Is this a good time to invest? Are the markets too cheap or expensive?

Let’s look at historical data to get a perspective.

In this post, let’s look at Nifty PE levels and see if this provides some information about prospective/future Nifty returns.

I have considered Standalone P/E of Nifty 50 as reported on the NSE website. You can download the complete data from this website. Note many Nifty 50 companies have subsidiaries but the earnings from such subsidiaries are not considered in standalone numbers. P/E based on consolidated earnings would have been a better indicator but NSE does not publish Consolidated P/Es. Hence, we must rely on standalone P/Es.

This data is for Nifty 50. There are many other indices and you can do a similar exercise for such indices too. Similarly, NSE also reports other ratios such Price-to-Book (P/BV) and dividend yields, and you can do a similar exercise for these ratios too.

I picked the P/E ratio because this is the one that most of us relate to. You must not base your investment decisions on P/E of Nifty alone. If you are interested in a specific stock (and not in a diversified fund or an index fund), you will have to dig deeper. You can’t just rely on market P/E or even the stock P/E to make the investment decision. The earnings can be misleading and are also easier to fudge. The earnings can be cashless. For instance, sales can go up along with a much higher jump in account receivables. Therefore, with stocks, you clearly need to look beyond Price-Earnings. For the market indices, I hope that the averages will take care of the issues with a few stocks in the index. Thus, P/E of the market index is more reliable for diversified investment (not for stock-specific investment).

Does the current Nifty PE level tell anything about Nifty future returns?

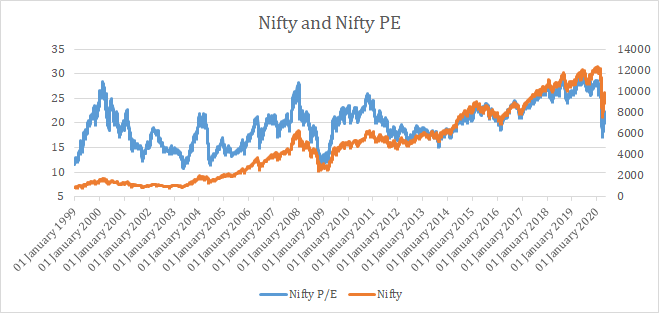

I plot the Nifty P/E and Nifty 50 level (price index) for every day since January 1, 1999. This gives a total of 5317 data points.

We can already see high Nifty PE are followed by fall in Nifty levels.

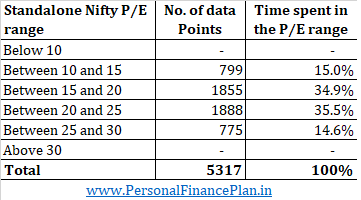

Next, let’s see how much time Nifty spends in various P/E ranges.

As expected, Nifty spends (has spent) most time in the middle ranges and only about 30% time when the P/E levels are below 15 or above 25.

Subsequently, we look at the 1-year, 3-year, and 5-year average future returns from for each of the trading days (starting Jan 1, 1999) and compile the data for various investment horizons for various P/E ranges. The returns shown are annualized. There will be a greater number of data points for 1-year returns than 5-year returns because Nifty levels after April 2015 wouldn’t have completed 5 years.

Note this data is for future returns i.e. for January 30, 2010 (and the PE level on that day), we calculate the return from January 30, 2010, to January 29, 2011 (1-year return), January 29, 2013 (3-year return) and January 29, 2015 (5-year return).

You can see the average and median (future) returns fall as we move from left to right (Lower PE to Higher PE) for all the time windows. While maximum and minimum returns are not as meaningful, those also fall as you move from left to right. Thus, investing in the Nifty index when the PE is low has been rewarding until now.

In the below graph, I just copy the data from the above table for average returns (axes are changed). You can see that the average returns fall as you go from top to bottom.

By the way, the mean PE since January 1999 is 19.95.

How to use this information about Nifty PE and returns?

When you go through the above tabulations, a few things are clear.

When the markets are expensive, you can expect prospective returns to be low.

Similarly, when the markets are cheap, you can expect future returns to be high.

In the following chart, I plot the Nifty PE levels and the Nifty future returns (1-year, 3 year, and 5-year) for every trading day since January 1999.

As you can see, when the Nifty PE (in red) is high, the future returns are low and vice-versa.

Remember nothing is guaranteed (you can only expect).

History does not repeat, but it does rhyme. This is a quote often attributed to Mark Twain. With respect to markets, it makes a lot of sense.

When the markets are expensive, they will eventually figure out a reason to fall. A word of caution, before the tide reverses, the stocks (markets) can get even more expensive.

On the other hand, when the markets are cheap, they will eventually figure out a reason to rise.

The reason will be different every time and it will take different lengths of time, but it will happen. The assumption is we are talking about a country with good social, legal, and political dynamics, otherwise there is no floor on the downside.

You can use this information to make minor tweaks to your target asset allocation.

For instance, let’s say you work with a flexible range of 40-50% equity allocation. When the P/E is high (say above 25), you might want to be on the lower end of this range. Alternatively, when the P/E is low (say around 15 or below), your equity allocation can be towards the higher end of the allocation.

An eye of PE levels can help avoid grave mistakes too. Having 80% equity allocation when the Nifty PE is over 25 is clearly not wise if history is anything to go by.

I am talking about small adjustments and not binary decisions. In my opinion, binary decisions about asset allocation are likely to be counterproductive over the long term. By binary decision, I mean exiting equities when the P/E is high and a remarkably high allocation to equities when the P/E is low.

John Maynard Keynes once said, “Markets can remain irrational longer than you can remain solvent.” Thus, the markets can remain expensive or cheap for long periods. In fact, cheap can get cheaper and expensive can get more expensive (This happens very often with individual stocks). If you take binary asset allocation decisions, this can test your patience. Even if you are not leveraged, this can compromise your investment discipline. Waiting on the sidelines (because you think markets are expensive) while everybody else makes money is not easy. This can play tricks with your mind, even if you are very smart.

You might also want to look at this data in manner. When the market is above 25 PE, the average 5-year return is only about 3% p.a. Maximum 5-year return is 7% p.a. While there is no guarantee that this will repeat, the data still indicates that the risk-reward is not in favour of equity investments at high PE levels. Let’s say if the 10-year Govt. Bond yield at the time is about 6-7% p.a., is this risk of equity investment really worth it? I don’t think so. Hence, you might want to go slow on equities.

By the way, you can also use moving averages for tactical asset allocation or any other ratios to make a similar judgement. However, it is easier to make changes to your portfolio if we base it on things that we relate to. If you have never studied technical analysis and don’t believe in it, you won’t be comfortable making changes to the portfolio on the basis of moving averages. P/E is a ratio that most people relate to and we can see above that it works.

The current Nifty PE (May 12, 2020) is 21.21.

What do you plan to do with your portfolio?

8 thoughts on “What does Nifty PE indicate about future returns?”

Great analysis Deepesh, as usual!

Would it be easy for you to do this analysis for more granular PE ranges? If it’s just a matter if tweaking some parameters in your scripts then it might be worth it.

I think so because 5 is a big range and one can’t wait for PE to move this much before making investment decisions. It can take years!! e.g. how does one interpret PE of 18? What if this 14-16% avg return is mainly because of data pints in PE range 15-17? then PE 18 is actually a bad time to enter.

Thanks Rajnish!!! Glad you found the post useful.In fact, I had thought of starting with narrower ranges but didn’t want data to confess to something or try to establish correlation where none exists. Hence, went with broader (and more intuitive) ranges.

I am not sure if I would want to base my decision on whether the PE is 16.5 or 17.5.Having said that, in the next iteration, let me work with narrower ranges.

Nice Analysis !, Very Insightful.

Thanks Amol!!!

Great analysis Deepesh, as usual!

Would it be easy for you to do this analysis for more granular PE ranges? If it’s just a matter if tweaking some parameters in your scripts then it might be worth it.

I think so because 5 is a big range and one can’t wait for PE to move this much before making investment decisions. It can take years!! e.g. how does one interpret PE of 18? What if this 14-16% avg return is mainly because of data pints in PE range 15-17? then PE 18 is actually a bad time to enter.

please ignore above comment, it’s a duplicated. Re-posted by mistake. sorry!

Nice analysis.

Another point to notice, and I believe super important to stress on, is that as investment horizon increases (1y to 3y to 5y in above post), difference in returns narrows down. It would be interesting to see 20 year returns.

Point is PE becomes less important as investment duration increases. Of course it’s still quite important and if there is no hurry then avoid high PE and do jump in on low PE.