In this post, I will focus on certain aspects of capital gains taxation for non-resident Indians (NRIs). Even though the rate of capital gains tax is same for residents and non-residents, there are a few differences that affect taxation for NRIs.

- Tax exemption limit for NRIs is Rs 2.5 lacs irrespective of age.

- In case of Resident Indians, the tax exemption limit is Rs 2.5 lacs (< 60 years), Rs 3 lacs (>=60 and < 80) and Rs 5 lacs (>=80)

- Interest income on NRO account is taxed at marginal income tax rate.

- Interest income of NRE or FCNR accounts is exempt from income tax in India.

- Capital gains tax rate for NRIs is same as that for residents.

- Short term capital gains (holding period<=1 year) on the sale of equity/equity funds are taxed at flat 15%.

Long term capital gains (holding period > 1 year) on sale of equity/equity funds are exempt from tax.Long term capital gains on the sale of equity/equity funds (in excess of Rs 1 lac per financial year) will be subject to a tax of 10%. This was introduced in Budget 2018.- The aforesaid capital gains tax on equity/equity funds applies to only those units on which Securities Transaction Tax (STT) has been paid (under Section 111A).

- Short term capital gains (holding period <= 3 years) on the sale of debt mutual funds/gold/real estate etc are taxed at your marginal income tax rate (as per income tax slab). For real estate, the holding period for the capital gains on sale of property to qualify as LTCG has been reduced to 2 years (introduced in Budget 2017).

- Long term capital gains (holding period > 3 years) on the sale of debt mutual funds/gold/property etc are taxed at 20% after indexation. There are a few assets such as listed bonds or tax-free bonds where long term capital gains are taxed at flat 10% (without the benefit of indexation). Go through this post for more on long term capital gains tax.

Set off of Capital Gains against the Basic Tax Exemption limit

The treatment depends on the type of capital gain.

1. Short-Term Capital Gains on sale of equity/equity mutual funds

Set off against the basic tax exemption limit is NOT available to NRIs for short-term capital gains of equity shares/equity mutual funds (defined under Section 111A).

For instance, if you (NRI) made short term capital gains of Rs 4 lacs on the sale of equity shares and have other income of Rs 75,000 in India, you will still have to pay tax at 15% on gain of Rs 4 lacs. Hence, your tax liability will be Rs 60,000 (before surcharge and cess).

In case of a resident, he/she will get the benefit of adjusting short term capital gains against shortfall in income from the basic tax exemption limit.

Example: A resident Indian makes short term capital gain (STCG) of Rs 4 lacs on sale of equity funds units and other income of Rs 75,000 in a financial year, he/she will have to pay capital gains on only Rs 2.25 lacs. His total income (excluding STCG on equity funds) is only Rs 75,000. Since there is shortfall of Rs 1.75 lacs from basic tax exemption limit, this shortfall can be adjusted against short term capital gains on redemption of equity fund units. Total tax liability will be Rs 33,750 (15% of Rs 2.25 lacs).

Read: How can NRIs invest in Mutual Funds in India?

2. Long Term Capital Gains on sale of equity/equity mutual funds

Long term capital gains on sale/redemption of equity shares/equity mutual funds are exempt from tax. Hence, there is nothing to worry about.

LTCG in excess of Rs 1 lac per financial year is taxed at 10%. To understand the impact of LTCG on equity returns, go through this post.

Residents can set-off LTCG against basic tax exemption limit but non-resident can’t.

3. Short Term Capital Gains on the sale of Debt/Gold/Real Estate etc

Set off against basic tax exemption limit (Rs 2.5 lacs) long term capital gains of any capital asset (other than equity) is permitted for both resident and non-residents.

You can adjust such short-term capital gains against basic tax exemption limit.

For instance, you have short term capital gains on the sale of debt funds/property to the extent of Rs 4 lacs and other income of Rs 75,000. Total income for the year is Rs 4.75 lacs (including capital gains). The entire income will be taxed as per income tax slab. You will have to pay tax of Rs 22,500 (irrespective of residential status).

4. Long Term Capital Gains on sale of Debt/Gold/Estate etc

This treatment is similar as in case of Short Term Capital Gains Tax on equity/equity fund units. Residents can set off LTCG against basic tax exemption limit while non-resident can’t.

Rate of taxation is 20% after indexation or 10% without indexation depending upon the type of asset.

Deduction for investment under Chapter VI-A (Section 80C to 80U)

There is no difference in treatment for residents and non-residents.

You can claim deduction for such investments only against Short Term Capital Gains (STCG) on non-equity investments.

For capital gains for investments defined under Section 111A (capital gains in equity/ equity funds) and Section 112 (long term capital on other assets), you cannot reduce the amount of capital gains by investment/expenses in life insurance, PPF, ELSS, health insurance premium etc.

Essentially, you CANNOT reduce your capital gains by investments/expenses made under Section 80C to Section 80U. The only exception is STCG on non-equity investments.

There is no relief under Section 80C to Section 80U when it comes to LTCG on sale of non-equity investments (debt/gold/property etc) and capital gains on equity investments.

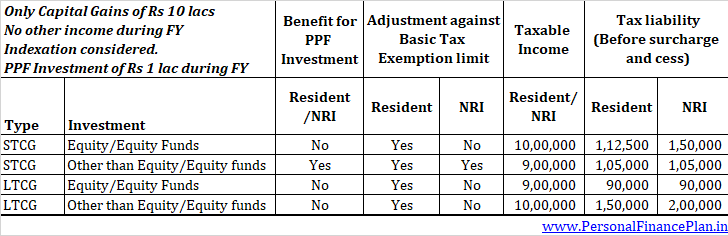

Example 1

You made short term capital gains of Rs 10 lacs on sale of debt mutual funds/gold/property. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You can take benefit for investment in PPF for short term gains on equity investments. Hence, total taxable income will become Rs 9 lacs.

First Rs 2.5 lacs is exempt (for both residents and non-residents). You pay 10% for income up to Rs 5 lacs and 20% on income above Rs 5 lacs (till Rs 10 lacs).

Total tax liability will be Rs 25,000 + Rs 80,000 = Rs 105,000.

Example 2

You made SHORT term capital gains (STCG) of Rs 10 lacs on sale of equity mutual fund units. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF. Hence, total taxable income will become Rs 10 lacs.

Residents can adjust short term capital gains on equity MF units against basic tax exemption limit. You will pay a flat 15% of such short capital gains (over Rs 2.5 lacs).

Total tax liability (for residents) will be Rs 1.125 lacs (15% of Rs 7.5 lacs)

Non-Residents cannot adjust short-term capital gains on equity MF units against basic tax exemption limit. You will have to pay 15% on the entire Rs 10 lacs towards capital gains tax i.e. Rs 1.5 lacs (before cess and surcharge).

Example 3

You made LONG term capital gains (LTCG) of Rs 10 lacs on the sale of equity mutual fund units. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF for long term capital gains.

However, since long-term capital gains on equity funds are exempt from tax, there will no capital gains tax liability.

Since the first Rs. 1 lac is exempt per financial year, you will have to pay tax at 10% on the remaining Rs 9 lacs.

Therefore, your total tax liability will be Rs 90,000 (Rs 9 lacs X 10%).

Example 4

You made LONG term capital gains (LTCG) of Rs 10 lacs on sale of DEBT mutual fund units. The capital gains amount is after accounting for indexation. There is no other source of income. You invest Rs 1 lac in PPF. What will be your income tax liability?

You cannot take benefit for investment in PPF for long-term capital gains.

Hence, the taxable income will stay at Rs 10 lacs.

If you are a resident, you can set off such gains against the shortfall in basic tax exemption limit. You will have to pay tax at 20% on Rs 7.5 lacs.

If you are a non-resident, you CAN NOT set off such gains against the shortfall in basic tax exemption limit. You will have to pay tax at 20% on Rs 10 lacs. Capital gains tax for NRIs in this case will Rs 2 lacs.

Must Read: Income Tax and TDS Rates for NRIs

Investments in Foreign Currency

If you have purchased shares or debentures of an Indian company in foreign currency, rupee depreciation may affect your returns.

It is quite possible that you may have made gains in rupee terms but made losses in foreign currency terms. Is there a relief?

Suppose you invest 1,000 USD (Rs 70,000) in equity shares of a company at Rs 70/USD. You exit investment at value of Rs 90,000 making rupee gain of Rs 20,000. During the interim, let’s suppose the USD has moved from Rs 70 to Rs 1,00 (rupee depreciation). So, in USD terms, the value of your investment is USD 900 only. Hence, you are incurring a loss of USD 100.

For such cases, there is relief under Section 48. Your capital gain/loss will be calculated in foreign currency and reconverted into Indian Rupees for finding out capital gains.

In the aforesaid example, you will incur a capital loss of Rs 10,000 (100USD X Rs 100/USD) and not a capital gain of Rs 20,000.

Do note the relief is only for shares and debentures of an Indian company (and not for any other capital asset).

An additional point to note is that this provision can be a double-edged sword. Your gains will get enhanced in case of rupee appreciation.

Set off/Carry Forward of Capital Losses

The rules are same for both residents and non-residents.

- You CAN NOT set off income from any other head (Salary/House Property/Business/Other sources) against Short term or long term capital loss (STCL or LTCL). Only income from capital gains can be set off against STCL or LTCL.

- Short term capital losses (STCL) can be set off against both long term and short term capital gains (STCG and LTCG).

- On the other hand, Long term capital losses can be set off against only Long term capital gains (and not short-term gains).

- For capital assets where long term gains are exempt from tax, no set off against long term capital losses in such assets shall be allowed.

For instance,long termcapital losses in equity mutual funds cannot be used to set off any capital gain. This is because long-term capital gains onsaleof equity funds are exempt from tax. - In the event you do not have enough capital gains to set off against capital losses, you can carry forward the losses for the next eight years. Such losses, therefore, can be used to set off capital gains in the next 8 years.

- Both long-term and short-term capital losses can be carried forward for 8 years.

- To carry forward capital loss, you must file the return before the due date.

For more on this set-off of losses, suggest you go through the following post.

How to save Long Term Capital Gains Tax?

There are provisions under Income Tax Act that allows investors to avoid paying tax on long term capital gains. The relief is provided under Section 54, Section 54EC and Section 54F of the Income Tax Act.

Quite expectedly, the relief comes with multiple conditions. I have a detailed post on this topic. You can go through this post to find out more on this topic.

Do note the relief is available for only long-term capital gains. No such relief is permitted for short-term capital gains.

Read: How to save tax on Capital Gains from the sale of house?

Special Provisions for NRIs

In addition to general provisions mentioned above, NRI get the benefit of special provisions under Section 115-C to Section 115-I for specified assets purchased in foreign exchange.

Specified assets include shares/debentures in an Indian company, deposits with an Indian Company or securities issued by Central Government.

For a financial year, you can choose whether you want to be governed by general provisions or specific provisions (Chapter XIIA). It is entirely your choice.

If you choose to governed by Special provisions for a particular year,

- Your investment income and long term capital gains on assets (other than specified assets) are taxed at flat 20%.

- Long term gains on specified assets are taxed at 10%.

- There is no benefit of indexation.

- There is no adjustment against basic tax exemption limit and deduction for investment/expenses under Chapter VI-A (Section 80C to 80U).

Capital gains tax regime (under general provisions) is already quite benign. Hence, specific provisions may be useful only in select cases.

Points to Note

- Your income tax liability may not be over by paying capital gains tax in India. You may have to pay additional tax in your country of residence.

- You may get credit for taxes paid in India.

- For NRIs, TDS is deducted at the maximum possible rate for the transaction. For more on NRIs and TDS rates, go through this post. If excess tax has been deducted, you can claim it back at the time of filing income tax return.

Disclaimer

This is a very simplistic representation of the Income Tax laws. There are many conditions which may completely alter taxation in specific cases. Covering such conditions is beyond the scope of this post. Moreover, I am not a tax expert. You are advised not to make decisions solely on the basis of this post. You are advised to consult a Chartered Accountant or a tax consultant before making any decision.

33 thoughts on “NRI Corner: Capital Gains Tax for NRIs”

Good one, particularly examples selected made it easy to understand complex law.

Thanks Mundada!!!

Great job Raghaw! Once place where all became clear to me! Thanks!

You are welcome, Vikas!!!

I and my wife are NRI. We sold a property in India and most of the money paid in 2012 but registry was made in dec 2015. We sold the property in Octo 2017. some says I be getting short term capital gains and some say I will be under long term capital gains. Please clarify.

How can I save the maximum tax if it turns out to be short term capital gains.

Thanks

Hi Manoj,

I think you meant you purchased a property.

These scenarios are always tricky.

From this fiscal year, the holding period for a property for the gains to be qualified as LTCG has been reduced to two years. However, in your case, this will not be enough if the date of registry is considered at date of acquisition.

Suggest you talk to a good CA. He/she is the right person to guide by looking into specifics of the case.

Great job raghaw.

I am an NRI. I have purchased bitcoins in dollars from my salary and have sold it in India in INR.

So now I have to give capital tax? And on what basis it will be calculated.

Thanks

Hi Prateek,

You may not subject to Taxation both in India and in US.

In India, as I understand, you will have to pay as income from other sources.

Suggest you talk to tax consultants in respective countries.

SIR I AM A NRI LIVES IN LONDON, I HAD SOLD THE PROPERTY IN AY 2016-17 WHICH WAS PURCHASED IN AY 2000-2001, NOW I AM LIABLE TO PAY CAPITAL GAIN TAX @20%. IS THERE ANY TAX EXEMPTION FOR NRI IS AVAILABLE?

You can seek relief under Section 54. Please go through the relevant portion of the post.

YOUR QUOTE “For capital assets where long term gains are exempt from tax, no set off against long term capital losses in such assets shall be allowed. For instance, long term capital losses in equity mutual funds cannot be used to set off any capital gain. This is because long term capital gains on sale of equity funds are exempt from tax”.

Long term capital losses can be set off against long term losses from sale of mutual funds. I saw some court proceedings and judgement on this AND filed IT returns accordingly. No issues.

Hi Manimaran,

I know there are a few case judgements. I had mentioned the more accepted line.

In my other post on capital gains, I have mentioned this.

Anyways, now that LTCG on equity is proposed to be taxed, set-off will be allowed.

You will need to update the article to include the new LTCG of 10% starting 1st April.

Thanks for pointing out, Abhay.

I left India on 23.4.17 to visit my son and will be back in April 19. I am a rtd. Pensioner. I understand that my tax status will be NRI. I have rented my house in India for 19000 p.m. Is it necessary for the tenant to deduct TDS on the rent. If so what is the tax rate. Till date he did not deduct the tax.

Am

Dear Sir,

I am not the best person to answer these questions. Please contact a Chartered Accountant.

As I understand, the tenant needs to deduct TDS at 30%.

https://www.personalfinanceplan.in/nri-corner/nri-corner-income-tax-and-tds-rates-for-nris/

VERY NICE… YOU MADE SOME THINGS VERY CLEAR… HOPE YOU CAN CONTINUE DOING THE GOOD WORK..

GOOD LUCK AND GOD BLESS !

I’m an NRI living in USA. For shares sold in India, my broker deducts TDS at 15%. When filing taxes in US, i am showing cap gains from India, and calculating tax as per US laws for Cap Gains from shares. But then from total taxes calculated, I am claiming credit for taxes paid (TDS by broker) in India.

I believe this is the correct way, but can you confirm that?

thx in advance.

Broker is right in deducting TDS. The TDS amount can be adjusted with final taxes paid.

HI Deepesh,

I have few queries specific for NRI’s…on TDS

Equity fund – LTCG – Is the TDS of 10% deducted for all withdrawals or is it only if the returns are above 1 lakhs. For eg if I have 2 funds and have withdrawn profits of 90K each, will the TDS be deducted for both the funds?

Debt Fund – LTCG – Is the TDS of 20% deducted or will indexation be considered? If not do I have to file returns and claim indexation benefits?

Debt Fund – STCG – If i don;t have any income in india and have got returns if Rs 2 lakhs through debt fund. Can I claim a full refund of TDS?

Appreciate your time…

Thanks & Regards

Robin

Hi Robin,

1. yes, flat 10%. AMC does not know about your other gains.

2. As I understand, it is 20%. But I do agree, AMCs have information about indexation and can make adjustments for indexation. The timing of release of indexation numbers is an operational nightmare.

3. Yes

Thank you

I am an NRI and was holding listed equity shares for more than 8 yrs in my HDFC securities brokerage account. I sold all my holdings in September 2017 to generate capital gain (longterm) of about 3 lacs.

Will my longterm gain of 3 lacs be exempt (because its sold before 31st Jan 2018) or will it be taxed at 10% ?

Your gains are exempt since you sold the shares before January 31, 2018.

Thanks for the quick reply !

Another quick question – I failed to convert my resident savings bank accounts to NRO. I have interest income from those and I am going to furnish all of those in this years tax return as I had some short term capital gains when I sold off all equity assets from my hdfc securities account in September 2017. Is there any concern with regard to non-compliance? I am going to close my resident account at end of this year when I visit.,

thanks in advance.

Satish

I’m an NRI and I plan to invest some money in debt funds in India for short term. I understand that I would have to pay STCG tax in India, but I wanted to know if I would have to pay tax in USA as well? I know under DTAA I can get credit in USA on the tax paid in India, but how much credit will I get?

Dear Akash,

Yes, you can take credit in US for taxes paid in India.

Keep in mind that the financial years in India and US will be different. So, reporting will become a bit complicated.

hi i am, sanatan mukherjee a ordinary Indian resident i had some equity share in a foreign company(listed in London stock exchange) vary recently i sold them to my previous employer basic on their offer am i able to gate exemption u/s-112a , i got these shares from my employer as (Employee Stock Option Scheme) i hold all the share more than 12 months.

Hi Deepak,

Thank you for creating a nice informative page. If you see this message, can you confirm if my understanding is correct, for the below taxation for NRIs.

Let us say I am an NRI. I have Rs 490,000 as STCG from debt funds in an year and no other income.

1. Can I use both Basic Exemption Limit and 80c deduction for this gain? (Since STCG in debt funds is not covered under section 111a).

2. For FY2018-2019, can I use the standard deduction of 40000?

3. Am I eligible for tax rebate till 300000?

In summary, I can show taxable income as (300000 = 490000-150000(80c)-40000(std deduction)) and hence will not pay any tax?

Thanks,

BR

Thanks Mr. Roy.

1. Yes

2. No

3. No. REbate under Section 87A is only for residents.

Hi Deepesh,

One query from an NRI’s perspective on short term capital gains/losses on sale of shares (equity investments). I’m a UK based NRI and i have a securities account in India. In FY 2018-19, i booked some short term profits as well as losses on sale of shares. For the profits that i booked, full taxes @ ~18% were charged instantly from my bank account. However subsequent to that, I also booked short term capital losses on sale of shares. for the last FY, short term losses are more than short term gains. Given losses are more than gains, there is no tax liability on me.

I need your advise on how to claim the taxes back i was charged as TDS on short term capital gains.

Thank you very much in advance.

Best

Rajat

Hi i am Nitin, I am indian seaferer working on foreign going ships.

1) I want to invest in mutual funds. but as i have find that in join any broker as NRI they ask for foreign address. but in my case i work on ship so i dont have any foreign address proof.

2) Also i found that there is tax deduction as TDS in mutual funds, but what if in that that year i am unable to have NRI status as per Income tax dept. so can i ask for refund in TDS has cut more and if it possible then do adjustment as resident have facility against 2.5lack exemption.

3) Also NRO account cut the TDS at higher rate on interest approx 20 percent last time that i remember. In case if in FY i am unable to get NRI Status do my NRO account will be consider as normal saving account and Extra tax that was cut will be refunded ?

Dear Sir:

Two questions:

1. Can I use foreign exchange rate loss to offset capital gains tax? When I purchased the land in Sep 2007 USD exchange rate was Rs 40.1885; when I sold the property in Oct 2022 exchange rate was Rs 79.9557 per USD.

2. I had lost my original sales deed from my purchase of property in 2007. I had to spend over Rs 400,000 in obtaining a police “No Trace Certificate”. Can this expense be used to offset the capital gain?

Thanks

Raju Iyer