Franklin Templeton AMC dropped a bomb yesterday. In a communication dated April 23, 2020, it notified that it is winding up 6 debt mutual fund schemes.

- Franklin Low Duration Fund

- Franklin Dynamic Accrual Fund

- Franklin Credit Risk Fund

- Franklin Short Term Income

- Franklin Ultra Short Bond

- Franklin Income Opportunities Fund

These are very popular schemes. The combined assets under these schemes are ~ 28,000 crores.

I copy an excerpt from Franklin Communication.

What does this mean?

- You can’t make any further purchases in the mentioned schemes.

- You can’t redeem your investments from the mentioned schemes. Your money is stuck.

It is like the entire portfolio of these schemes has been side-pocketed.

The realized value from the sale of underlying assets (or receipt from any interest/ principal from the bonds) will be distributed to the unit holders on proportionate basis.

Do note the NAV of these schemes will still be published on a daily basis.

Additionally, there are other mutual funds (both equity and debt) from Franklin that are open for business as usual. The issue is limited to only 6 debt mutual fund schemes.

Is my money lost?

No, your money is not lost (even though you may get back less).

It is just stuck. You have lost the flexibility of taking it out whenever you want.

As and when the fund realizes any money from these investments, it will be transferred to your bank account.

What must have forced Franklin AMC’s hand?

To meet redemptions, they must sell bonds. And the bond markets are not very liquid, especially for the not-so-good-credit-quality bonds.

You do not get good deals (and sometimes no deal at all) when you try to sell in illiquid markets. We witnessed how NAV of most debt mutual fund schemes (even liquid funds) fell during the month of March. This was because they faced sharp redemption pressures.

Franklin schemes have been witnessing sharp outflows too. For instance, Franklin Ultra Short used to be a ~ Rs 20,000 crore scheme just about a few months back. The scheme’s size as on April 23, 2020 is just Rs 9,728 crores. As I discussed in one of my earlier posts, a sharp drop in the size of the mutual fund scheme is a red flag.

Here is how the asset under management have fallen for Franklin UST Bond Fund.

Franklin knows the best about the quality of the portfolio of these schemes. Perhaps, Franklin figured out that it won’t be able to meet redemptions if outflows continued at this scale. That the credit quality of its portfolio was not particularly good didn’t help.

The lockdown and its repercussions will test viability of many weaker companies. Hence, it is difficult to find buyers for bonds from such weak companies.

In a way, it is also a prudent move. If the redemptions continued, Franklin would have continued to sell better quality bonds from its portfolios. Therefore, the investors who stayed back would be left with even lower quality portfolios.

When will I get my money back?

You will get your money back as and when the AMC realizes any income (interest payment or principal repayment) and sells these bonds. Sale of bonds is difficult during present times.

If you are an investor, look at the underlying portfolio to see when various exposures are maturing.

Franklin Ultra Short Bond fund is an ultra-short bond fund. For an ultra-short bond fund, the average maturity of the portfolio can be upto 6 months as per SEBI guidelines.

Franklin Low Duration Fund is a low duration fund. For a low duration fund, the average maturity (Macaulay duration) of the portfolio can be up to 1 year.

Therefore, you can expect an Ultra-short bond fund portfolio to mature faster. Hence, you are likely to get your money back sooner in case of an ultra-short bond fund (provided there are no defaults).

At the same time, average maturity of 6 months does not mean that all the underlying bonds will mature within 6 months. Remember, the cap is on Average maturity(Macaulay Duration of the portfolio, and not on the maturity of each bond).

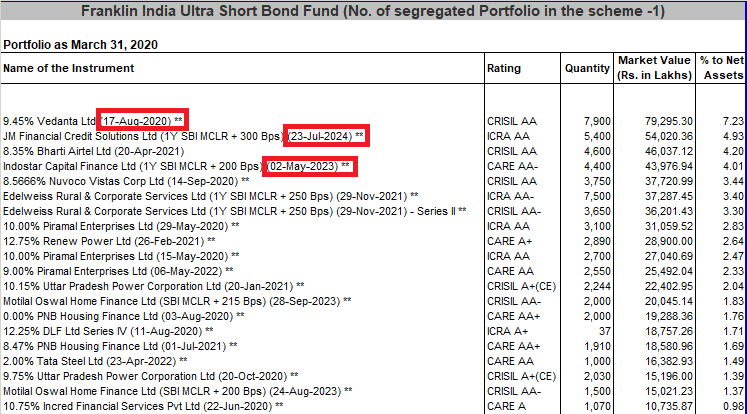

I copy a snapshot of some the portfolio holdings of Franklin Ultra Short Bond Fund as on March 31, 2020. You can see some of the bonds whose maturity extends to even 2024.

Do note this data is on March 31, 2020. On March 31, the size of Franklin Ultra Short Bond Fund was Rs 10,964 crores (On April 22, it is Rs 9,738 crores). So, it has lost Rs 1,200 crores over the last 3 weeks. The AMC would have sold investments to meet redemptions. Hence, the current portfolio may be very different from the one copied above.

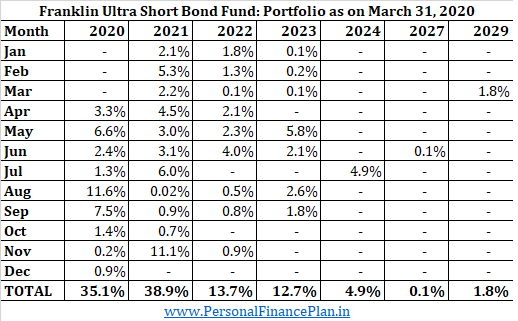

As for the portfolio as on March 31, 2020, here is how the maturity profile of the Franklin Ultra Short Bond Fund looks like.

The sum of all the percentages is more than 100%. This is because the scheme had borrowings as on March 31, 2020.

As mentioned earlier, the portfolio may have changed since March 31, 2020. You can see only 74% of the portfolio is maturing in the next two years. This is quite bizarre for an ultra short duration fund. Do note that this data is only about bond maturity (principal repayment). All the bonds will continue to pay interest too as per the schedule. Hence, you will more than what you see in the table (unless there are defaults).

How good is the portfolio?

While credit ratings are not really reliable, it still gives us an idea of the quality of the overall portfolio. In this case, this might indicate how much money you will get back.

I have put the portfolio in the descending order of credit quality. The only exception is A1 and A1+, which should be right up at the top (but I have put them lower). You can check the credit scale of various rating agencies here: CRISIL, ICRA CARE

Over 80% of the portfolio is AA- and above. So, I think you should get a fair amount back.

You can check the portfolio of other Franklin funds here (Select Monthly Portfolio Disclosure) and do similar analysis.

More worried about the “Beyond First order” effects

What we discussed above is how this Franklin move affects investors. However, I feel the repercussions of this move will be far-reaching.

What will be impact on other debt MF schemes from Franklin?

What about the confidence in other credit risk funds? Will this category survive?

The Credit Risk Mutual funds are a source of funding to many weaker companies. If their debt is having so many problems, what about their equity?

What about the confidence in debt mutual funds in general?

I don’t know the answer. Time will tell.

Choose your investments wisely

Disclosure: I do not have exposure in any of these schemes. However, as discussed in my earlier post on Franklin exposure to Vodafone-Idea bonds, I did recommend a few clients to take some exposure in Franklin Ultra Short Bond Fund as a credit risk fund. In hindsight, it looks like a bad decision. After Vodafone-Idea issue and especially after the recent lockdown, I had started asking investors to exit this fund. However, I could not communicate this to all and some of them will be stuck with small exposures. There are certain legacy portfolios (clients purchased before they started working with me) that still have significant exposure to Franklin Ultra Short Bond Fund. That is painful. Could have done better.

19 thoughts on “Franklin winds up 6 Debt MF schemes: What does it mean?”

Could these be some second order effects worth thinking about?

– run on even liquid debt funds

– spill over into even equity funds e.g small cap

Yes.

I don’t want to create panic (and there is no need to panic) but people may want to get out of debt mf schemes.

If MFs have to sell bonds to meet redemptions, there will be too much supply.

Many financial institutions (NBFCs/HFCs) that rely on refinancing may not be able to refinance their debt easily. And that complicates many things.

Small cap is equity. So, I am not worried much. Volatility/drawdown is expected. They can just sell at whatever prices.

As investors, we might want to see if this makes borrowing even more difficult for smaller companies.

Can this have an impact on liquid funds ?

Hi Amol,

The portfolio are quite good and liquid there. Therefore, in my opinion, it is unlikely.

Having said that, stranger things have happened this year.

It is about confidence in the system. Am sure some investors would want their way out.

Hi

Is this not a a typical “run on an MF” just like a “run on a bank”.

When there is “run” no fund house or even a Bank can withstand the redemption pressure.

Although sad, investors should not lose hope as these investment can be realized (debt funds) on the maturity date and the corporates hopefully will pay up. Agreed that there is no liquidity but at least there will be a recovery of money.

I am sure there will be collateral damage on all liquid funds as the main purpose of liquid fund was to be an alternate to bank deposits. People will move the money back to Banks.

Regards

Ninan

Hi Ninan,

It is not a run yet.

Yes, even the strongest banks can fail if a run happens.

It is all about confidence in the system. If everybody panics, then we are done.

We have not reached that stage yet. I hope the regulators (especially RBI) will come in and help if things got bad.

But, debt funds industry loses face with such events.

Many will move money back to FDs.

For anyone who is in say upto 20% tax bracket, there is little case for investing in debt funds.

This development is likely to cause a run on most of the debt funds, destabilising the whole bond market ecosystem.

This was and remains avoidable by of a govt or RBI backed corporate bond buying programme as repeatedly recommended by leading pink papers.

The Finance Ministry seems to be incapable of thinking beyond fiscal deficit number.

Hi Arvind,

Many things can happen.

I understand that bond markets will be mess if everyone tries to sell.

I believe, if the push comes to shove, the RBI will provide support (perhaps not by buying bonds, but lending against them through banks).

We will have to see how this space develops over the next few days and weeks.

Hi Deepesh,

Very crisp and informative article.

I am wondering about one point – why these schemes are being collectively referred to as ‘Credit Risk Fund’ in various communications by AMC and media articles? Of course, all debt MF will have some elements of credit risk. But as per the fact sheet and SEBI classification of these schemes, barring one or two, rest belonged to Low Duration, Ultra Short Term, Short Term, etc. So ideally credit risk component shouldn’t be prominent in these funds. Isn’t false communication is bit deceptive?

Regards,

Pratyush

Hi Pratyush,

SEBI classification (for low duration, ultra short, short term) puts restrictions based on average maturity of the portfolio.

The AMC can choose to invest in good credit quality bonds or poor quality bonds in the schemes. No restriction.

Franklin, as a fund house, took a lot of credit risk in some of its funds. Many other AMCs don’t.

That’s why everybody is loosely referring to all the funds as credit risk funds.

You can say that but the source of this problem is high credit risk in the portfolio.

Yes true. Thanks Deepesh for your views!!

Ho w can the Ultra Short Bond Fund can have so many top investments maturing after an years? Was FT giving wrong information with respect to average maturity of the scheme?

What is the likleyhood of getting back at least 50% of money invested in FT Ultra Short Bond Fund in the next 6 months?

Hi Vasanth,

The cap is on duration (and not average maturity). Duration also takes into account the timing of the cashflows. Therefore, the quantum of coupon also matters.

You are right. On the face of it (just by looking at their portfolio), one gets the impression that the average maturity is higher than 6 months.

However, if they have structured bond repayments in a way that it reduces duration, they might still be able to keep it down.

Honestly, looking at their portfolio, I am also confused how they have kept it lower.

There is a good chance that you will get 50% back over the next 6-8 months. The AMC might not just wait for the bonds to mature. They may try to find buyers in the secondary market.

Thank You Deepesh.

Dear Deep – Sad to see that things are happening so worse that Never happened in history that a reputed mutual fund company is closing 6 funds at once that too short-term credit debut funds:-((.

I have a question regarding these funds. I understand that the maturity of funds are just 6 months duration (Average) and in that case let’s say I invested Rs. 10,00,000 in Jan 2019 and the fund has grown to Rs. 10,80,000 including all accrued interest and when the fund is going to be LIQUIDATED now, will we be able to get at least the original principal amount of Rs. 10,00,000?

My understanding is that the individual bonds in which the funds hold, the companies who took credit should return the prinicipal amount once it reaches the maturity date. In that case, I feel we should get the principal back with majority of companies (Agreed a few companies will not be able to honour it and we will be losing principal too…)

Personally, I have invested Rs. 15,00,000 in Franklin Ultra-Short Bond Fund on April 2019. Can you please let me know at your convenience that will I be able to get an approximate amount of at least Rs. 12,00,000 back assuming a loss of 20% on its original cost?

Please help as the situation is horrendous…..

Thanks

Bava

Hi Saravana,

I can understand your frustration.

SEBI has put cap on duration (which is different from maturity). While calculating duration, the timing of cashflows also matters.

Hence, not all bonds are maturing in the next 6 months. Please look at the portfolio of the fund ending March 31, 2020. We need to wait for latest portfolio as on April 30, 2020. This would be out by 8-10th May.

Yes, as and when the payments are made by the underlying bonds, the AMC will keep transferring to your bank account.

I also believe most of these companies will meet all repayment commitments.

I will be surprised if you don’t even get 80% of your investment back.

Thank you very much for your fast response and I appreciate you. Will catch up with you later…

As usual, well explained, the situation.

As an immediate thought, would like to switch all debt funds to gilt funds. IMO. This is best time for gilt, being lower interest rates. But I found its getting impact -0.75% on Friday. Any thoughts on this ?

Thanks Sunil!!!

Yes, you can move to gilt funds but the interest rate risk will be higher there. Quite volatile too.

Lower current yield only means that the buy-and-hold returns over the long term will be in that range (not necessarily for MF since money keep coming in and going out).

For a short term investor in gilt funds, what matters is the outlook on interest rates going forward.

If you expect interest rates to fall, gilt funds could be a good choice (short term).

On the other hand, if you expect interest rates to rise (due to fiscal pressures), gilt funds are not the right place for the short term.