If you keep a sizeable amount of money in savings bank accounts or bank fixed deposits, you must know about tax relief on interest income under Section 80TTA and 80TTB.

Let’s find out about the tax relief under Section 80TTA and Section 80TTB.

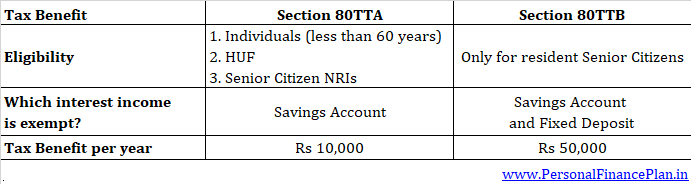

#1 Section 80 TTA (Interest Income on Savings Bank Accounts)

Interest earned on savings accounts is exempt from income tax to the extent of Rs 10,000 per financial year.

Only the interest earned on the savings account is eligible for benefit under Section 80TTA.

Only the saving accounts with the following entities qualify for the benefit under 80TTA.

- Banks

- Post Offices

- a co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank or a co-operative land development bank)

Interest earned on fixed deposits does NOT qualify for tax benefit under Section 80TTA.

Who is eligible?

- Individuals and HUF (Hindu Undivided Family) are eligible.

- NRIs can also take benefit under Section 80TTA. They can take benefit for interest earned on NRE and NRO savings accounts.

- If you are eligible for tax benefit under Section 80TTB, you cannot take benefit under Section 80TTA. To be discussed later.

#2 Section 80TTB (Only for Senior Citizens)

The tax relief is only for Senior Citizens. If your age is less than 60 years, you can’t seek tax relief under Section 80TTB.

This tax rule was introduced in Budget 2018 and is applicable from FY2019.

As per this section, interest income from savings bank accounts and fixed deposits is exempt from income tax to the extent of Rs 50,000 per financial year.

To be eligible for tax benefit under Section 80TTB, the deposit (savings and fixed) must be with one of the following:

- Banks

- Post Offices

- a co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank or a co-operative land development bank)

Who is eligible?

- Only resident senior citizens are eligible.

- Non-residents are not eligible. Taxpayers under the age of 60 are not eligible.

Points to Note

- Interest income from company fixed deposits or bonds/NCDs will not qualify for relief under Section 80TTB. Only the interest income from deposits with banks, post-offices and co-operative banks qualifies.

- Income from Pradhan Mantri Vaya Vandana Yojana (PMVVY) is NOT eligible for relief under Section 80TTB.

- As I understand, even the interest earned on Senior Citizens Savings Scheme (SCSS) is NOT eligible for relief. Not very sure about this though.

Section 80TTA Vs. Section 80TTB

If you contrast relief under Section 80TTA with Section 80TTB, you can see

- Relief under Section 80TTA is limited to savings accounts while Section 80TTB covers both savings account and fixed deposit accounts.

- Rs 10,000 under Section 80TTA vs Rs 50,000 under Section 80TTB

- Relief under Section 80TTA available to individuals and HUF. Section 80TTB provides relief to only individuals.

- Section 80TTB provides relief to only resident senior citizens. No such restriction under Section 80TTA.

Either Section 80TTA or Section 80TTB

As you can see, senior citizens (who are resident) will take tax benefit under Section 80TTB. Therefore, they won’t be able to take tax benefit under Section 80TTA of the Income Tax Act.

Only those who can’t seek relief under Section 80TTB can seek relief under Section 80TTA.

Since Section 80TTB provides much higher and wider tax relief, senior citizens have nothing to complain about.

Additionally, since Section 80TTB provides relief to only resident Indians, senior citizen NRIs cannot take benefit under Section 80TTB. Now that such senior citizens can’t take benefit under Section 80TTB, senior citizen NRIs can seek relief under Section 80TTA. Interest on NRE savings account or FDs is anyways exempt from tax. Senior Citizen NRIs can utilize this benefit under 80TTA for interest on NRO savings account.

10 thoughts on “Section 80TTA and Section 80TTB: Saving tax on interest income”

Referring your article, which is quite explanatory- Kindly let us know the provision for NRO account clearly again. In NRO account, the bank deducts TDS @ 30% + Cess, and deposits it with the Government.

Kindly let me know if the Interest so earned shall be covered u/s 80TTA, and shall the TDS be treated as TDS for Income Tax purposes.

The Bank refuses to issue form 16A (TDS).

Regards

V.K.Dadoo

Thank you sir!!!

Yes, you can claim back refund for the excess tax paid while filing ITR.

Relief under 80TTA is available to NRIs too (only for NRO savings and not NRO FDs).

Thanks for your kind reply. However, the refund can not be claimed unless the deducted TDS is reflected in Form 26AS, and the bank in this case, ICICI bank has told us clearly that this form 16A in respect of the TDS can not be issued.

With your kind permission I intend taking up with the ICICI Bank customer care and other officials for issuing us the TDS certificate, which naturally will be in the form 16A.

Regards

V.K.Dadoo

Dear Sir,

If TDS has been deducted, it must show in your 26AS.

The bank cannot deny your request for Form 16A (though I think you don’t need it).

You don’t spend too much time talking to customer care.

Write an e-mail to customer care.

If you don’t get a satisfactory response, escalate to mdceo[at]icicibank.com

Should get resolved in a few hours.

Great article, so informative!

Thank you Abhinav!!!

Dear Deepesh Ji,

1) I have sold agricultural land worth Rs.1.36 crores in FY 2018-19. LTCG is 1.30 crores. I’ll be investing Rs.50 lakhs in NHAI/REC bonds in FY 2018-19.

2) I will be selling agricultural lands again worth Rs.37 lakhs in FY 2019-20. LTCG is 32 lakhs.

Can I invest 32 lakhs in NHAI/REC bonds in FY 2019-20 even though I have invested 50 lakhs in NHAI/REC bonds in FY 2018-19 or there a one time limit on investments in NHAI/REC bonds.

The above mentioned sale of Rs.1.36 crores and 37 lakhs are separate transactions.

Dear Kaushal ji,

This part is slightly subjective.

Here is what is mentioned in Section 54EC

Provided further that the investment made by an assessee in the long-term specified asset, from capital gains arising from transfer of one or more original assets, during the financial year in which the original asset or assets are transferred and in the subsequent financial year does not exceed fifty lakh rupees.

Even though the cap is for a financial year, the aforesaid clause can cause problems.

You sold first property in FY2019. You will invest in bonds in FY2019.

The aforesaid clause is to prevent sellers from saving tax by splitting the bond investments across two years (for the same investment). Even though you have two properties, the clause could be interpreted to prevent you from investing more than Rs 50 lakhs in FY2019 and FY2020.

To avoid confusion, sell the second property towards the second half on FY20 and make tax-saving investment in bonds in early part of FY2021.

Please consult a Chartered Accountant too.

Greetings !!

I have a doubt regarding the interest to be claimed under 80 TTB for senior citizen. Where it is said, that “including saving interest the assessee can claim under 80TTB “

Dear Sir,

You have to refer to Section 80TTA. 80TTA mentions that you can use this section if you have taken benefit under Section 80TTB.

Where the gross total income of an assessee [(other than the assessee referred to in section 80TTB)], being an individual or a Hindu undivided family, includes any income by way of interest on deposits (not being time deposits) in a savings account with—

Hope this answers your query.