For most retail investors, mutual funds mean equity mutual funds. Well, equity mutual funds have a sibling too i.e. debt mutual funds. Though total investments under debt mutual funds are far greater than equity mutual funds (due to higher institutional participation), most retail investors don’t consider debt funds.

Primary reason is there are other financial products such as fixed deposits and recurring deposits that provide returns comparable to those provided by debt mutual funds. And there is an element of inertia and comfort too. You have been investing in fixed deposits for a long time. Debt mutual funds must offer you enough before you make the switch.

There are a few areas where fixed deposits are ahead while there are certain aspects where debt mutual funds have an edge. In one of my subsequent posts, I will do a detailed comparison between bank fixed deposits and debt mutual funds. Not in this post though.

In this post, I will discuss the debt mutual funds in detail. What are the various types of debt mutual funds? What are the elements that can affect mutual fund performance? What are the risks that a debt mutual fund faces? How are capital gains and dividends taxed?

What are Debt Mutual Funds?

Debt mutual funds are a variant of mutual funds that invest in debt securities or bonds. Debt securities include government securities, corporate bonds and commercial paper, money market instruments, certificates of deposits from banks etc.

Since the debt MF schemes invest in debt instruments, the returns are debt-like too. Any event that affects the performance of underlying debt securities will affect performance of debt funds too.

Bond prices and Interest Rates have an Inverse Relationship

When the interest rates go up, bond prices go down. On the other hand, when the interest rates go down, the bond prices go up.

Additional Characteristics of Bonds or Debt Securities

Bonds with longer maturity offer higher interest rate (coupon). So, if the bond with maturity of 2 years offers 7% p.a., you can expect the bond (from the same issuer) with maturity of 5 years to offer more than 7% p.a.

Duration is a measure of interest rate sensitivity of a bond. Duration tells you how much the price of a bond will change for a percentage change in interest rates.

If the duration of a bond is 8, the market price of the bond will go down by 8% if the interest rate goes up by 1%. On the other hand, if the interest rate goes down by 1%, the NAV of the MF scheme will rise by 8%. This is a very simplistic representation. Capital markets tend to price in a lot of information even before the event happens. For instance, bond yields may fall (bond prices may rise) in mere expectation of an interest rate cut.

Long maturity bonds have high duration and hence face the greatest interest rate risk. So, though such bonds are likely to offer high coupon (interest rate), these bonds face the greatest interest rate risk too. These will fall the most in case of an interest rate hike. On the other hand, long term bonds will rise the most in case of an interest rate cut.

Duration of a mutual fund is essentially the weighted average of duration of underlying bonds or securities that the MF scheme has invested in.

Bonds from companies with inferior financials (low credit rating) will offer higher interest rate (coupon) too to compensate for the higher risk taken by the investor. However, the risk of default on such bonds is higher too.

![]()

What are the risks that Debt Mutual Funds face?

1. Interest Rate Risk:

A debt MF scheme is merely a portfolio of underlying bonds. As discussed above, duration of MF scheme is weighted average of duration of underlying securities.

Higher the duration (interest rate sensitivity) of underlying bonds, higher the duration of debt MF scheme.

And higher the duration of a mutual fund, the greater the sensitivity of NAV to interest rate movement.

In simple terms, if the duration of a debt mutual fund scheme is 8, the NAV of the scheme will go down by 8% if the interest rate goes up by 1%. On the other hand, if the interest rate goes down by 1%, the NAV of the MF scheme will rise by 8%. Again, this is a very simplistic representation.

Based on the duration, debt funds can be classified into liquid funds, ultra short-term funds, short term funds, and long term debt funds. Then, there are dynamic bond funds, where the fund manager adjusts the duration of the scheme based on her interest rate outlook.

Liquid funds (with the least duration) have the lowest interest rate risk while long term debt mutual funds have the highest interest rate risk. In case interest rate goes down, liquid funds will go up the least while the long term debt fund will rise the most.

On the other hand, if the interest rate moves up, NAV of liquid funds will fall the least while NAV of long term funds will fall the most.

2. Credit Risk:

Mutual Funds invest in debt securities such as Government Securities and bonds issued by companies. If for any reason, the price of underlying debt securities declines or there is default on such securities, the NAV of the MF scheme will suffer.

Though you may ignore the possibility of a sovereign default (on government securities), companies can default on their debt payments.

Price of debt securities can also decline in cases of rating downgrades (this is more of price risk than credit risk though).

There are gilt funds (invest in government securities), corporate bond funds, credit opportunities fund etc. Some mutual fund scheme can hold a mix of both.

3. Liquidity Risk

The fund manager may not be able to liquidate a security due to lack of demand (low volumes). In such cases, he may be forced to hold the security till maturity. In cases of extremely redemption pressure, the fund manager may be forced to sell the security at a low price or may be forced to restrict redemptions. Hence, you may not be able to take out money even if you want to. This happened recently in case of JP Morgan debt fund.

Apart from the credit and interest rate risk, NAV of debt funds can suffer due to external events too. After all, debt mutual funds invest in bonds. If, for any reason, prices of those bonds go down, NAV of the debt MF scheme will suffer.

For instance, in mid 2013, a number of foreign investors started selling Indian debt heavily (I wouldn’t go into reasons). Basic Economics dictates that when the supply is high (people are selling) as compared to demand, prices go down. NAV of debt mutual funds took a severe beating during the time.

Essentially, funds will differ based on their interest rate sensitivity or the credit quality of the underlying securities they invest in.

So, you can have various permutations and combinations viz. short term gilt funds (low duration and high credit quality), long term gilt funds (long term and high credit quality), long term, short term corporate debt fund etc.

Where to find information about Debt Mutual Funds?

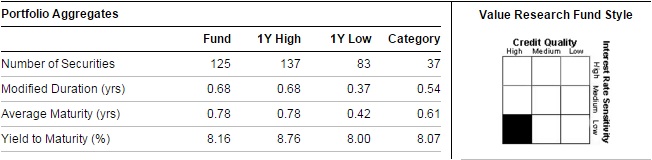

You can find information about duration and credit quality of an underlying MF scheme on ValueResearch website. There are many other websites but I will stick with ValueResearch.

Below is the snapshot for ICICI Prudential Flexible Income Plan. You can see clearly from the style box that the fund invests in high credit quality instruments and has a low duration.

ICICI Prudential Flexible Income Plan

Here is the similar information for ICICI Prudential Corporate Debt Fund

ICICI Prudential Liquid Fund

ICICI Prudential Long Term Fund

Hence, the style boxes give a very good idea about the duration (interest rate sensitivity) and credit quality of underlying securities. You can even have a look at the portfolios of the MF schemes on the ValueResearch website.

What are the Contributors to return from Debt Mutual Funds?

The return from the debt mutual funds can be broken down into two components.

- Interest Income: Underlying debt investments yield interest income that accrue to the debt MF scheme and adds to the NAV. Typically, longer the maturity of underlying bond, higher the interest rate (coupon) offered.

- Capital Appreciation: Price of underlying debt investment can rise (or fall) due to an interest rate cut (or rise) or credit rating upgrade (or downgrade) etc. If the price of underlying investment increases or decreases, NAV of the debt MF will be impacted too.

Here is the complex part. Longer the maturity of underlying bond, higher the coupon it will offer. Long term bonds will also gain more (capital appreciation) in case of an interest rate cut. However, such bonds will also fall the most in case of interest rate hike. The same argument can be extended to the Mutual funds that hold such bonds.

And yes, the return under debt mutual funds is not fixed. The return is market linked and depends on the performance of underlying securities.

There is no guarantee of positive returns under mutual funds. You can even incur capital loss on your debt mutual fund investments. I have booked losses in my debt MF investments.

But yes, since debt MF schemes invest in debt instruments only, performance of these funds is not as volatile as equity mutual funds.

Past Performance of Debt Mutual Funds

I have compiled the following information from ValueResearch (January 28, 2016). Please understand it is merely a snapshot in time and does not mean debt mutual funds will always give returns like this.

An important observation: Short term and ultra short term funds have done better across all tenors. Again, this is a snapshot in time. It does not mean short term and ultra short term funds will outperform other types of debt funds all the time.

Tax Treatment Capital Gains and Dividends in Debt Mutual Funds

In case of debt mutual funds, the tax liability arises only at the time of sale of mutual fund units.

If holding period for debt mutual fund units is less than or equal to 3 years, the resulting capital gains shall be treated as short term capital gains and taxed at the marginal income tax rate (income tax slab).

Must Read: All you need to know about Short Term Capital Gains Tax

However, if the holding period is greater than 3 years, the resulting capital gains shall be treated as long term capital gains and taxed at 20% after accounting for indexation.

Indexation is rise in cost of the asset due to inflation. The Central Government notifies cost inflation index every year. The cost of purchase is adjusted for inflation. You are taxed for gains over and above this adjusted purchase cost. The indexation benefit is applicable only to long term capital assets.

Must Read: All you need to know about Long Term Capital Gains Tax

About the dividends, dividends are not taxable at the hands of the investors. However, the MF scheme deducts dividend distribution tax (DDT) before making the payment to the investor. So, essentially, tax is paid out from your funds only.

The applicable DDT is 25% (plus 12% surcharge and 3% cess). This makes the effective rate 28.84%, which is quite high.

Debt Mutual Funds do not pay any interest. Such funds only pay dividend. And dividends are not guaranteed. Payment of dividend is at the discretion of the fund manager (or AMC). You get the dividend if you opt for the dividend option (and not growth option).

At such high dividend distribution tax, it may not make too much sense opting for the dividend option (unless you are in the highest income tax bracket). I have done a detailed post on whether you should opt for growth or dividend option. You can go through the following post.

Must Read: Mutual Funds: Growth or Dividend?

Which type of debt mutual fund is the best?

There is no crisp answer. It depends on your requirements and your financial goals.

If you are investing for a few days or weeks, you should go for liquid funds. These are the least volatile and have no exit loads. Returns will also be reasonably predictable.

If you are looking to invest for a few months or years, then go with short or medium term debt funds. The returns should be higher than liquid funds and with lesser volatility than long term funds.

If you want to bet on the favorable interest rate movement, then long term gilt funds are the best. These funds have the highest interest rate sensitivity (duration). If you feel that interest rates are headed downwards, invest in long term debt funds. But yes, it is a double edged sword. If interest rates rise contrary to your expectations, you might be staring at losses.

Long Term debt funds are not invest right and sit tight kind of funds (as equity funds are). These are tactical plays. You must time your entry and exit based on interest rate expectations. Otherwise, capital gains during interest rate down cycle will be wiped out during interest rate up cycle. Do note interest income from underlying bonds will still accrue to the debt fund.

If you want to bet on interest rate movement but do not want to do that yourself, opt for a dynamic bond fund. The fund manager will do it for you.

If you want a higher return (for a higher risk), go with credit opportunities fund or corporate bond funds.

And yes, do not just focus on duration. Focus on credit quality of underlying investments too.

How do I invest in Debt Mutual Funds?

I do not look at my debt investments to provide growth to my overall portfolio. For that, I have equity funds. I invest in debt mutual funds for stability, diversification and proper asset allocation.

I don’t like to bet on interest rate movements. To be honest, I am not sure if I am capable either.

I don’t like to invest in credit opportunities fund for a couple of percentage points of higher return.

I prefer to invest in MF schemes that fall in the bottom left of the style box i.e. the funds that have low duration and invest in high credit quality securities. I prefer short term and ultra short term debt funds that invest in high credit quality debt securities.

How do you invest in debt mutual funds?

23 thoughts on “PFP Primer: All you need to know about Debt Mutual Funds”

I have been going through lot of articles where short vs ultra short term vs long term funds are not clearly explained. I would expect you to elaborate on the same.

For e.g I want to do a regular investment on debt funds, month on month for next 10 years. What type of fund to choose? Actually a short term fund is doing good for long term. Please explain.

The term is duration i.e. interest rate sensitivity.

Short term funds have low duration i.e.such are less sensitive to interest rate movements. So, if interest rates go down, the NAV will go up less as compared to long term debt funds.

http://www.investopedia.com/terms/d/duration.asp

I prefer short term debt funds, even for long term investments.

Thanks much for the details.

Reg Clubbed income on debt/equity funds:

If we invest in a jointly held ( with my spouse ) debt/equity funds and note that the fund is invested by me alone, here. ( a. Here shall we assume 50% of investment is gifted to my spouse ? )

After 10 years or so we acquired a corpus of few crores. Now, we move the corpus into a fixed income products ( again a joint account ) as regular income for our family, say retirement.

Here, how the income tax is derived ? Is this aggregated interest will be split into two holders and to calculate IT accordingly.

( The idea is we have to create accounts in such way that the retirement corpus can be split under two persons so that to reduce tax liabilities. )

Dear Sunil,

You have to look at this from perspective of Income Tax Department.

They don’t want to distribute your assets, save taxes on income from those assets and at the same time retain control over income from those assets.

Hence, they are ok if you gift your assets to a complete stranger since you are losing control over income.

Same can’t be said if you distribute your assets to your spouse. Hope you get the idea.

Since you are the source of funds and you are expected retain control of the income from those assets even if you gift your wife (or open joint accounts), her income will be clubbed with yours and you will have to pay tax.

It becomes very easy to save tax if Government does not club such income.

I am planning to do a post of clubbing of income in the next few months. Perhaps, you will get much crisp answers in the post.

Tax Men cannot execute the law at their own discretion!.

Tax Act explains that, returns earned from the returns of the investment is considered as income of the received party. So, one’s spouse will completely own the part of the corpus as received.

If IT dept cannot agree due to their own power, then I have to be strong enough in my documents. Say, no joint accounts in any products and gifted amount…those respective signed papers ready etc

( Joint accounts help in lot of cases, but here I have to sacrifice it.)

Btw..Do you have any reference to Auditor-Paid Service, so that I can get clarified/procedures to proceed on this.

It is written in tax laws. They will go by what is written. And no amount of supposedly watertight documentation can stop them.

They are merely following the law.

I am sure there are ways to save tax. Just that Income Tax law has a view on such distribution of assets to spouse, minor children and daughter in law. I provided the reason in my previous comment.

But yes, would suggest you talk to a tax expert. They will have practical experience and will be able to guide you better.

Talk to any local good CA. They can also help in case of any scrutiny.

You can also talk to guys at ClearTax. I have never interacted with them but I think they are good.

It should not be very expensive either.

thanks a ton for clarifying the basis of classificatin of funs – int rate sensivity or duration. So short term debt funds can work otu for long term investing too.

!

Yes, I prefer short term debt funds even for long term investments. Much less volatile than long term debt funds. Gains made in long term debt funds during an interest rate down-cycle will be wiped out during an interest rate up-cycle.

1. What about investing in Gilt Funds – Short Term Category, forecasting softening of interest rates say just for 6 months period to get better than FD rates

2. I could see SBI Gilt Fund – Short Term grows constantly for last three years irrespective of interest rate movements !! ??

>> https://www.valueresearchonline.com/funds/newsnapshot.asp?schemecode=899

NAV>>

https://www.personalfn.com/tools-and-resources/mutual-funds/NAVHistoryDetails.aspx?HistNavSchemeId=9d9fc79b-bc2e-4a55-b88d-b5506a834bc9|SBI%20Magnum%20Gilt%20Fund%20%20Short%20Term%20%20Growth

Dear Sunil,

Short term funds have low duration and hence are less susceptible to interest rate movements.

Personally, I like short term gilt funds.

In this case, we can prefer Short Term Gilt over Short Term General Debt funds, for a long duration of investment, being double digit returns

With gilt funds, there is little risk of default (credit risk). With other funds, credit risk may be higher.

Personally, I do not expect returns on short term debt funds to be very high (double digit) in the immediate future.

( Due to domenitization )Being more liquidity pumping into the system, we can expect deposit rates to go down in the market and so increases in the gilt/debt fund value.

And how the nav value will increase ?, meaning whether the change happens in single day or gradually, in reacting to interest rate fall.

Hi Sunil,

It is not so simple. Underlying securities are market-linked. Expectations typically get already priced in anticipation of an event. Hence, when the actual event happens,there may not be any major impact. It can be both ways, gradual or in a few days.

But yes, the increase in NAV due to accrual of interest will be gradual.

May be I am not getting it. The nav change due to drop in interest rate ( not the regular accrual ) is gradual or was it gone up, already due to expectations of the event ?

Can you explain the terms and impact on returns…

Modified duration

Yield to maturity

Avg maturity

Modified duration and avg maturity are measures of interest rate sensitivity of debt MF portfolio. Higher the duration or maturity, greater the sensitivity.

YTM is the return you get (including coupons and capital appreciation) if you hold the bond till maturity.

In general, when NAV is not declared, does it mean the fund is not growing on those days , a kind of investment is idle on those days?

Please explain. ( Liquid/ Dept /Equity fund categories )

Dear Sunil,

NAV is not declared on weekends and on market holidays.

For equity funds, NAVs can’t change.

For debt funds, the interest will accrue and will reflect when the market opens next.

I hope I got your question right.

Thanks for the details. Seems debt funds and liquid funds have different OFF days.!

Btw.. Debt Fund and Liquid Fund interest rate for a given period of years, to be calculated as ‘Day wise cummulative’ right ?

You are welcome, Sunil.

Interest does not have an off day.

1. OFF Days..I meant non declaration days.

2. If we calculate interest calculation, whats the mode of cummulative to be chosen say daily/monthly etc.

3. We have lot of names like flexible income plan, treasury , savings fund etc but hope all falls under Short term , ultra short term etc. How to identify the category ?

Cumulative calculation won’t work with traded securities or if the underlying securities are traded in the secondary market.

There is no standard nomenclature. Read the scheme information document for better clarity. There is no other way.