NHAI tax-free bonds issue opens on December 17, 2015 and closes on December 31, 2015. The issue size is Rs 10,000 crores. NTPC, PFC , REC and IRFC have already come out with tax-free bonds issue this fiscal.

In this post, I shall focus only on the factual information about these NHAI bonds. Everything else remains the same. You can refer to my posts on NTPC, PFC , REC and IRFC tax-free bonds for detailed rationale.

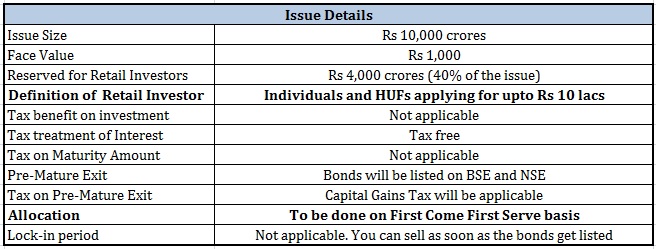

NHAI Tax-Free Bonds Issue: Salient Features

NHAI Tax-Free Bonds Interest Rates

Points to Note about NHAI Tax-Free Bonds

- Only the interest earned is exempt from tax.

- There is no tax exemption under Section 80C of the Income Tax Act on the investment amount.

- Retail investors can only invest up to Rs 10 lacs (no more than 1000 bonds) in these bonds.

- If you purchase more than 1000 bonds, you will be classified as High Net worth Individual and will be eligible for a lower interest rate.

- Interest shall be paid annually.

- NRI cannot invest in NHAI tax-free bonds. They were allowed to invest in earlier issues by NTPC, IRFC, PFC and REC.

- The allotment will be on First-Come-First-Serve basis.

- If you sell these bonds within 1 year, capital gains will be taxed as per your income tax slab.

- If you sell these bonds after 1 year, capital gains will be taxed at 10%. There is no benefit of indexation for these bonds.

- These bonds will be listed on BSE and NSE. However, you can expect liquidity to be low. Hence, exit in the secondary market won’t be as easy.

Should you invest in NHAI Tax-free Bonds?

Investors in the 10% tax bracket do not have much to gain by investing in these bonds. Only those in 20% or 30% tax brackets and seeking regular income should think about investing in these tax-free bonds. Exit in the secondary market may not be as easy or at an unfavorable price. So, be prepared to hold the bonds till maturity if you are planning to invest.

Senior Citizens can get 9.3% p.a. in senior citizen savings scheme (SCSS). Though the interest from SCSS is taxable, you get tax benefit on investment under Section 80 of the Income Tax Act. So, if you are taking full tax benefits, the post-tax yield of SCSS will be much higher than that of tax-free bonds.

You don’t get benefit of compounding in these bonds. So, these bonds don’t suit you if you are looking for long term wealth creation.

If you are planning to invest in this issue, do apply on the first day itself. Given the demand for these bonds, you may not get any allotment if you don’t apply on December 17.