LIC Dhan Sanchay (Plan 865) is a non-linked and non-participating life insurance plan. This means you will know upfront what you will get at the time of maturity. No scope for confusion. Unfortunately, that’s where the good parts end. While I didn’t expect the returns to be great, I didn’t expect returns to be so pathetic either. The returns are much lower than what non-participating plans from other insurance companies offer.

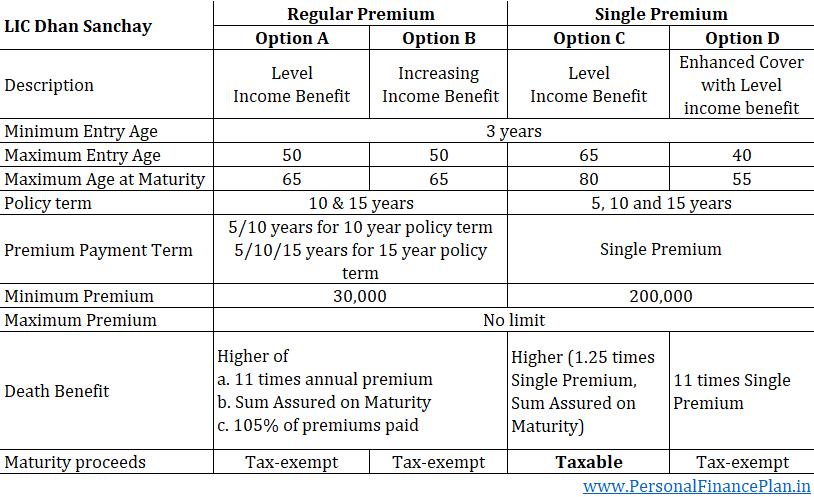

LIC Dhan Sanchay (Plan no. 865): Salient Features

1. Non-linked and non-participating. You know upfront what you are getting into. You can calculate the returns from this plan before you purchase the plan.

2. LIC Dhan Sanchay comes in 4 variants. Options A, B, C and D.

3. An income plan i.e., you pay the premium for a few years and LIC pays you for a fixed number of years after policy maturity.

4. Usual incentives for high premium and online purchases.

You can find more details about LIC Dhan Sanchay on the product page on the LIC website.

For Option C, since the minimum death benefit is not at least 10 times Sum Assured, the maturity payouts will be taxable. Maturity proceeds shall be exempt for all other variants.

Death Benefit is exempt under all the options.

LIC Dhan Sanchay (Plan 865): Maturity Benefit

Maturity benefit under LIC Dhan Sanchay is formed of two components.

Maturity Benefit = Guaranteed Income Benefit (GIB) + Guaranteed Terminal Benefit (GTB)

Guaranteed Income Benefit (GIB) is paid to the investor in installments. The duration and the size of installment depends on the variant chosen, policy term, and the premium payment term.

Guaranteed Terminal benefit (GTB) is paid lumpsum along with the last installment of GIB. So, the lumpsum payment is not made at the time of maturity but a few years after maturity.

In the next section, we shall see how GIB and GTB are calculated. While these calculations may seem a bit complex, you will know upfront (before the purchase of policy) how much you will get under GIB and GTB. That’s why LIC Dhan Sanchay is a non-participating plan. Everything is known upfront.

LIC Dhan Sanchay (865): How Guaranteed Income Benefit (GIB) is calculated?

Guaranteed income benefit (GIB) is payable during the payout period.

The payout period begins from the date of maturity and is equal to the

1. Premium payment term for Option A and Option B

2. Policy term for Option C and Option D (there is no premium payment term in these options. These are single premium plans after all).

You can select the frequency of payouts (monthly/quarterly/semi-annual/annual).

For regular/limited premium payment (Option A and B)

Guaranteed Income Benefit =Annualized Premium X GIB Multiple X Modal factor for GIB

We already know the annualized premium. The value of GIB multiple will depend on the variant (Option A or option B) and the policy term and the premium payment term.

Payout term shall be the same as premium payment term.

Payout term = Premium payment term

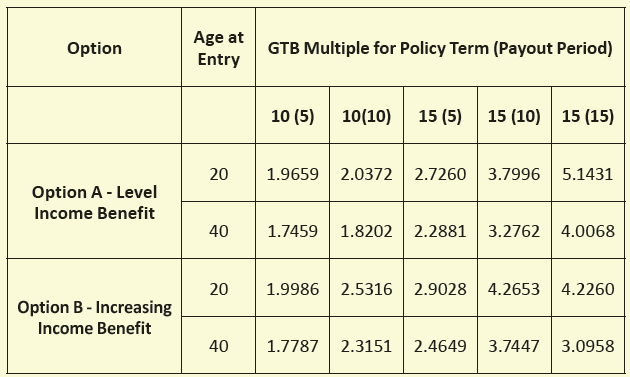

GIB Multiple for Option A and Option B

I reproduce the information from the policy brochure

Under Option A: Guaranteed income benefit remains constant throughout the payout period.

Under Option B: Guaranteed Income benefit increases by 5% every year. GIB multiples for Option B in the above table are for the first year only. That’s how the income increases every year.

The third variable is the Modal Factor for GIB. That depends on the payout frequency you opt for.

Illustration for GIB calculation

Option A

Let’s say a 40-year-old investor signs up for Option A and chooses an annual premium of Rs 1 lac (before taxes)

Policy tenure =10 years

Premium payment term = 10 years

Payout term = Premium Payment term = 10 years

Let’s say he opts for annual payout mode.

To calculate GIB, we need the following.

1. Annualized premium (Rs 1 lac)

2. GIB Multiple (The corresponding value for Option A, policy term of 10 years and premium payment term of 10 years is 1.3)

3. Modal factor for GIB (Annual Payout mode = 1)

GIB = Rs 1 lac X 1.1 X 1 = Rs 1.3 lac. You will get Rs 1.3 lacs per annum for 10 years.

Had you chosen monthly payout mode, the value of modal factor will change to 0.0850

GIB = Rs 1 lacs X 1.3 X 0.0850 = 11,050 per month for 10 years.

Option B

If you had chosen Option B (instead of option A), GIB Multiple would be 1.05.

GIB = Rs 1 lac X 1.05 X 1 (annual payout) = Rs 1.05 lac (this is the first-year payout)

Every year, the payout will increase by 5% (simple increase)

Hence, you will get Rs 1.10 lacs in the second year. Rs 1.15 lacs in the third year. Rs 1.21 lacs in the fourth year. Rs 1.26 lacs in the fifth and final year.

GIB Multiple for Option C and Option D

The modal Factor for GIB is the same as for Options A and B.

Option C

Entry age = 40 years

Single Premium = Rs 10 lacs. Policy Term = 10 years. Annual Payout.

Payout period = Policy Term = 10 years

GIB Multiple = 0.18

GIB = Rs 10 lacs X 0.18 X 1 = Rs 1.8 lacs per annum for 10 years.

Option D

GIB = 0.15

GIB = Rs 10 lacs X 0.15 X 1 = Rs 1.5 lacs per annum for 10 years

Note: Everything else being the same, you will get a higher income in Option C compared to Option D.

Why?

Under Option D, you get a much higher life cover (11 X Single premium). Under Option C, you get only 1.25 X Single Premium). Under Option D, a bigger portion of the premium goes towards providing life cover. Hence, lower payouts. Along expected lines.

No free lunch.

At the same time, the proceeds from Option C are taxable. Tax-exempt for Option D.

LIC Dhan Sanchay (Plan 865): Guaranteed Terminal Benefit

Guaranteed Terminal Benefit (GTB) = (Annualized Premium/Single Premium) X GTB Multiple X Modal Factor for GTB

As I understand, the modal factor or GTB depends on the payout frequency chosen for the GIB.

Illustration for GTB calculation

Option A

40-year-old; Annual Premium: 1 lac; Policy Term=10 years; Premium Payment Term=10 years

GTB = Rs 1 lacs X 1.8202 (GTB Multiple) X 1 (GTB modal factor) = Rs 1.82 lacs

This will be paid along with the last installment of GIB. For a premium payment term of 10 years, this will be payable at the end of 9 years from the date of maturity.

Option B

40-year-old; Annual Premium: 1 lac; Policy Term=10 years; Premium Payment Term=10 years

GTB = Rs 1 lacs X 2.3151 (GTB Multiple) X 1 (GTB modal factor) = Rs 2.31 lacs

This will be paid along with the last installment of GIB. For a premium payment term of 10 years, this will be payable at the end of 9 years from the date of maturity.

Option C

40-year-old; Single Premium: 10 lacs; Policy Term=10 years; Single Premium Payment

GTB = Rs 10 lacs X 0.3606 (GTB Multiple) X (GTB modal factor) = Rs 3.6 lacs

This will be paid along with the last installment of GIB. For a policy term of 10 years, this will be payable at the end of 9 years from the date of maturity.

Option D

40-year-old; Single Premium: 10 lacs; Policy Term=10 years; Premium Payment Term=10 years

GTB = Rs 10 lacs X 0.0469 (GTB Multiple) X (GTB modal factor) = Rs 46,900

This amount will be paid along with the last installment of GIB. For a policy term of 10 years, this will be payable at the end of 9 years from the date of maturity.

LIC Dhan Sanchay (Plan 865): What are the expected returns?

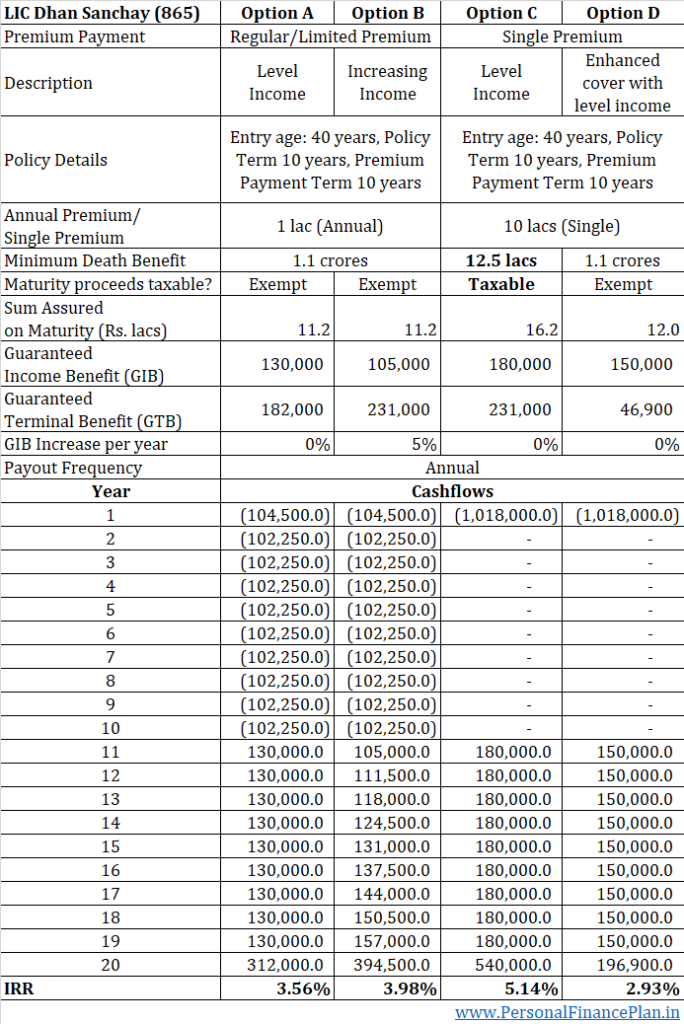

I can’t calculate the returns for all the entry ages, variants, policy terms, and policy payment term combinations. I have calculated the entry age of 40, policy term of 10 years and premium payment term of 10 years.

Should you invest in LIC Dhan Sanchay?

As you can see, the returns are just pathetic. You expect better than 3-4% p.a. for a long-term product Yes, LIC Dhan Sanchay has a life insurance component but that doesn’t change the conclusion. For life cover, you can always buy a cheap term insurance plan.

The returns can vary slightly based on the entry age and the policy and premium payment terms chosen.

The returns from Option C seem much higher at about 5% p.a. This is because the life cover component is much lower in Option C (only 1.25 X Single premium). However, for the same reason, the maturity payouts from this plan will be taxable.

Stay away from LIC Dhan Sanchay.

Additional Points

Death Benefit can be taken in installments of up to 5 years.

The default option under LIC Dhan Sanchay is lumpsum. However, if you wish, you can specify that your nominee receives death benefit in installments.

The policyholder must exercise this option during his/her lifetime. The nominee cannot exercise this option.

The interest rate used for calculation of installments shall NOT be lower than (5-year Gsec rate – 2%). That’s quite low.

I understand why you would want your nominee to receive death benefit in installments. In many cases, nominees can’t manage such a large corpus, especially during times of emotional stress. Receiving death benefit in installments gives them the breathing space and you can be sure that at least the next few years are covered.

Hence, while receiving death benefits in installments is not the most optimal solution, you might find merit in exercising this option.

Maturity Benefit can be taken lumpsum

We discussed earlier how maturity benefit under LIC Dhan Sanchay is paid in installments spread over many years.

If you wish, you can choose to receive maturity benefit lumpsum.

If you exercise this option, you will get Sum Assured on Maturity.

Sum Assured on Maturity = (Annual premium, Single premium) X Maturity Benefit Multiplier

For instance, in the illustration discussed earlier, we consider the entry age of 40 with policy and premium payment terms of 10 years.

Under Option A, if you choose to receive the maturity benefit as lumpsum, you will get Rs 11.21 lacs on the date of maturity.

The IRRs in this case will be even lower at about 1.6% p.a.

Hence, this option must be used only in extreme cases.

2 thoughts on “LIC Dhan Sanchay (Plan no. 865): Review”

Any illustration for lumsum maturity amount for option A

Shared for a particular age (40 year old male) in the post.

You want to understand something else?