, such plans are likely to be quite expensive as the probability of making a claim is quite high.

How expensive are such plans? Should you purchase health insurance plans that cover OPD expenses? Or is it taking insurance a bit too far? Do such plans make economical sense? These are some of the questions I would try to answer in this post.

How expensive are plans with OPD coverage?

Health insurance plans that cover OPD expenses are quite expensive.

The problem is you may not be able to find plans that differ only on the OPD coverage. Hence, it becomes difficult to attribute excess premium to just OPD coverage.

Let’s make an attempt.

I pick up two health insurance plans, Apollo Munich Maxima and ICICI Lombard IHealth Plus that cover OPD expenses.

I will compare premium for Apollo Munich Maxima with Apollo Munich Optima Restore. The issue is these two plans differ on more than OPD coverage.

In case of ICICI Lombard IHealth Plus, you can purchase cover for maternity, OPD expenses and health checkup under a separate rider. So, this makes the comparison slightly easier.

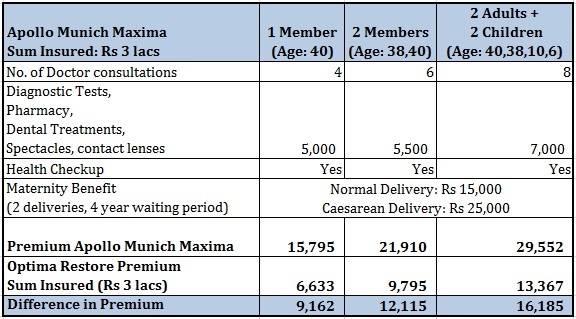

Apollo Munich Maxima

You can see that the difference in premium is quite substantial. For a family of four, the excess premium is Rs 16,185 per annum.

Let’s say a single consultation costs you Rs 600. For 8 consultations, you can get reimbursement for maximum of Rs 4,800. Add to it Rs 7,000 worth of medicines or dental treatment costs. That is a total of Rs 11,800. For this, you are paying excess premium of Rs 16,185.

Not just that, reimbursement for consultation at a non-network hospital is capped at Rs 400. How many of us go to big hospitals for regular consultations?

Yes, there is an additional maternity benefit but it comes with several limitations. You have a 4 year waiting period and even after that there is a sublimit on this expense. I ignore health checkups. These tests mentioned are fairly cheap and can be done only at specified network labs or hospitals.

In my opinion, cost does not justify the benefit.

Must Read: Should you purchase health insurance plan with Maternity Benefit?

ICICI Lombard IHealth Plus

Under this plan, you can purchase a rider over the base plan. This rider covers maternity expenses, OPD expenses and Health checkup costs. The total reimbursable expense for health checkup and OPD consultations is Rs 5,000 per policy year. Pharmacy expenses are not covered under the plan. There is no cap on the number of consultations. Compare this amount with excess premium that you are paying.

The difference is not as stark as in case of Apollo Munich Plan.

Points to Note

- You will have to get the expenses for OPD reimbursed. You can’t get cashless facility for OPD expenses.

- You will have to submit claim form along with payment receipts/invoices to the insurance company. The insurance company may also insist on other documents if required.

- There might be additional restrictions placed such as only one claim (ICICI iHealth Plus) during the policy year. So, you will have to keep all the receipts/reports/ consultation papers safe for that one claim at the end of the policy year.

- OPD expenses at non-network hospitals may be capped.

I will not be surprised if many of us fail/forget to make claim of OPD expenses incurred due to laziness. After all, you need to fill up a form, collect all the documents and send those to the insurance company.

Tax Benefits

After all, even plans with OPD coverage are health insurance plans. Hence, premium paid for health insurance plans with OPD coverage gets the same tax benefit.

So, even if you are paying excess Rs 5,000 for OPD coverage, you are essentially paying only Rs 3,500 since you are Rs 1,500 in tax (30% of Rs 5,000 for taxpayer in 30% tax bracket).

Must Read: Tax Benefits of Health Insurance

Who can opt for such plans?

- If you feel (based on experience) that you can take maximum benefit from these plans, you can opt for such health insurance plan with OPD coverage. However, there is a caveat. The annual premium mentioned in the previous sections is for healthy individuals. If you have been visiting a doctor quite frequently for an illness, be prepared to shell out higher premium. Redo the cost benefit analysis if the premium is loaded for you.

- You want to maximize tax benefit under Section 80D. However, do not get fixated with tax benefits.

Who must avoid these plans?

If you are a healthy individual, stay away from such plans. You wouldn’t visit a doctor just to make claim under the health plan. Even if you have to, there are better ways to plan for such expenses as discussed in the next section.

Any alternate approach? What about medical emergency corpus?

You can create a medical emergency fund. You are advised to have such a fund because regular health insurance plans do not cover many costs. OPD expense is one such expense.

There are many more. Your illness may require you to take medicine for a long time. Such expenses won’t be covered beyond a point. You may have to go through many diagnostics tests. Unless you get hospitalized within a few days after such tests, a regular health plan won’t cover the cost. Even during hospitalization, expenses for consumables are not covered.

Even though a health insurance plan takes care of the biggest expense (hospitalization), you may still have to shell out significant amount of money for other expenses.

It is to take care of such expenses that you need a medical emergency corpus.

In case you cannot purchase health cover for a family member due to any reason (old age, pre-existing illness, unaffordable), then the medical emergency corpus (and its size) gains even greater importance.

The focus of this post is OPD coverage. Hence, I will bring out the aspects in context of OPD expenses only.

In case you use money from this corpus, this corpus needs to be replenished.

And do factor inflation. Medical inflation is much higher than general inflation. I wouldn’t be surprised if the number is north of 15% per annum. And do not go by the number that you read in newspapers. Consider hikes in various charges at the hospitals that you visit.

In my case, the hospital I typically visit suddenly shot its OPD consultation fee from Rs 600 to Rs 900 one fine day. That’s a hike of 50%.

How big should be the medical emergency corpus?

It is difficult to put a number to it. I will be comfortable with a corpus of Rs 50,000-Rs 1 lac per family member. The size of the corpus also depends on the treatment cost at the hospitals in the vicinity.

How to build up this corpus?

You can keep this corpus in a fixed/recurring deposit or a liquid or short term debt fund.

Do note interest on FD/RD is taxable. Moreover, there will be capital gains tax implications if you redeem from mutual funds to fund your treatment.

PersonalFinancePlan Take

In my opinion, a health plan with OPD coverage is taking insurance a bit too far. There is no point trying to cover every bit of financial risk. Cover reasonable risk. Cover risk that is likely to take put a serious dent on your finances.

And strike a balance between cost and benefit.

Personally, I wouldn’t shell out Rs 6,000 for a benefit that is capped at Rs 10,000. Moreover, I am not sure if I will be able to take full benefit of Rs 10,000.

There is no need to purchase health insurance plans with OPD coverage. The numbers simply don’t add up. You end up paying too much. It is better to have a medical emergency corpus to take care of such expenses.

Do not go by what I say. Do a cost benefit analysis for your case. These calculations are quite simple and crisp. You can compare the difference in premium against the coverage (and prospects of utilization) for consultation and medical costs (medicines, diagnostics etc) and tax savings. And yes, do consider operational hassles of making a claim.

Image Credit: Pictures of Money, 2014. The original image and information about usage rights can be downloaded from Flickr.

2 thoughts on “Does it make sense to purchase Health cover with OPD coverage?”

Hello Deepesh,

Nice article…

As I am a Dental surgeon by profession I get a lot of patients who ask me about Insurance coverage for various Dental treatments.

Usually no one has much problem paying for regular dental trwatments which cost few thousands.

Patients usually enquire abt Insurance coverage when the treatment cost goes above 15,000, 20,000 or higher.

Now according to me if someone is getting a total benefit for OPD insurance capped at 5,000 annually then theres no point in going for these coverages.

Because only when one has to pay 20,000 or 30,000 for bridges or implants then only patient feels the pocket pinch…

In any case such high costs of OPD is not covered

Thanks Biswadeep.

Yes,even insurance companies are aware of these things. Health plan with OPD coverage is more a marketing gimmick than anything else. Makes for good sales presentation but little sense otherwise.