A few days back, I watched a commercial by LIC promoting its children’s plan. The two plans promoted were LIC Jeevan Tarun and LIC New Children’s Money Back Plan.

I had reviewed LIC Jeevan Tarun in an earlier post and found it to be an utterly stupid product. Though I do not expect LIC New Children’s Money Back plan to be any different, I will still review this product to complete the review set.

Please note I have nothing against LIC. Even private insurers come out with equally bad products. However, since LIC is more popular and better trusted, it is easier to get the message across. You must be equally apprehensive of such products from private insurers.

You are advised to go through reviews of LIC New Jeevan Anand, LIC Jeevan Tarun and LIC New Money Back Plan-25 years. These reviews will give you an idea about inherent issues in traditional life insurance plans.

Review: LIC New Children’s Money Back Plan

New Children Money Back plan is a participating non-linked money back plan.

Like all money-back plans, you get guaranteed payback (percentage of Sum Assured) from the insurer during the premium payment term. At maturity, you get the unpaid Sum Assured along with vested bonuses.

You can find policy wordings for the plan on LIC website.

Bonus is a much misused keyword when it comes to traditional life insurance plans.

Under this plan, Simple Reversionary Bonus in announced every year by LIC. It is expressed as per thousand of Sum Assured. Do note even though the bonus is announced every year, it is paid only at the time of policy maturity. So, LIC may have announced a bonus of Rs 40,000 for your plan. You wouldn’t Rs 40,000 right. You get the amount only at the time of maturity. And therein lies the trick.

Go through the post on LIC New Money Back Plan to understand how this bonus feature is smartly used during sales pitches.

There is no compounding.

Getting Rs 40,000 today is not same as receiving Rs 40,000 20 years later.

Though Final Additional Bonus (FAB) is announced every year, it is applicable for your plan only in the year of maturity or death. If LIC does not announce anything in the year of maturity (or death of the policy holder), you don’t get anything.

Salient Features: LIC New Children’s Money Back Plan

- Life cover is on the life of the child

- Entry Age: 0 to 12 years

- Policy Term: 13 to 25 years

- Policy matures when the policy holder turns 25 (policy anniversary immediately following 25th birthday)

- Premium waiver rider is available in the event of death of parent/proposer. I ignore this rider. Will focus only on the base plan.

Survival Benefits under LIC New Children Money Back Plan

Your child gets 20% of Sum Assured on policy anniversary immediately following 18th, 20th and 22nd birthday.

At maturity (after 25th birthday), the child will get remaining 40% of the Sum Assured, along with vested Simple Reversionary Bonuses and Final Additional Bonus, if any.

Death Benefit under LIC New Children’s Money Back Plan

As frivolous as it may sound, life insurance is on the life of the child.

This is a good enough reason for you to discard this plan.

Who takes a bet on his/her child’s life?

So, if something were to happen to you, your family won’t get anything. In that case, essentially, it becomes an investment plan. And traditional life insurance plans provide guaranteed poor returns.

You purchase insurance so that your family’s finances are taken care off in case you are not around.

Although this aspect is meaningless, even the cover on the life of the child does not commence from day 1. The life cover commences once your child turns (first policy anniversary after the child turns 8) and two years from the date of purchase of policy, whichever is earlier.

In the event of death (of child) before commencement of risk (life cover), you will get back total premiums paid till date excluding taxes and rider premium.

In the event of death (of child) after commencement of risk (life cover), you will get:

Sum Assured + Vested Simple Reversionary Bonuses + Final Additional Bonus, if any

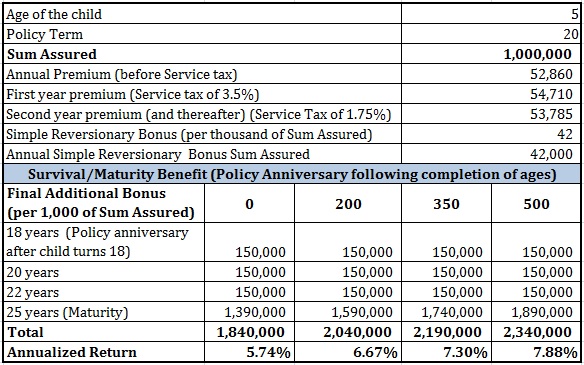

Illustration

Suppose you purchase LIC New Children Money Back plan for your daughter aged 5 years. The policy term is 20 years and the policy matures after your daughter turns 25.

You chose Sum Assured of Rs 10 lacs.

The annual premium for the plan is Rs 54,710 in the first year and Rs 53,785 in the subsequent years.

New Children Money Back plan is a new plan. Hence, bonus for only last year is available. In 2015, the Simple reversionary bonus for policy term of 20 years was Rs 42 per thousand of Sum Assured.

That makes it an annual bonus of Rs 42,000 (42 * Rs 10 lacs / 1000). I have assumed the bonus will remain same during the course of the plan.

Final Additional Bonus (FAB) is tricky since it is applicable in the year of maturity/death. Hence, I will consider for various values of FAB

You can see the return for a very optimistic FAB is 7.88% p.a. only.

Even the safest PPF gives a return 8.1% at the moment. You may argue returns in PPF are not guaranteed and may change next year. However, bonuses on LIC plans are not guaranteed either. LIC may not declare any bonus or may declare a lower bonus.

Had you invested the same amount in PPF account for your daughter, your daughter will have Rs 26.9 lacs in her PPF account when she turns 25.

I ignore Death benefit under the plan because the life insurance is of the life of your daughter. By doing so, the return under the plan has increased a bit (as the mortality charges will be lower for a child). However, life insurance component of the plan serves little purpose.

Must Read: Which is the best term life insurance plan for you?

PersonalFinancePlan Take

Traditional Life insurance plans are opaque, provide low life coverage and guaranteed poor returns. LIC New Children Money Back plan is no different.

Regular payout after completion of 18, 20 and 22 years are meant to fund your children’s education. Your child will receive maturity amount after turning 25. You may plan to use the money for children’s education and marriage.

However, the returns, as we have seen, are low. Even PPF is expected to beat the returns easily.

Moreover, there is little flexibility if you want to exit/surrender the plan and take out your money. There is heavy surrender penalty.

But the clincher is the life cover. Life cover is on the life of the child. Such cover is meaningless. In such a case, you are purchasing the product only for investment purpose. And you know investment returns are bad in such plans. Good enough reason to avoid the plan.

Verdict: Stay away from LIC New Children Money Back Plan

30 thoughts on “Don’t invest in LIC New Children’s Money Back Plan”

Fr

Hi iam 35 yrs self employed in mumbai .i have to pay 16 lac final installment for a home. No loan has been taken by me ever . should i pay the installment without taking home loan or take a home loan for it and invest this money in mf for long term retirement planning ?

Additinally There is abt 15 lakh in ppf and mf and i own another house which is on rent. I also stay on rent. Please advice..

Dear Tarun,

This is not the relevant post.

I understand, in your case, entire interest is tax deductible. Hence, the effective cost of home loan will be low.

However, that does not mean that you take a loan.

There is no crisp answer.

A lot depends on your existing investment pattern and the cash flows.

But yes, do not withdraw from your PPF to repay this loan.

I assume you have never ventured into MFs.

If I were you, I will not complicate things. I will simply pay the final installment from excess cash. Subsequently, I will start SIPs in MFs from my monthly cashflows.

Request you to post any follow-up queries in comments section of the following post.

http://www.personalfinanceplan.in/opinion/do-not-overestimate-tax-benefits-on-home-loan-repayment/

I am already running sip mmfs …i wanted to know iif i should put 16lakh in mmf for retirement or pay pproperty inatallment

Rs 16 lacs lumpsum given your current asset book may be tricky. You will need an investment strategy.

Repay the loan.

Dear sir u want to invest in lic mf growth fund and mf mid cap fund sip …do u hv any better ideas

Dear Apsal,

Didn’t get your question. Do you want to invest in these funds?

I strongly disagree with you. Life cover on child is actually a pretty good option (At-least for boy child). We Indians always see our children as future investment/pension fund. We always remind them, they should start earning soon, so that we can retire. We also often remind them directly ‘We’ve big financial hopes on you’. This system is remarkably different from that of west.

So loss of a 25-year old son is a big financial loss for us in an Indian perspective & should be adequately covered.

You are entitled to an opinion. We can always disagree.

“At-least for boy child.” Is girl child not important?

I do not differentiate between a boy and a girl child.Hence, simply can’t relate what you are saying.

For me, loss of a child is much bigger concern/fear than its financial impact. Therefore, you can expect my priorities to be very different.

I would plan my finances in a way that I do not have to depend on my kids.

In any case, traditional plans provide a low cover. Term insurance is a much better choice.

Hye…then which child plan do u suggest

None. Purchase a term plan and invest in equity MFs, PPF, SSY.

Dear deepesh

Kindly refer which is the best policy for 4 yr kid?

Don’t buy life insurance for the kid.

You need life cover, not them.

Seek professional help.

Dear

sir any queries and any comments to lic policy so please call and meet my branch lic

branch (unit 310 janpath new delhi)

Should you have any comments or queries please do not hesitates to contact.

Thanks and regards

PramodTiwari

Senior Insurance Advisor (Lic of india)

Branch Office: 310, Oriental Annexe 1st and 2nd floor, 86, Janpath, New Delhi – 110001

Satellite Office: 310 (SO), Plot No. 32, DDA Community Centre, Rani Bagh (Behind M2K Pitam Pura), Delhi – 110034

Mobile-09310467871

09650941046

Email -pramodtiwari310@yahoo.com

Hi Sir,

I want to know about which child plan is good.

Child Age 3y and father age 28y

Thanks

Sanjay

Hi Sanjay,

Purchase insurance for you, not for your kid.

http://www.licinternationaluae.com/Prof_Edu_Plan.html

hi

can n u please review the licinternational dollar child education plan and help us decide

this is the link

thanks

Looks like a regular money back plan.

I won’t be very keen on this plan.

Hello Mr. Raghaw,

What do you suggest would be the most appropriate investment option for my daughter (2 months old) considering monetary requirements for her future (studies / marriage)? I plan to invest 60ks/year.

Thanks in advance for your advice.

Best regards,

Debarun Basu.

Dear Debarun,

In my opinion, purchase a term plan on your life and invest in PPF/SSY/mutual funds for your daughter’s education.

Hello Mr. Raghaw,

To add onto my previous question, I also have a PPF a/c for around 5 yrs. I do not contribute much to that account at this point of time. However is it possible that I can leverage this PPF a/c for my daughter’s future financial requirements and for how long can I continue to contribute to my PPF a/c?

Thanks in advance for your advice.

Best regards,

Debarun Basu.

While I was looking for child plan options, even I had a similar opinion on why child’s life is being insured rather than the premium payer’s life and was looking for a plan where guardian’s life would be insured in a child’s plan , but seems like there are none linking child and premium payer’s life. Your post has given me much needed clarity and instilled confidence in my decision on why not to go for a child plan or rather how to go about saving for a child.

Thank you for the much needed and kind advice Deepesh

Regards

Hardik Singh

Hi Hardik,

We are exactly on the same page.

Thanks for your kind words.

Hi Deepesh

I have a SSY for my daughter however that will mature when she reaches 21 Yrs, however i am looking at additional investment when she reaches 17-18 Yrs as she might plan for a foreign university or within India some new educational courses which might be expensive looking at rising cost in education sector?

Thanks in advance for your guidance.

Hi Japjit,

Please consult a financial advisor in your city. Some exposure to equity funds may help.

Hi,

Thanks for your advice and i partial accept that. I am a businessman and i need some sort of commitment to set aside as savings for my baby girl. LIC Plans gives us a range of our return values altought not exact and what we are going to get is almost clear and what we need to pay is fixed.

But in PPF and MF the returns may vary and no one can predict 18 years financial track from now.So i feel LIC policy is somewhat a safe side to depend upon. And also an added advantage is the returns are tax free.

Your opinion on this.

Hi Raj,

If you are more comfortable with LIC, go ahead with it. Just that you have to live with lower returns over the long term. You don’t need life insurance for a kid either.

With PPF, you will most likely get better returns than the LIC policy. PPF is tax-free too.

Yes, MF offer potential for higher returns but at a higher risk. So, not for everyone.

Sir, please Post a review on LIc Jeevan Saral Policy. Thanks

Hi Deepesh,

Is the Bal Suraksha plan from LIC on the same terms as this new children money back plan?

Please let me know. Thanks!

I like your post, i took a pause but when it comes to loan from a policy with simple interest charges compared to compounded interest charges, you can run your policy for 5+ years then you can take loan out of it to pay your premium which company’s allows that benefit, returns are low but their is a risk cover and death benefit, MF or other instrument only talk about return which they cannot guarantee after 20 years+ its just a calculation that in future if your portfolio grows by 6% annually for 25 years then on 26th years, market crashes that will eat up your returns which has happened during covid, LIC guarantees the sum, how about the taxes FD attracts TDS, Instruments attracts LTCG. I am satisfied with LIC, because LIC gives limited SI charges loan and my studies, fees were covered by only LIC. Trust is all that matters.

Hi Shireesh Shrivastava,

More over, the premium waiver rider benefit will be very much useful, if any risk happened to the parent , all the future premium will be waived and the child will get the complete benefit without paying any premium. No other instruments ( PPF or FD or MF ) can give this option.