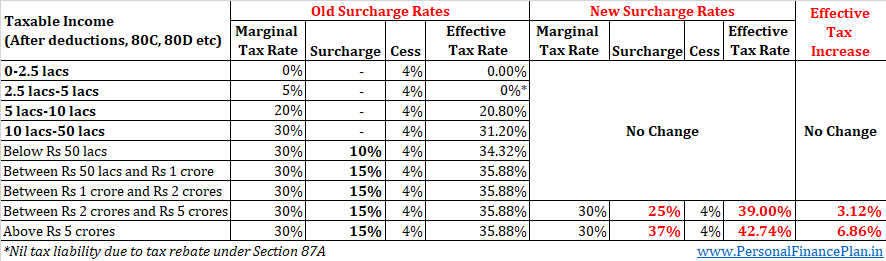

Taxes for the rich (high-income earners to be more precise) are going up. Apart from the usual income tax rates, you may have to pay surcharge too if your taxable income is in excess of Rs 50 Lacs. A Surcharge is levied on the income tax. Until about a few years back, the surcharge was applicable only if your income exceeded Rs 1 crores. Over the last few years, the Government has not only widened the scope of applicability of surcharge but has also increased the surcharge rates.

Here is the latest as per Union Budget 2019 (Final).

As you can see above, if your taxable income (after accounting for all the deductions) is above 50 lacs, your marginal tax rate is not just 30%. When you include surcharge and cess, it can shoot up drastically and range between 35.88% and 42.74%. Huge, isn’t it?

In this post, let’s look at the impact of such taxation on your tax liability. Additionally, I will also discuss a minor relief that taxpayers whose taxable income marginally exceeds Rs 50 lacs (or respective surcharge slabs such as 1 crore, 2 crore and 5 crores) can avail.

Impact on your Tax Outgo

What is Marginal Relief on Surcharge?

The basic idea is that the increase in tax liability (due to surcharge) should not exceed the increase in income. If that is the case, the taxpayer will get marginal relief for the difference amount.

Let’s consider with the help of an example.

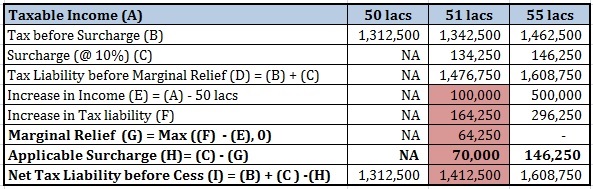

Suppose your taxable income (after deductions) is Rs 50 lacs. Since the income does not exceed Rs 50 lacs, there is no surcharge applicable. The tax liability before cess will be 13.125 lacs.

Let’s suppose you get a bonus of Rs 1 lac. Your taxable income goes up to Rs 51 lacs. The tax liability rises up to Rs 13.42 lacs (before cess). Surcharge at 10% equals Rs 1.34 lacs. Total tax liability before cess becomes Rs 14.765 lacs.

So, your salary/income went up by Rs 1 lacs while your tax liability has gone up by 1.64 lacs.

Sounds unfair, doesn’t it? Who would want such a bonus?

To take care of such anomaly, marginal relief is provided on Surcharge. This ensures that your tax liability does not increase more than the increase in income.

This relief will only be available in cases where the taxable income is marginally above the threshold. If you work out the numbers, you will realize that the marginal relief will only be available till the income level of Rs 51.96 lacs. (Rs 5,195,896).

Suppose X is your income and X is between Rs 50 lacs and Rs 1 crore. If you are interested in how I found out Rs 51.95 lacs at the limit, try solving the following equation.

X – 50 lacs = Tax liability on Rs X lacs * (1 + 10% surcharge) – Tax liability on Rs 50 lacs

If you have income higher than Rs 51.96 lacs, marginal relief will no longer be applicable because the increase in income will exceed the increase in tax liability (post surcharge). You can call Rs 51.96 lacs as the threshold.

By the way, the concept of marginal relief has been around for a long time. It is not new.

How do you calculate Marginal Relief?

Marginal Relief = Tax Liability on Rs X lacs * (1 + 10% Surcharge)

– Tax liability on Rs 50 lacs

– (X – 50 lacs)

Carrying forward from the above example where taxable income is Rs 51 lacs,

Marginal Relief = Rs 14.77 lacs – Rs 13.13 lacs -1 lac = Rs 64,250

Surcharge =134,250 -64,250 = 70,000

Another way to look at this analysis: From the taxable income of Rs 50 lacs to Rs 51.96 lacs, your net post-tax income will be the same. Any increase in income will set-off by an increase in tax and surcharge, adjusted for marginal relief.

Do note marginal relief on surcharge is not just available to tax-payers with income between Rs 50 lacs and Rs 1 crore. Marginal relief will come into picture whenever you are moving across various slabs for surcharge. You will have to tweak the above equation a bit to figure out the impact. You need to account for a surcharge of 15% (or higher as the case may be).

Am I eligible for marginal relief?

You are eligible for marginal relief if your income falls between the following surcharge slabs and thresholds.

Marginal Relief on Surcharge will be applicable between Surcharge slabs and Thresholds. This also implies that your post-tax income will remain constant between surcharge slabs and thresholds. For instance, if your income goes up from Rs 50 lacs to Rs 51.95 lacs, your post-tax income won’t change.

How to calculate these thresholds and marginal relief?

Threshold – Surcharge Slab = Tax Liability on Threshold – Tax liability on Surcharge Slab

Marginal Relief = Tax liability on X including Surcharge – Tax liability on Surcharge Slab including Surcharge – (X-Surcharge slab)

X refers to your taxable income. Surcharge slab is the slab just below X. So, if your taxable income is Rs 60 lacs, X is Rs 60 lacs and Surcharge slab will be Rs 50 lacs. If your taxable income is Rs 1.75 crores, X is Rs 1.75 crores and surcharge slab is Rs 1 crore.

Note that marginal relief can’t be negative.

Disclaimer

I am not a tax expert. You are advised to consult a Chartered Accountant.

The post was first published in February 2017 and has been updated since.

4 thoughts on “How Marginal Relief helps those who pay Surcharge on Income Tax?”

whether Amendment has done in case of domestic companies -surcharge rate whose Total income is between 50 lakhs to 1 crore

rebate is not provided for income of 350000 for ay 18-19

Agricultural income Rs. 300000

And Non Agricultural income Rs 5500000

So total tax with marginal relief. Please replay

Hi Amit,

Please work out the calculations with a Chartered Accountant.