Many of us rely on interest income for our regular cash flows. A few can’t look beyond such investments.

However, are you aware how your interest income is taxed?

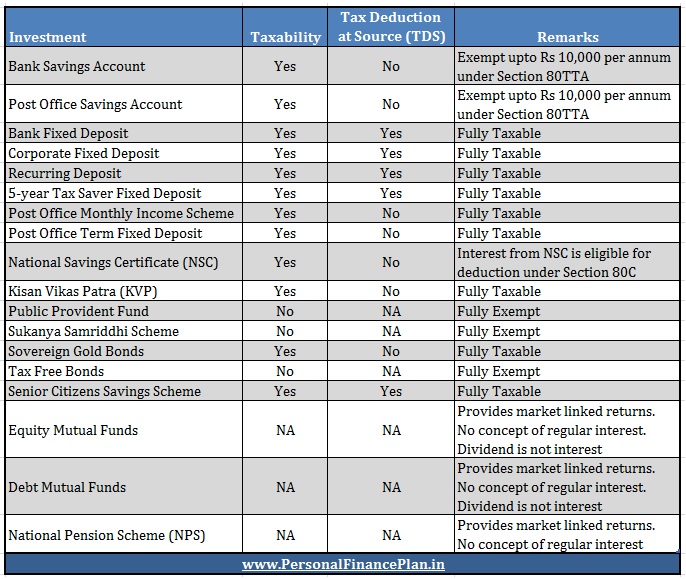

Taxation of Interest Income for various Investments

The tax treatment of interest income varies across investments. Clearly, a few investments receive favourable treatment as far as taxation of interest income is concerned.

For instance, interest income from PPF account and tax-free bonds is exempt from income tax while interest income from bank fixed deposits is taxed at your marginal rate of income tax (slab rate).

In this short post, let’s look at how interest income from select investments is exempt from tax while the interest income is taxable for other investments.

You can see some of the investments such as equity and debt funds and NPS do not offer interest income. Hence, the returns from investments are not taxed as interest income.

For equity and debt mutual funds, the returns are market linked and are taxed as capital gains.

NPS does not provide interest income either and provides market linked returns. The taxation of NPS proceeds is quite different.

To be honest, the earlier table shouldn’t have had equity and debt MFs and NPS in the first place. However, I thought it will be better to have such investments here.

What about TDS?

For Tax deduction at source, TDS is deducted only once the interest income per annum exceeds a certain threshold.

Moreover, if your total income during the year falls below minimum tax exemption limit (Rs 2.5 lacs for age < 60), you can avoid TDS by submitting Form 15G/15H.

What should you do?

Even though a few investments enjoy favourable tax treatment, your investment decisions shouldn’t merely be driven by tax considerations alone. For instance, even though PPF offers good returns and tax-free interest, it is not a suitable investment if you need the money after 3 months.

In such a case, a fixed deposit will be better choice.

Keep your goals in mind too.

If you liked the post, your friends may like it too. Please share with your friends.

Disclaimer

I am not a tax expert. Therefore, you are advised to consult a Chartered Accountant.

Book Suggestion: Retire Rich Rs 40 a day (P V Subramanyam)

18 thoughts on “How is Interest Income from your Investments taxed?”

Good post. Information is clear, concise and useful too.

Thank you sir.

Will request you to share the posts with your friends on Facebook and Whatsapp so that they can also benefit.

Hello Deepesh,

My father is going to retire this year and would be collecting about 35 lakhs in arrears & other benefits.

1. How will it be taxed (Percentage) if he puts all of it in 4 -5 bank FDs?

2. How will it be taxed (Percentage) if he puts the lumpsum in SWP in 4-5 equity MFs ?

Karunya

Hi Karunya,

Tax treatment of arrears is a bit complicated. Income of previous years may also have to be considered. A CA will guide you better on taxation of arrears.

1. FD interest is taxed at marginal income tax rate.

2. SWP from an equity fund is an extremely bad idea. SWP should be set from debt funds. In case of debt funds, capital gains tax liability arises only at the time of redemption. If redeemed before 3 years, the resulting gains at taxed at marginal income tax rate (slab rate). After 3 years, it is 20% after indexation.

Please understand debt funds come in multiple variants and it is not difficult to select a wrong category of debt funds.

Seek professional help if required. Mistakes after retirement can be extremely damaging.

Suggest you to go through the following posts.

https://www.personalfinanceplan.in/mutual-funds/why-systematic-withdrawal-plan-swp-from-equity-funds-is-a-bad-idea/

https://www.personalfinanceplan.in/mutual-funds/bank-fixed-deposits-vs-debt-mutual-funds/

https://www.personalfinanceplan.in/mutual-funds/bank-fixed-deposits-vs-debt-mutual-funds-part-ii/

Thanks Deepesh for the lengthy clarification and for your patience !

I shall consult a CA and go through your posts as well.

Perhaps you can do a post on how & where to invest a lump sum amount in the future for the benefit of us all 🙂

Karunya

You are welcome, Karunya.

Please share the post with your friends.

Sure, will think about it.

Thanks Deepesh. Its valuable information. I like to know more about tax free bond . And how to start equity with small amount..

You are welcome, Indu.

Interest from tax-free bonds is exempt from tax.

If you have no prior experience in equity markets, suggest you start with equity funds.

Please consult a SEBI RIA or a financial planner.

My Jeevan Surekshwa policy is matured and I am getting monthly pension.

I have been including this sum in my Total Income of year for tax purpose.

Is it correct?

Yes, that’s right.

I am a prospective investor and was looking for profitable options to invest. I wanted your views about Peer to peer lending and is it a viable option to invest?

High risk, high reward debt investment approach.

One can take some exposure to the Peer-to-peer lending.

Interest accrued on NSC is taxable , but how to include broken period interest.? Several calculators available on internet but they give int accrued at the end of completed year.

I have purchased NSC VIII issue (5 years) on 19Jan2012. matured on 19Jan 2017.

This year eligible taxable interest will be from 1April 2016 to 18Jan 2017. Am I right? if yes there is no calculator available for arriving at broken period interest

Hi Pradip,

How did you file for the last year? You reported the entire year premium, right?

YES . Last year was full year hence interest accrued for whole year was due, but this year it is broken period..

I have read on internet that due to complexity of calculations broken period to be ignored and whole year is to be reckoned . Likewise first year broken period is to be ignored and last year broken period to be treated as full 5th year,

However I am not sure about correctness of this information

Dear Pradip,

I am not so verse with taxation aspects.

In my opinion, you should have reported the entire NSC interest over the years in some return or the other.

For the this year, you just need to report Actual interest earned – Interest already reported.

A good CA is a better person to answer this question.

hi

i want clarification on rate of income tax on interest on capital gains earned/accrued in a financial year ..what is the rate of income tax if i have taxable income from salary in the same financial year .

Capital gains taxation (except short term gains on non-equity investments) is independent of your salary or other income (with some relaxations if the income is below minimum limit).

Interest income will be added to your income and taxed as per your marginal tax rate.