The tax on LTCG from equity funds was introduced in Budget 2018. This made ULIPs attractive to a number of investors. The insurance companies have jumped onto this opportunity and have launched a number of Unit-Linked Insurance Plans or ULIPs.

In this post, let’s look at the two broad categories of ULIPs. Type I and Type II ULIPs. The only difference between the two types of ULIPs is in the death benefit. The death benefit defines the amount that the nominee (under the policy) gets in the event of demise of the policyholder during the policy term. However, this difference in death benefits also impacts the returns of the two types of ULIPs.

How ULIPs work?

Unit linked insurance plans (ULIPs) are insurance products that provide the dual benefit of insurance and investment. A ULIP has many charges. Some of the charges (premium allocation, policy admin) are recovered upfront from the premium while the others (mortality charge) are recovered through the cancellation of fund units.

Sum assured is the minimum amount that one gets in the event of the death of the policyholder. Investors/policyholders are offered various investment options (equity, debt, balanced etc). You can choose the investment fund as per your requirement. The value of your investments (“fund value”) grows over a period of time through regular premium payments and the return on your investments.

ULIPs can be broadly classified into two types: Type-I and Type II ULIPs.

Death benefit under the two types of ULIPs

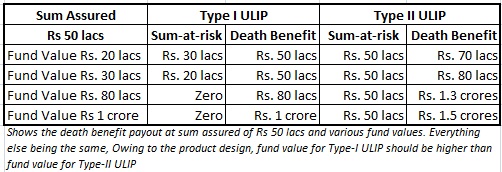

Type-I ULIP

In the event of the death of the policyholder, the insurance company pays the higher of fund value or sum assured to the nominee/beneficiary. Suppose a person has paid the premium for 8 years, the fund value has grown to 30 lacs. The Sum Assured is Rs 50 lacs. In the event of the death of the policyholder, the beneficiary will be paid Rs 50 lacs (higher of 30 lacs, 50 lacs).

Type II ULIPs

In the event of the death of the policyholder, the insurance company pays the sum of fund value or sum assured to the nominee/beneficiary. Considering the same scenario, the beneficiary would have received Rs 80 lacs (Rs 30 lacs + Rs 50 lacs)

How does this impact the return?

Among other charges, an insurance company charges a mortality charge on sum-at-risk for the insurance company. The Sum-at-Risk is the amount insurance company will have to pay from its own pocket in the event of the death of the policy holder. Expectedly, the higher the sum-at-risk, the higher the mortality charge. Additionally, the mortality charge increases with the age of the policyholder.

Under type I ULIP, since the insurance company only needs to pay the higher of the fund value and sum assured, the sum-at-risk goes down as the fund value grows. Considering the above example, if the fund value after 5 years is Rs 20 lacs, the sum-at-risk will be Rs 30 lacs (Rs 50 lacs – Rs 20 lacs). This is because in the event of the death of policyholder, the insurer needs to pay only Rs 30 lacs from its pocket. Rs 20 lacs is already there with the company in the form of fund value.

If the insured event (death of the policyholder) occurs after the fund value has grown to Rs 30 lacs, the sum-at-risk for the insurance company will go down to Rs 20 lacs. If the fund value grows to Rs 50 lacs (or higher), there is zero sum-at-risk for the insurance company. This is because its entire liability (Rs 50 lacs or higher) can now be met through fund value only. Therefore, under Type I ULIP, sum-at-risk keeps decreasing as the fund value grows and eventually becomes zero. As sum-at-risk keeps decreasing, the mortality charge also goes down and eventually goes to zero.

On the other hand, in the case of a type II ULIP, sum-at-risk is constant (sum assured) during the term of the policy. Therefore, the mortality charge does not go down and infact increases every year as the policyholder ages.

Thus, the investor/policyholder pays much lower mortality charges in a type-I ULIP. Since your returns are net of all the charges including mortality charges, Type-I ULIP provide better return due to lower incidence of mortality charges.

Under Type-II ULIPs, sum-at-risk remains the same and hence mortality charges are higher. This impacts the returns adversely. Thus, type-I ULIPs offer better returns than type-II ULIPs (everything else being same).

PersonalFinancePlan Take

Type-I ULIPs offer far superior returns than Type-II ULIPs if the policyholder survives the policy term. However, Type-II ULIPs perform far better if the policyholder passes away during the policy term.

You can go through our ULIPs vs MF + Term Insurance for comparison. So, which one is better? One provides better maturity benefits (policyholder survives the policy term) while the other provides better death benefits.

To answer the question, you have to look at why you purchase insurance products.

If you want to invest in a ULIP purely from an investment angle, Type I ULIP is better.

If you want to invest in a ULIP and get good life coverage too, Type II is better. However, you must note you can purchase life cover through a term insurance plan at a much cheaper cost.

I prefer that you keep your investment and insurance needs separate. However, if you must invest in a ULIP, I suggest that you invest in a Type-I ULIP. Ensure that you have adequate life cover.

5 thoughts on “Variants of ULIPs you must be aware of”

How could one conclude that, how much preuimm allocation charge should be paid. as u say it varies 5% 70%.I’m looking forward to takn an ULIP CAPITAL BUILDER by Max Newyork, they r asking for 30% Premium Allocation Charge. Also at last how to conclude that they r not cheating there commission from our Premium.

Charges for ULIPs have come down significantly. IRDA has imposed strict guidelines to cap charges. So, you don’t have to worry much. Premium allocation charges (and all other charges) are specifically mentioned in the policy brochure or document. You might be better off investing in mutual funds and purchasing a pure term cover rather than buying a ULIP.

Dear Deepesh,

I was looking for resources that help me with financial decisions and ended up reading very informative posts. I am 40 and yet to make big financial decisions other than fixed deposits and less risky routes. Recently, I was approached by agent with SBI smart scholar ULIPs suggesting it will help to plan daughter’s education. He came at a point when I was thinking about SIPs and mutual funds (no experience so ever). From his pitching I thought it might be good product and to start investing in equity and bonds (not thinking as an insurance product). From reading your post, I clearly understood types of ULIPs and charges (big thank you for educating us!). I am wondering SBI smart scholar come under category of type 2 with a crux that higher of sum insured or fund value in case of death after 5 years (but before 18 years) + fund value paid at age of 18. If the person’s survive then only the fund value at age of 18 . It is not clear whether this offer only better death benefits rather than better returns (because of charges).Since the fund value is tax free, would it be good option for better returns too (now that taxation are imposed on mutual funds)? Or go for type 1 ULIPs (since charges are lower) assuming person survives + term insurance. Thank you.

Dear Vinod,

Do not go for ULIP (either type I or type II) if you do not need insurance.

If you need life cover, go for a term plan.

It is a typical child plan where premiums are waived off in the event of demise of the parent.

Such plans are easier to relate to. However, as always expect this plan to be expensive and have other usual problems of ULIPs.

Here is a very old post on my website.

https://www.personalfinanceplan.in/should-you-buy-unit-linked-child-plans/

For investment, explore PPF and mutual funds for long-term wealth creation. Seek professional assistance, if required.

Here is another post you must go through.

https://www.personalfinanceplan.in/ltcg-tax-equity-mutual-funds-ulips-comparison/

Dear Deepesh,

I have taken Life Time Classic (Maximiser V) from ICICI Bank. The purpose is to create a fund for my child at the time of his college. But now I can see that there are other good options also. I have paid three premiums. Please suggest whether I shall continue the same or not?.