Which is the best way of investing in gold?

Physical gold, Jewellery, gold ETFs, mutual funds, or Sovereign gold bonds?

Let us leave out physical gold and jewellery in this post and focus on financial investments in gold.

In this post, let us compare the various features of gold bonds and gold ETFs (and gold mutual funds) and assess which is a better choice.

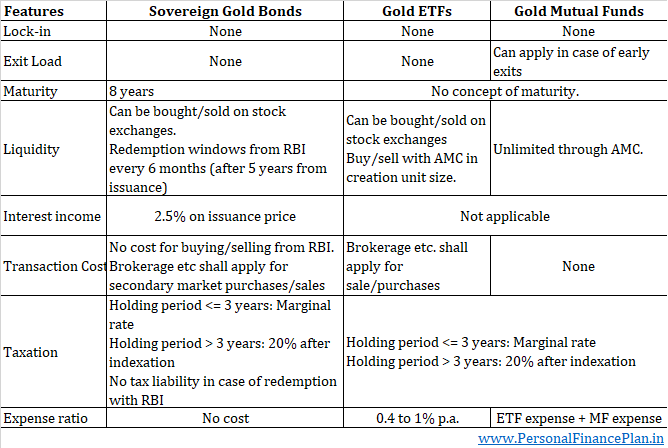

#1 Sovereign Gold Bonds vs Gold ETFs: Lock-in and Maturity

No lock-in with Gold ETFs and Gold mutual funds. No concept of maturity either with Gold ETFs or gold mutual funds. You can hold these investments for life.

Gold ETFs do not have any concept of exit load either. Gold mutual funds may have a minor exit load for early exits.

When it comes to gold bonds, there is no lock-in technically. You can always sell the bonds on the secondary market. No exit penalty either. However, if you hold the bonds in physical format (and not in demat format) and do not want to convert them to demat format, you will have to wait until premature withdrawal windows or maturity to get your money back.

Moreover, gold bonds will mature in 8 years (from the date of issuance). Therefore, you can hold for life. Subsequently, if you wish, you can invest in another tranche of gold bonds.

Slight edge to Gold ETFs

#2 SGB vs Gold ETFs: Liquidity

Gold ETFs must be bought and sold in the secondary market (unless you are a big player and can buy/redeem directly with the AMC).

Gold Bonds, on the other hand, can be bought from both primary and secondary market. Even when you want to exit, you can SELL on the secondary market or REDEEM from RBI at specified time periods.

Purely from the point of view of secondary market liquidity, gold ETFs will likely do better because there are only a few ETFs (10-12 at present).

On the other hand, there are 50 gold bond issues already and RBI adds a new gold bond issue every month. Therefore, the demand and supply for gold bonds may be spread across various gold bond issues. You can find volumes for various bond issues on NSE website. Some bonds have higher volumes than others.

Note: I have seen gold bonds traded both at discount and premium to the underlying gold price. Ideally, gold bonds should trade at a premium to the underlying gold price because of the additional interest component. But the markets are markets. There are many other factors involved that affect demand and supply. We discussed some of those factors in my post on buying gold bonds in the secondary market.

By the way, gold ETFs will also have an issue of Price-NAV difference.

Gold ETFs are the likely winner here.

Gold mutual funds may be an even better choice here since you buy from the AMC and sell to the AMC. And the AMC must offer unlimited liquidity.

#3 Sovereign Gold Bonds vs. Gold ETFs: Interest income

Sovereign Gold Bonds are a clear winner here.

You earn an interest income of 2.5% p.a. on gold bonds. Note that the interest rate on each tranche may be different. When the gold bonds were launched in 2015, the interest rate used to be 2.75% p.a. RBI has been issuing the recent tranches at 2.5% p.a.

Please understand you may buy Sovereign gold bond from the secondary market at a price different from the issuance price. The interest is calculated on the issuance price of respective gold bond (and not your purchase price). For instance, RBI issues a gold bond tranche at Rs 5,000 per unit. You manage to buy the same gold bonds at Rs 4,500. The interest will be calculated on Rs 5,000.

No other form of gold investment (physical gold, gold mutual fund, golf ETF) provides you interest income.

Winner: Sovereign Gold Bonds

#4 Gold ETFs vs SGBs: Taxation

The taxation is the same for gold ETFs, Gold mutual funds and Sovereign gold bonds.

If you sell before holding for up to 3 years, the resulting capital gains are taxed at your marginal tax rate.

If you sell after holding for over 3 years, the resulting capital gains are 20% after indexation.

However, the SGBs have two additional favourable tweaks:

Firstly, there is interest income that gets taxed at your marginal rate.

Secondly, in gold bonds, you can exit your position in two ways. Selling or Redeeming.

You SELL Sovereign Bond to a fellow investor. You REDEEM the SGB with the RBI.

The gains from SGBs are taxable only if you SELL to a fellow investor.

The redemption with the RBI (either on maturity or at specified premature withdrawal windows) is exempt from tax. And this gives gold bonds a big advantage if you are a long-term investor. You buy at 2,000 and on maturity the gold bond price is 5,000. Technically, you have a gain of Rs 3,000. However, such gain will not be taxable.

No way you can avoid this tax on such capital gain in gold ETFs or gold mutual funds.

Winner: Sovereign Gold Bonds

#5 SGBs Vs. Gold ETFs Vs. Gold Mutual Funds: Expense Ratio and Returns

Both Sovereign Gold Bonds and Gold ETFs (gold mutual fund) track the price of gold. Thus, any difference in performance will come on account of higher expenses or transaction costs.

Gold ETFs charge management fee. The expense ratio of gold ETFs can vary from 0.4% p.a. to 1% p.a. This will create a drag on the performance.

Point to Note: If you explore websites such as ValueResearch, you will see that gold mutual funds have low expense ratios (compared to Gold ETFs). However, gold mutual funds usually invest in their own gold ETFs. For instance, HDFC Gold Fund will invest only in HDFC Gold ETF. Therefore, a gold mutual fund will have dual incidence of costs. Their own expense ratio and the expense ratio of the ETF.

When gold mutual funds or gold ETFs buy gold, they must pay GST (3% currently). While they can get input credit for the GST paid, this is still a drag on the performance. I have not been able to estimate the impact. Please understand GST is applicable when ETFs buy gold (and NOT when you buy gold mutual funds or gold ETFs).

Additionally, in case of gold ETFs, there can be transaction cost (brokerage etc) and potentially impact cost if you buy in the secondary market.

You can see the impact. Look at the underperformance of Nippon India Gold BeES against domestic gold prices.

In contrast, sovereign gold bonds will mirror the price accurately (at least if you buy from the primary market and redeem with the RBI).

No expense ratio in Sovereign Gold Bonds. No GST is applicable when you buy Sovereign gold bonds. No transaction cost or impact cost either if you buy in the primary market and redeem with RBI.

Lower cost of SGBs and interest income will translate to better returns over gold ETFs and gold mutual funds.

Winner: Sovereign Gold Bonds

Here is the summary of the comparison.

Which is a better choice?

Gold ETFs and gold mutual funds score better when it comes to flexibility (lock-in and maturity) and liquidity.

Gold Bonds provide additional interest income and score slightly better in terms of taxation too. Due to lower costs, gold bonds will likely provide much better returns than gold mutual funds and gold ETFs.

After looking at all the aspects, Sovereign gold bond is the winner over gold ETFs and gold mutual funds.

When can Sovereign Gold Bonds fail you?

When you invest in SGBs, you do not buy gold. The Government does not buy gold to back up your investments.

All you buy is a commitment from the Government of India that it will

- Pay 2.5% of the nominal value of the bond (the price at which the bond was originally issued by the RBI) per annum.

- On maturity, pay the amount equivalent of the prevailing gold price in rupees.

Essentially, the Government, in addition to the interest payments, will return you the price of Gold on maturity in rupees. And thus, the Government carries the price risk.

Gold ETFs do not. Your investments in gold ETFs are backed by purchasing actual gold.

What if the Government defaults?

Unlikely since the Government can print unlimited amount of money. Not that easy though.

However, what if Rupees crumbles (loses its value sharply) Or India experiences hyper-inflation?

The commitment by the Government is NOT to give you gold, but to give you Rupee equivalent of prevailing gold price. And rupee will be worthless in that scenario. Thus, any payment in Rupee will not matter. Rupee will cease to be a store of value. Your bank FDs or any fixed income investments will be wiped out. Only real assets such as property, gold etc (or claims on real assets such as equity) will retain value.

You might say that the Government must return the prevailing price of gold, no matter how high the price. However, by the time Government pays it and you spend it, the rupee would have lost much of its value.

Of course, this is a hypothetical scenario. Quite far-fetched. But such episodes of hyperinflation happen more frequently than you think. Here are a few episodes of hyperinflation in the past century, the most notable being in Germany post World War I.

Contrast this with physical gold. That physical gold will still retain its value against say the USD. You can migrate to another country with your gold and exchange your gold for a stable currency. I understand it is not easy to take gold out of the country. However, even if you were to stay in India, your physical gold will be a good store of value (will retain its value against other assets) until the Government figures out a new stable currency. Perhaps, gold will become currency then (for a short period).

In fact, gold ETFs might be a better option than gold bonds in such a scenario because your investment is backed by gold. There is also a possibility that you can convert your physical units into actual gold. Moreover, gold ETFs do not have maturity associated. So, you can opt to hold these units until the country tides over the crises. Gold bonds have a maturity date.

I do not want to indulge in fear mongering. These things are much more complicated than I would like to believe. Many second, third and higher order effects will come into play. My knowledge or grasp of such matters is rather limited.

By the way, I do not think India will go through such a phase. Thus, I have all my gold investments in Sovereign gold bonds. And even if such a thing were to happen, we will have much bigger problems to manage. Law and order will be a mess. Widespread panic. Many institutions will fail. The intent is merely to highlight a scenario where holding physical gold scores over SGBs.

6 thoughts on “Gold ETFs Vs Sovereign Gold Bonds”

very useful information to start a new finance plans.

Very well explained Deepesh. Continue your good work. Best wishes,

Thanks Varararajan!

Very good article. Do we need to pay accrued coupon (dirty price) if we buy SGB in secondary market just like in the case of any other bond ? If yes (most likely), it is a bit more expensive to buy SGB in secondary market compared to the subscription to the fresh issue by Govt. Fresh issue avoids this accrued coupon and also gives 50 rupees additional discount for online subscription and payment. While the fresh issues are not readily available at all times, but they do come atleast monthly once. That’s why may be SGBs are more illiquid in secondary market. So SGBs are best leave till maturity and for any short term investments and trading ETFs are best.

Hi Prabhakar,

Thanks!

SGB sometimes (not always) even trade at discount to the underlying gold price. So, that tells you the pricing is not efficient.

Even when it trades at a premium, it does not seem that accrued interest is properly accounted for.

There is okayish liquidity in some of the issues. Try SGBAUG28.

Yes, frequent primary issuances can affect not just the liquidity but even the prices in the secondary market.

Wrote about this in this post.

https://www.personalfinanceplan.in/buy-sovereign-gold-bonds-stock-exchanges/

Thanks for sharing this amazing article.