The Finance Minister presented the final budget for FY2019-2020 on July 5, 2019. Here are the key highlights of the budget.

Income Tax slabs unchanged; Surcharge increased for the rich

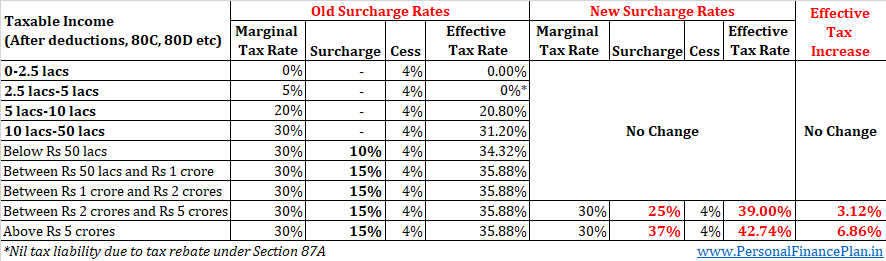

There has been no change in the income tax slabs. There is a sharp increase in surcharge for those earning more than Rs 2 crores.

We must understand the impact of the surcharge is not just limited to your salaries. The surcharge is levied on all types of income, even capital gains. Therefore, for a taxpayer with taxable income in excess of Rs 5 crores, the long-term capital gains tax on the sale of equity/equity mutual funds is 14.25% (10% LTCG tax, 37% surcharge and 4% cess). Earlier, it was only 11.96% (10% LTCG tax, 15% surcharge and 4% cess). This is quite a substantial increase.

The marginal relief on Surcharge can still be availed.

Additional Tax Benefit on Housing Loan under Section 80EEA

To give a fillip to the real estate sector, the Government has provided an additional tax deduction of Rs 1.5 lacs per financial year towards interest payment for the housing loan. This is subject to the following conditions

- The home loan must be sanctioned between April 1, 2019, and March 31, 2020.

- The stamp duty value of the house must not exceed Rs 45 lacs.

- You must not own any house on the date of sanction of the loan.

As you can see, this benefit is only for first-time buyers. This tax benefit under Section 80EEA will be available in the subsequent years too.

This tax benefit is over and above the tax benefit of Rs 2 lacs for home loan interest payment under Section 24. Therefore, the total tax benefit for the loan taken in FY2020 can go up to Rs 3.5 lacs.

At the same time, we must also see the utility of it. For a Rs 45 lacs house, you will get a loan of about Rs 36-37 lacs. At an interest rate of 9% and a loan of Rs 36 lacs for 15 years, you will pay Rs 3.2 lacs as interest in the first year. 3.08 lacs in the second year. 2.95 lacs in the third year and so on. The interest amount will be higher if the tenure was longer or the loan amount was higher.

Your actual benefit will depend on your tax slab too.

We must understand that the pre-conditions to avail tax benefit for interest payment are different under Section 24 and Section 80EEA.

The deduction under Section 80EEA is available for home loans from banks and approved financial institutions. Under Section 24, even interest paid on home loans from friends and relatives is eligible for tax benefit.

Under Section 24, you get the tax benefit on interest paid only after you have received possession of your house (interest paid before possession is eligible for deduction over the next 5 years in 5 equal installments). Section 80EE and 80EEA do not impose any requirement of possession or completion of construction. Therefore, Section 80EEA provides you immediate relief even if you have purchased an under-construction property.

Push towards Electric Vehicles (Deduction of Rs 1.5 lacs under Section 80EEB)

Good news for the buyers of Electric Vehicles.

If you take a loan to purchase an electric vehicle, you will get an additional tax deduction of Rs 1.5 lacs for the interest paid for such a loan under Section 80EEB. The tax benefit would be available for both cars and bikes.

The tax deduction is subject to the following conditions:

- The vehicle must be purchased between April 1, 2019 and March 31, 2023.

- The loan must be taken from a financial institution.

The tax relief is not just limited to the year of purchase but shall be available in the subsequent years too. In an additional boost, the Government has proposed to reduce GST on such vehicles from 12% to 5%.

Additional Announcements in the Budget

Gifts from Resident to Non-Residents (NRI) shall be considered to accrue in India and hence be subjected to income tax. Gifts received from close relatives, through inheritance or at the time of marriage continue to be exempt. Exemption of Rs 50,000 worth of gifts per financial year shall also continue to apply. Read this post for more on this topic.

Buyback Loophole plugged: Dividends from shares are subject to DDT of 15% (company pays the tax before transferring money to investor account). The dividends are free in the hands of the investors unless your total dividend receipts cross Rs 10 lacs in a financial year. Such investors have to pay an additional tax of 10%. Promoters/rich investors were likely to be worst affected by this rule. To circumvent this tax issue, the companies preferred to take the buyback route (instead of giving dividends). Buybacks of shares were a better and tax-efficient way to transfer money to shareholders. Now, the companies will have to pay 20% of the amount used for share buyback as tax. In a way, they have equalized the tax treatment of buybacks and dividends.

TDS on taxable life insurance policies increased from 1% to 5%. Your life insurance policy proceeds are taxable if the Sum Assured is less than 10 times the annual premium. 1% was on the gross amount. 5% is on the income from the policy.

The Government plans to launch a CPSE ETF along the lines of ELSS. You will get tax benefits under Section 80C. The Government uses CPSE ETFs for its divestment in PSUs. The modalities are still awaited. You can expect a lock-in for 3 years.

Definition of a PSU has been revised. Earlier, The Government had to own at least 51% of the entity. Now, the definition is, The Government and the entities owned by the Government must hold at least 51%. If you view this along with the previous point, you can see that the Government plans to raise a lot of money through divestment.

NPS taxation was revised in December last year. The entire 60% lump sum withdrawal permitted at the time of retirement was made tax-exempt. Central Government was to contribute 14% of the basic salary to its employees. Investment in NPS Tier II account was also added to Section 80C basket (only for Central Government employees). Enabling provisions have now been added to Section 80C, Section 80CCD and Section 10.

Customs duty on gold increased from 10% to 12.5%. Gold prices shot up on July 5 for this reason.

Extra cess on Diesel and Petrol.

TDS of 2% if the cash withdrawal exceeds Rs 1 crore from a bank account. Well, you can open multiple accounts. Do note it is TDS. You can claim back the extra tax deducted at the time of filing ITR.

Pre-filled tax returns to be made available for investors. The information from various sources (banks, stock exchanges, mutual funds) shall be auto-populated.

Tax-filing mandatory for those who have deposited more than Rs 1 crore in savings/current account OR have spent more than Rs 2 lacs on foreign travel OR have paid the electricity bill of over Rs 1 lac in a year.

NRIs can now be issued Aadhaar card after their arrival in India (permanent return in my opinion) without the waiting period of 180 days.

Regulatory authority of Housing Finance Companies to be shifted from National Housing Bank (NHB) to the Reserve Bank of India (RBI).

New coins of 1, 2, 5, 10 and 20 rupees to be launched.

PAN and Aadhaar card to be made interchangeable. Those who do not have PAN card can file returns by quoting their Aadhaar card.

A new pension scheme (Pradhan Mantri Karam Yogi Maandhan) for Small Businessmen and Traders with a turnover of less than Rs. 1.5 crores. It is along the lines of Atal Pension Yojana.

8 thoughts on “Final Budget 2019: Taxes for the Rich, Benefits for Buyers of Homes, Electric Vehicles”

Very Useful post Deepesh and thanks for the same ! A Big Thank U !!!

You are welcome, Prasad

If you can explain the NRI stock purchase and sale changes that will be great

As per 2019 budget…nri doesn’t need pis account any more…please advise

Hi Deepesh

In affordable housing, you can take loan upto 90%. With additional charges, you can claim 3.5 Lakhs in the first year.

Hi Ajay,

Thanks for the inputs.

LTV caps, risk weights and provisioning norms for the housing loans are specified by the RBI.

https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=10995&Mode=0

Hurrah, that’s what I was exploring for, what a data!

present here at this blog, thanks admin of this website.

I have noticed you don’t monetize personalfinanceplan.in, don’t waste your traffic, you can earn extra

cash every month with new monetization method. This is the best adsense alternative for any type

of website (they approve all sites), for more details

simply search in gooogle: murgrabia’s tools

I visit day-to-day a few blogs and information sites to read posts, however this weblog gives quality based articles.