What is the best asset allocation for your long-term portfolio?

40:60 equity:debt or 50:50 or 60:40 or 70:30 or any other allocation?

You will get the answer to this question only in hindsight. The best allocation for the next 20 years (2020-2040) will be known only after 2040 ends. You can run backtests and see what has worked the best in the past. While this gives you an idea, there is no guarantee that the same allocation will be the winner over the next 20 years.

Hence, it is better to focus on the right asset allocation for you (Suggest you read this post) instead of expending energy on guessing the best asset allocation over the coming 20 years. However, it still makes for an interesting exercise to find out which asset allocation has worked the best in the past.

The Data and The Approach

For the purpose of this analysis, I consider only Nifty 50 and Liquid. I could have added gold and international equities to the mix but let’s keep this for a later day.

I consider Nifty 50 TRI and HDFC Liquid Fund data since October 2000 and use it to construct the following 6 portfolios.

- 100% Nifty 50 TRI (pure equity portfolio)

- Nifty 40:60: 40% in Nifty 50 TRI and 60% in HDFC Liquid Fund

- Nifty 50:50: 50% in Nifty 50 TRI and 50% in HDFC Liquid Fund

- Nifty 60:40: 60% in Nifty 50 TRI and 40% in HDFC Liquid Fund

- Nifty 70:30: 70% in Nifty 50 TRI and 30% in HDFC Liquid Fund

- Nifty 80:20: 80% in Nifty 50 TRI and 20% in HDFC Liquid Fund

Portfolios from (2) to (6) are rebalanced back to target allocation every year on April 1.

Points to Note

- Over the last 20 years, Nifty 50 TRI has delivered about ~14.5% p.a. HDFC Liquid Fund has delivered 7% p.a. With such sharp difference between the returns of two assets, 100% Nifty 50 TRI will likely deliver better returns than any combination of Nifty and liquid fund. Hence, if you think asset allocation and regular portfolio rebalancing will deliver some magic (from returns perspective), you are likely to be disappointed here.

- But you can expect lower volatility (compared to pure Nifty 50 portfolio) in these combination (asset allocation) portfolios.

- Moreover, Nifty 50 did very well in the first 10 years 2001-2010. Not so well in 2011-2020. We need to see how asset allocation portfolios perform during these periods.

- I have considered the Nifty 50 Total Returns index (returns that you earn in an index fund will be after expenses and tracking error). On the other hand, I have picked up a liquid fund (after expenses). Not fair. Moreover, a liquid fund is perhaps the lowest yielding fixed income product. Other fixed income products such as fixed deposits or PPF or other debt funds would have delivered better returns. However, data about the HDFC Liquid fund is easily available. So, I just picked it up. Most other debt funds haven’t been around since the year 2000. In a way, I have given an upper hand to Nifty 50 (higher equity allocation).

- I assume the portfolio rebalancing does not entail any transaction or tax costs. An unrealistic assumption but let’s play along.

- Further, I have considered the asset allocation portfolio as wrap products. Think of them as mutual funds that rebalance to target allocation on April 1. Again, a bit unrealistic but easy for me to analyze.

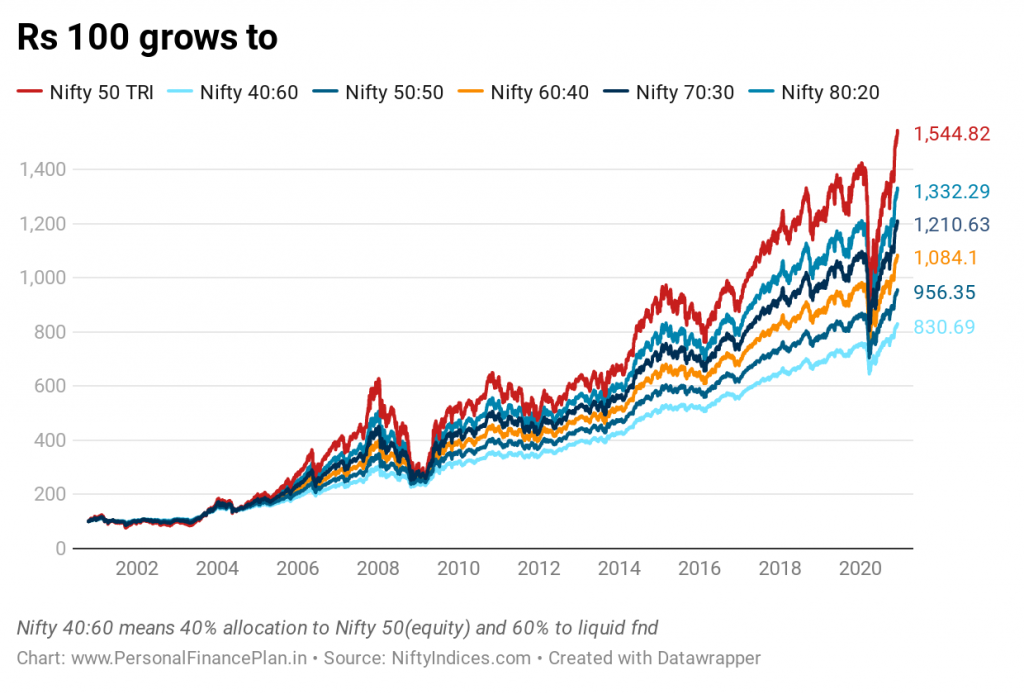

Performance Comparison

No surprises here. Given the wide difference in the returns (14.5% p.a. CAGR for Nifty 50 TRI and 7% p.a. CAGR for the HDFC liquid fund), a pure equity portfolio (100% Nifty 50 TRI) has beaten every asset allocation portfolio over the past 20 years.

In fact, higher the equity allocation, the better you have done.

However, this is not the complete picture. This is just a point-to-point return. We need to look at the rolling returns too. We will do this later.

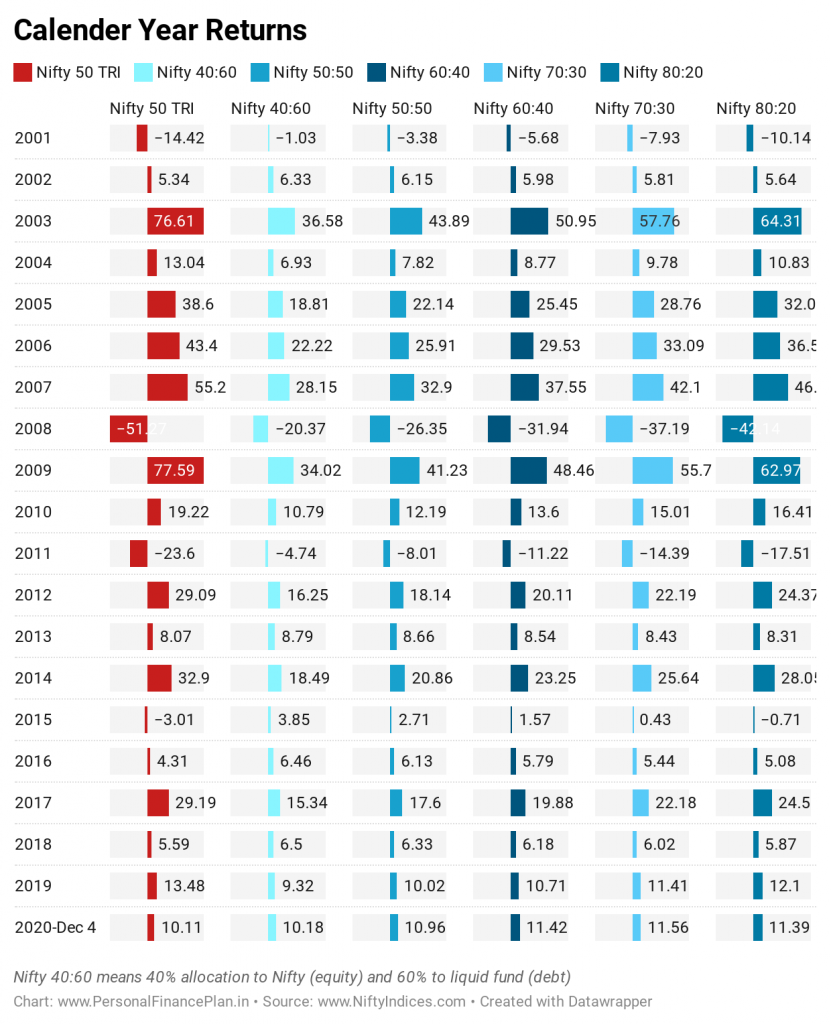

Similarly, with calendar year returns, the pure equity portfolio is either the best performer or the worst performer.

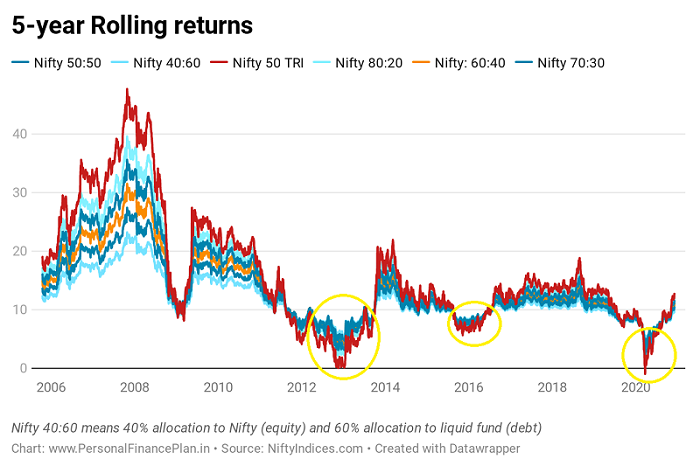

What about rolling returns?

Now, this is an interesting. Despite such good performance of Nifty 50 (compared to liquid fund) over these 20 years, there have been stretches of 5-year periods where the regularly rebalanced portfolios have beaten pure equity investments. Your patience as an equity investor will be tested during such times.

I thought it apt to break down the performance in 5-year and 10-year windows.

You can see that the outperformance of Nifty has come in the first 10 years (2001-2010). The most recent 10 years (2011-2020) have been mediocre for the pure equity portfolio (despite the massive run up in equity prices since March 2020). The regular rebalanced portfolios have delivered similarly at much lower volatility.

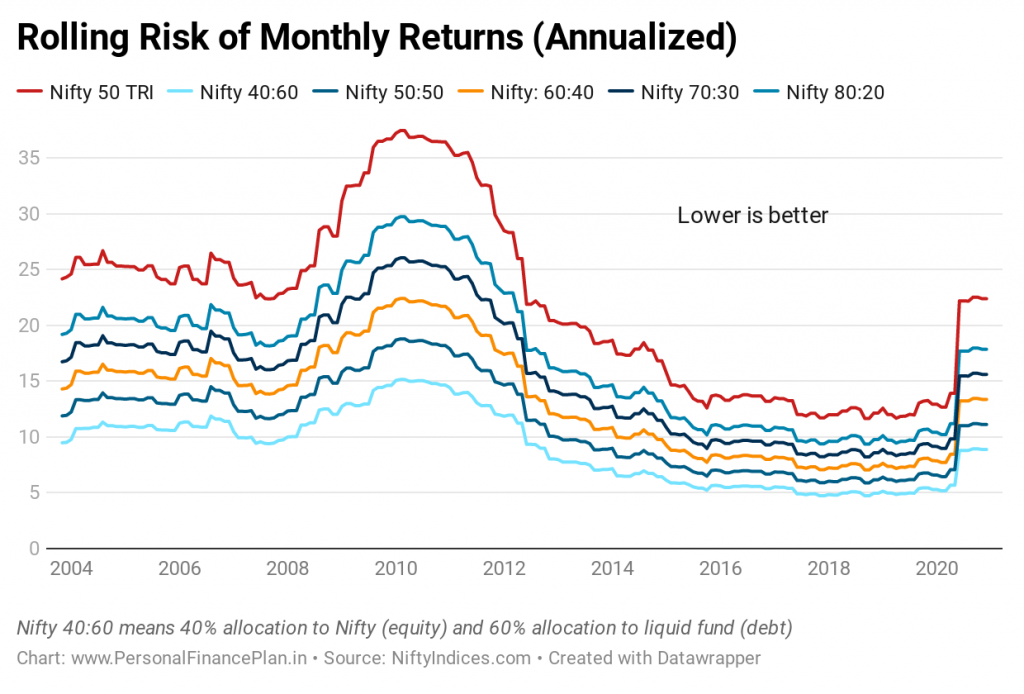

What about volatility and drawdowns?

No surprises here too. 100% Nifty 50 portfolio experiences the biggest drawdowns.

And working with an asset allocation approach and rebalancing portfolio regularly has reduced portfolio volatility.

And Low volatility is important. It is easy to see market dips and recoveries in charts. It is a completely different matter when you experience these events real-time with your money at stake. In my opinion, it is easier to stick with portfolios or strategies that are less volatile. Your worry or anxiety may make you do things that you might repent later. Easier to control your biases through a rule-based approach such as asset allocation and portfolio rebalancing. For most investors, a rules-based approach to investments will beat a gut-based approach over the long term.

Over the 20 years, asset allocation and portfolio rebalancing have not delivered higher returns, but it has reduced drawdowns and reduce volatility.

I have written before too that portfolio rebalancing may not always deliver excess returns (rebalancing bonus), especially if there is a wide difference in returns of the underlying assets. However, it will still likely reduce portfolio volatility, potentially resulting in better risk-adjusted returns.

Interestingly, in the most recent 10-year period (2011-2020), asset allocation portfolios have delivered returns almost similar to pure equity portfolios at much lower volatility.

Portfolio Rebalancing can be done in different ways

- I have considered annual rebalancing on April 1 every year i.e. on April 1 every year, you reset the portfolio back to the target asset allocation.

- Let’s say the target allocation is 50:50 equity:debt. Come April 1, the portfolio allocation is 52:48 equity:debt, you move 2% of portfolio from equity to debt and get back to target allocation of 50:50. Simple but that’s not the only way of rebalancing your portfolio.

- You can pick up a different date or a different rebalancing frequency. You could have selected January 1 as rebalancing date or even your birthday. Or you could have opted for monthly, quarterly or half-yearly rebalancing.

- A more frequent rebalancing schedule can result in higher transaction and tax costs.

- You can also work with thresholds. You rebalance only when a threshold is breached. Let’s say you are working with 60:40 (equity:debt) asset allocation. You rebalance the portfolio only if the equity allocation goes above 65% or falls below 55%. 5% above or below the target allocation.

- You can tinker with the deviation threshold too (5% in the previous example). It could be 10% of the target allocation (10% of 60% = 6%). In this case, you rebalance only if the equity allocation falls below 54% or rises above 66%.

- I believe in momentum investing and wouldn’t want to move out of a performing asset class early. Hence, I do not prefer to rebalance portfolio frequently. A six-monthly or an annual rebalancing schedule is fine. Working with thresholds will also likely prevent frequent rebalancing.

- You can use a combination of both approaches (threshold and rebalancing date). For instance, you check your portfolio every six months or 12 months. If the allocation has breached the threshold, you rebalance back to target levels or else let the portfolio untouched. If the equity allocation is 64% (60:40 portfolio with 5% threshold) on the rebalancing date, you do not rebalance the portfolio. On the other hand, if the equity allocation is 67% on the rebalancing date, you rebalance back to target allocation of 60:40.

- If you are in accumulation phase (still adding to your portfolio), you can tweak your incremental investments in the manner that portfolio asset allocation moves towards the target allocation. For instance, if your target asset allocation is 50:50 but the existing allocation is 55:45 (equity:debt), you can route more of your incremental investments towards debt. This way, you will also avoid transaction costs and taxes.

What is your preferred asset allocation? How frequently do you rebalance your portfolio?

Source/Additional Links

Disclaimer: Registration granted by SEBI, membership of BASL, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. Investment in securities market is subject to market risks. Read all the related documents carefully before investing.

Note: This post is for education purpose alone and is NOT investment advice. This is not a recommendation to invest or NOT invest in any product. The securities, instruments, or indices quoted are for illustration only and are not recommendatory. My views may be biased, and I may choose not to focus on aspects that you consider important. Your financial goals may be different. You may have a different risk profile. You may be in a different life stage than I am in. Hence, you must NOT base your investment decisions based on my writings. There is no one-size-fits-all solution in investments. What may be a good investment for certain investors may NOT be good for others. And vice versa. Therefore, read and understand the product terms and conditions and consider your risk profile, requirements, and suitability before investing in any investment product or following an investment approach.

5 thoughts on “What is the Best Asset Allocation for your portfolio? 50:50 or 60:40 or 70:30?”

sorry sir , the question is not relevant to the above thread but I will be grateful for any help

I have made a short term Capital loss of Rs. 50k And long term gain of Rs 1lakh in the same year. Now, as per notified rules the long term gain is exempt up to the limit of 1 lakh. My query is – .

1. Is it possible for me to claim the exemption on long term capital gains made during this year Of 1 lakh and Not set off the STC loss of this year and carry forward the Same to next year Since I know that I have made STC gain next year

Or it is mandatory to set off the short term losses first and claim the exemption on the remaining amount of LTCG(limit of 1 lakh)

Hi Vivek,

This is a grey area.

I had tried this in tax utility file sometime back.

STCG loss will automatically set off LTCG. Not desirable but that’s the way it is.

How about using a balanced fund (e.g. ICICI Dynamic Balanced fund, 65% equity. 35% Debt/Cash) to accomplish automatic rebalancing ? They can also be more opportunistic about debt vs equity allocations

That’s not a bad option. you can do that.

The problem can be their fixed income portfolios.

I have written about these products before.

https://www.personalfinanceplan.in/icici-balanced-advantage-dynamic-asset-allocation-fund-performance-review/

https://www.personalfinanceplan.in/balanced-hybrid-fund-value/

https://www.personalfinanceplan.in/credit-risk-hybrid-mutual-funds/

I want to invest 50% in a small cap index fund and 50% in short term debt fund via monthly SIP. Due to high volatility of small cap fund, I want to do rebalancing on the first of every month. Can you please backtest this portfolio for the last 10 years vs 100% investment in a small cap index fund via monthly SIP.

Thanking you,