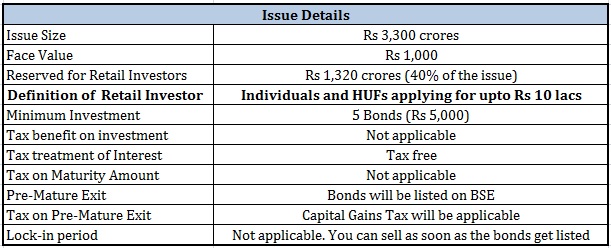

NHAI is coming up with its second tranche of tax-free bonds issue this fiscal. The issue will open on February 24, 2016 and close on March 1, 2016. The issue size is Rs 3,300 crores.

NHAI issued tax-free bonds worth Rs 10,000 crores in December 2015. Many other PSUs including NTPC, PFC , REC and IRFC have issued tax-free bonds this fiscal.

The investment rationale does not change from my previous posts on tax-free bonds. I will focus mostly on the factual aspects on the issue in this post.

NHAI Tax-Free Bonds: Tranche II: Salient Features

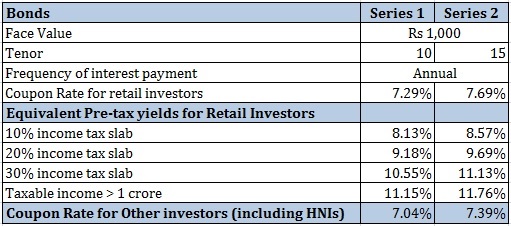

NHAI Tax-Free Bonds Interest Rate

Points to Note about NHAI Tax-Free Bonds

- The bonds are available in maturities of 10 and 15 years only.

- The coupon on these bonds in the December tranche was 7.39% p.a. for 10 year and 7.60% for 15 years.

- Only the interest earned is exempt from tax under Section 10(15) (iv)(h) of the Income Tax Act.

- There is no tax deduction under Section 80C on the investment amount.

- Retail investors can only invest up to Rs 10 lacs (no more than 1000 bonds) in these bonds.

- If you purchase more than 1000 bonds, you will be classified as High Net worth Individual and will be eligible for a lower interest rate.

- Interest shall be paid annually.

- NHAI is promoted by Government of India. So, I wouldn’t really worry about credit risk. The issue has been rated AAA by CARE, ICRA and CRISIL.

- NRI cannot invest in NHAI tax-free bonds.

- The allotment will be on First-Come-First-Serve basis.

- If you sell these bonds within 1 year, capital gains will be taxed as per your income tax slab.

- If you sell these bonds after 1 year, capital gains will be taxed at 10%. There is no benefit of indexation for these bonds. For more on taxation of tax-free bonds, refer to this post.

- These bonds will be listed on BSE and NSE. However, you can expect liquidity to be low. Hence, exit in the secondary market won’t be as easy.

- You can hold the bonds in both physical and demat format.

Should you invest in NHAI Tax-free Bonds?

(This part is essentially a copy paste from my post on HUDCO Tax-free Bonds. You can read that post here. The rationale can be extended to any issue of tax-free bonds)

These bonds are long tenor bonds and exit from these bonds won’t be easy. The interest is exempt from tax.

The tenor is 10 and 15 years. Investors looking to invest for such long horizon may find better options in equity mutual funds.

Since there is regular interest payout, you don’t get benefit of compounding in these bonds. So, these bonds are not suited for long term wealth creation. Hence, if you do not seek regular income, then these bonds are not for you.

Investors in the 10% tax bracket do not have much to gain by investing in these bonds. You can create FDs for 7.5-8% easily without any lock-in period. If you consider 50 basis points of interest more important than locking your money for 10-20 years, then you can go for these bonds. Personally, I wouldn’t apply if I were in 10% tax-bracket.

Those in 20% or 30% tax brackets and seeking regular income can think about investing in these tax-free bonds.

Exit in the secondary market may not be as easy or at an unfavorable price. So, be prepared to hold the bonds till maturity if you are planning to invest. In any case, if you are looking for a favorable exit in the secondary market, you are betting on interest rates, which are never easy to predict. And yes, don’t forget about capital gains taxes.

Do consider the following before making the final decision.

Retirees and Senior Citizens can get 9.3% p.a. in senior citizen savings scheme (SCSS). Even though the interest on SCSS is taxable, you get tax benefit on the investment amount under Section 80C of the Income Tax Act. Thus, the effective yield is much higher, especially if you are taking full tax benefits.

There is no tax benefit on investment amount under Section 80C HUDO tax-free bonds.

The same argument can also be extended to 5-year tax saving fixed deposits.

For instance, if you invest in a 5-year tax saving FD that offers 8% per annum, the post-tax yield (effective yield) shall be 9.89% (10% tax bracket), 12.08% (20% tax bracket) and 14.68% (30% tax bracket).This is under the assumption you get full tax benefit for investment in such FD under Section 80C. Though tax-free bonds and tax-saving FDs are not strictly comparable, I hope you get the idea.

It should not happen that you leave your Section 80C limit unutilized while you are investing in tax-free bonds.

14 thoughts on “NHAI Tax-free Bonds: Tranche II: Should you invest?”

Have you seen the Market price of NHB bonds jan 2014 and NTPC bonds Dec 13—trading by 15-20 % more then the face value. I mean to say exit is not issue as listed either at BSE or at NSE

Price is not a reflection of liquidity. The prices have gone up because interest rates have gone down.

Liquidity is measured through volumes and spreads.

That will give an idea if you can exit whenever you want to without too much of an impact cost.

You should not confuse by comparing tax saving FD with tax free bond as interest from tax saving FD is taxable however from tax saving bond is not.

Rishab,

I put that down clearly. There is no intent to confuse readers.

On tax-free bonds, there are no tax benefit under Section 80C while 5-year tax-saving FDs have tax benefits under Section 80C (that pushes up post tax yield). There is no jugglery that I am doing. I have supported my argument with mathematics.

when they are likely to be issue next NHAI tax free bonds ??

Gouthami, I am not sure.

How does one purchase these bonds, when they are issued?

There are many ways. In my opinion, the most convenient is through ICICIDirect.

If you plan to subscribe to such issues in the future, open an account with ICICIDirect.

I am sure there are other portals too but my experience with ICICIDirect has been excellent.

Thank you. Will try with ICICI.

You are welcome, John.

These bonds offer a tax rebate as per section 54 EC (Long term capital gains), Can NRI investing in these bonds, repatriate the funds after the period of maturity?

Dear Ram,

Section 54EC bonds, though issued by NHAI are different from tax-free bonds.

Tax-free bonds are not eligible for Section 54EC benefit.

NRI were not permitted to invest in these bonds. If they were allowed to invest on repatriation basis, they could repatriate money after maturity.

can i invest 50lakhs rupees every year in nhai bonds by selling

property worth 50 lakhs evry fincial year.

Dear Mandar,

NHAI tax-free bonds are different from NHAI capital gains bonds you are talking about.